{kind=link}

“On this world nothing is definite however dying and taxes” stated Benjamin Franklin

(Founding father of USA and face on America’s 100 greenback invoice/observe).

Advance tax, because the identify implies, is the tax that one pays upfront. Advance tax is the earnings tax that’s payable in case your tax legal responsibility exceeds Rs 10,000 and ought to be paid in the identical 12 months wherein earnings is obtained. It is usually referred to as as “Pay as you Earn” scheme because you pay the tax in the identical 12 months wherein you earn earnings.

If you’re a Salaried worker and have earnings apart from earnings from wage then it’s best to verify Advance Tax.

If you’re Freelancer, Professionals, companies, YouTuber, Blogger then you need to know and pay Advance Tax

- In case you estimate that you’ll owe greater than Rs.10,000 on March 31 in taxes (after deducting TDS) then it’s best to pay advance tax.

- You pay this tax in 4 installments and the due dates with Proportion of Advance Tax to be paid are 15 June(15%), 15 September(45%), 15 December(75%) and 15 March(100%).

- If the Revenue Tax will not be payable as per the above schedule, Curiosity is liable to be paid for late fee of tax as follows

- Curiosity beneath part 234B @ 1% per thirty days

- Curiosity beneath part 234C @ 1% per thirty days is payable if 90% of the tax will not be paid earlier than the tip of the monetary 12 months

- Advance Tax could be paid by submitting a Tax Cost Challan,ITNS 280.Challan

- Tax relevant: For particular person Choose 0021 : INCOME-TAX (OTHER THAN COMPANIES)

- Kind of Cost: Kind of fee relies on why you might be paying earnings tax. Enter 100 for Advance Tax.

- You need to declare Advance Tax whereas submitting Revenue Tax Return ITR

Who has to pay Advance Tax?

The provisions of the Revenue Tax Act make it compulsory for each particular person, self-employed skilled, businessman, and company to pay Advance Tax, on any earnings on which TDS(Tax Deducted at Supply) will not be paid. Each people, in addition to corporates, should pay this tax.

Advance Tax for Salaried Worker

If a person’s solely earnings is his wage, then the employer will deduct tax from his earnings(TDS) and submit it. In such a case there isn’t any trigger for fear over advance tax fee. The tax deducted will likely be made out there to the worker by the employer in Kind 16.

However when a Salaried worker has earnings apart from earnings from wage then he has to fret about Advance Tax. Ex earnings from different sources equivalent to curiosity gained (on saving checking account), capital beneficial properties, lottery wins, from home property or from enterprise, then advance tax turns into related.

If one estimates that one will owe greater than Rs.10,000 on March 31 in taxes (after deducting TDS) then it’s best to pay advance tax.

Freelancers, Professionals, companies, YouTuber

Presumptive earnings for Professionals: Impartial professionals equivalent to docs, legal professionals, architects, and many others. come beneath the presumptive scheme beneath part 44ADA. They need to pay the entire of their advance tax legal responsibility in a single installment on or earlier than 15 March. They’ll additionally pay the total tax due by 31 March.

Presumptive earnings for Companies: The taxpayers who’ve opted for a presumptive taxation scheme beneath part 44AD need to pay the entire quantity of their advance tax in a single installment on or earlier than 15 March. In addition they have an choice to pay all of their tax dues by 31 March.

Who doesn’t need to pay Advance Tax?

Advance Tax is NOT relevant when

- A senior citizen (the resident particular person who’s 60 yrs or extra) who do not need any earnings from enterprise & occupation, doesn’t need to pay advance tax. This transformation was launched from AY 2013-14. Extra particulars at Senior Citizen : Revenue and Tax

- If one adopts presumptive taxation then one has to declare earnings on the prescribed fee and no different deductions are allowed. One has to pay your complete advance tax by 15 March. That is relevant for

The way to discover if you need to pay advance tax

As we all know there are 5 sorts of Revenue, Revenue from Wage, Revenue from Home Property(Any residential or business property that you simply personal will likely be taxed), Revenue from Capital Positive aspects (If you promote Mutual Funds, Shares, Bond, Gold, Land or Property, Revenue from Income and Positive aspects of Enterprise or Career & Revenue from Different Sources. Particulars in our article Perceive Revenue Tax

For advance tax verify

- Revenue from Home Property: You probably have rental earnings.

- Revenue from Capital Positive aspects: Have you ever bought Mutual Funds, Shares, Bond, Gold, Land, or Property. Tax categorized as Lengthy Time period Capital Acquire Tax(LTCG) and Brief Time period Capital Acquire(STCG) is predicated on the asset you bought, the time interval you owned the asset. Particulars in our article Capital Acquire Calculator on Sale on Property, Mutual Funds, Gold, Shares

- Revenue from Income and Positive aspects of Enterprise or Career: The earnings chargeable to tax is the distinction between the credit obtained on operating the enterprise and bills incurred.

- Revenue from Different sources: Test the following earnings. Particulars in our article Revenue From Different Sources

- the curiosity of Saving Financial institution Account,

- Curiosity from Mounted Deposit, Recurring Deposit, Senior Citizen Saving Scheme(SCSS) and many others

- Curiosity from Revenue Tax Refund

- Household Pension

- Dividend Revenue: Dividend obtained on or after 1 April 2020 is taxable within the palms of the investor/shareholder. Particulars in our article Dividend and Tax

What if we don’t pay Advance Tax?

If you need to pay advance tax and In case you fail to pay your Advance Tax or, should you pay lower than the stipulated tax, you’d be penalised and must pay additional beneath Sections 234A, 234B, 234C. So there isn’t any escaping Tax. Because the Revenue Tax workplace says “Pay Tax Karo Chill out“

The curiosity is calculated at 1% easy curiosity per thirty days on the defaulted quantity for 3 months. The curiosity penalty would proceed as much as the subsequent deadline. If even after the final deadline of 15 March, the tax will not be paid, then the 1% can be on the defaulted quantity for a month, till the tax is absolutely paid.

Why Pay Advance Tax?

Advance tax is without doubt one of the main instruments utilized by the Govt. to gather tax from the assesses throughout India. This pay as you go type of tax is designed in such a means that an assessee is made to pay tax to the Govt. in a ‘Pay as You Earn Scheme’. This primarily goals at lowering the last-moment hassles to an assessee for fee of tax legal responsibility which can be due to both scarcity of time or funds.

The purpose of the Indian authorities behind organising the advance tax system was to hurry up the tax assortment. This method additionally allowed the federal government to earn curiosity on the quantity collected as tax, thus growing funds to the federal government coffers.

How is advance Tax Calculated?

Advance tax is computed on earnings that a person would possibly earn in the course of the 12 months, in that sense, it’s estimated earnings. The tax is calculated utilizing the charges relevant for the monetary 12 months.

Suppose after paying your first installment of tax on the estimated earnings, your precise earnings elevated as a consequence of some shares/mutual funds you bought, You will have to revise your earnings and accordingly pay the differential within the subsequent installment.

Though Advance Tax is liable to be paid on all incomes together with Capital Positive aspects, it’s troublesome to estimate the Capital Positive aspects which can come up in an 12 months. Due to this fact, in such circumstances, it’s supplied that if any such earnings arises after the due date of any installment, then, your complete quantity of tax payable on such capital acquire (after claiming exemption beneath part 54) shall be paid in remaining installments of Capital Positive aspects that are due. If your complete quantity of tax payable is so paid, then no curiosity on late fee will likely be levied

Listed beneath are the steps to calculate advance tax:

- Decide the Revenue: Decide the earnings you obtain apart from your wage. It’s necessary to incorporate any ongoing agreements that may pay out later.

- Minus the Bills: Deduct your bills from the earnings. You’ll be able to deduct bills associated to your work (freelancing) equivalent to hire of the work place, journey expense, web and cellphone prices.

- Complete the Revenue: Add up different earnings that you simply would possibly obtain within the type of hire, curiosity earnings, and many others. Deduct the TDS deducted out of your salaried earnings.

- Complete Advance Tax: If the tax due exceeds Rs.10,000 you then’ll need to pay advance tax.

Advance tax Charges and Dates

From FY 2016-17 For each particular person and company taxpayers

| Due Date | Advance Tax Payable |

|---|---|

| On or earlier than fifteenth June | 15% of advance tax |

| On or earlier than fifteenth September | 45% of advance tax |

| On or earlier than fifteenth December | 75% of advance tax |

| On or earlier than fifteenth March | 100% of advance tax |

Beneath are the dates and percentages earlier than FY 2016-17.

| Due Date | Installment % of Advance Tax |

| fifteenth September | Up-to 30% |

| fifteenth December | Up-to 60% |

| fifteenth March | Up-to 100% |

For instance, suppose your complete tax legal responsibility(after deducting TDS) for this 12 months is Rs 1,00,000

So by fifteenth June you have to to pay 15% which involves Rs 15,000

So by fifteenth September you have to to pay 45% which involves Rs 45,00

By fifteenth December you’ll have to cowl 75%, so you have to to pay one other Rs 75,000.

By fifteenth March, 100% of advance tax involves Rs 100,000, you have to to pay one other Rs 25,000.

Penalty on not paying/paying much less Advance Tax: Sections 234A, 234B and 234C

In case you owe greater than Rs.10,000(after deducting TDS) whereas submitting your returns, you can be penalized with Curiosity beneath sections 234A , 234 B & 234 C

Underneath Part 234C, there are three parts. For the primary instalment, the shortfall penalty is calculated for 3 months @1% p.m. Equally, within the second instalment, the shortfall penalty can also be calculated for 3 months @1% p.m and the ultimate instalment is calculated at a flat fee if 1% for 1 month solely.

Underneath part 234B, penalty arises when the overall quantity of advance tax paid together with the quantity of TDS is lower than 90% of the overall tax legal responsibility. In such a case, curiosity is calculated at 1% per thirty days of the quantity of shortfall for the time interval from April to the month wherein the return is filed.

Underneath part 234A, the legal responsibility arises solely when the return is filed after the due date which for AY 2020-21 is 30 Nov.

Finotax has nice Advance tax calculators. Test it out right here. Let’s have a look at these sections intimately.

Curiosity beneath part 234 C

234 C will likely be relevant should you don’t pay your advance taxes in common installments. As per the Revenue Tax Act, you’re presupposed to pay 15% of advance tax by 15 Jun, 30% of your advance tax by fifteenth Sep, 60% by fifteenth December and 100% by fifteenth March. Let’s see it by means of some examples.

Mr. Khushal is operating a clothes store. Tax Legal responsibility of Mr. Khushal is Rs 45,500. He has paid advance tax as given beneath:

Rs. 8,000 on fifteenth June, Rs. 11,000 on fifteenth September, Rs. 12,000 on fifteenth December, Rs. 14,500 on fifteenth March. Is he liable to pay curiosity beneath part 234C, if sure, then how a lot?

Any tax paid until thirty first March will likely be handled as advance tax. Contemplating the above dates, the advance tax legal responsibility of Mr. Khushal at totally different installments will likely be as follows:

1) In first installment: Not lower than 15% of tax payable ought to be paid by fifteenth June. The tax legal responsibility is Rs. 45,500 and 15% of 45,500 quantities to Rs. 6,825. Therefore, he ought to pay Rs. 6,825 by 15thJune. He has paid Rs. 8,000, therefore, there isn’t any quick fee in case of first installment.

2) In second installment: Not lower than 45% of tax payable ought to be paid by 15thSeptember. Tax legal responsibility is Rs. 45,500 and 45% of 45,500 quantities to Rs. 20,475. Therefore, he ought to pay Rs. 20,475 by fifteenth September. He has paid Rs. 8,000 on fifteenth June and Rs. 11,000 on fifteenth September (i.e. complete of Rs. 19,000 is paid until 15thSeptember). There may be quick fee of Rs. 1,475 (i.e. Rs. 20,475 – Rs 19,000).

Although there’s quick fee of Rs. 1,475 however Mr. Khushal won’t be liable to pay curiosity beneath part 234C as a result of he has paid minimal of 36% of advance tax payable by fifteenth September. He has paid Rs. 19,000 until fifteenth September and 36% of 45,500 quantities to Rs. 16,380. Therefore, no curiosity shall be levied in case of deferment of second installment.

3) In third installment: Not lower than 75% of tax payable ought to be paid by fifteenth December. Tax legal responsibility is Rs. 45,500 and 75% of 45,500 quantities to Rs. 34,125. Therefore, he ought to pay Rs. 34,125 by fifteenth December. He has paid Rs. 8,000 on fifteenth June, Rs. 11,000 on fifteenth September and Rs. 12,000 on fifteenth December (i.e. complete of Rs. 31,000 is paid until 15thDecember). There’s a quick fee of Rs. 3,125 (i.e. Rs. 34,125 – Rs 31,000). Therefore, he will likely be liable to pay curiosity beneath part 234C on account of quick fall of Rs. 3,125 (*).

There’s a quick fall of Rs. 3,125 in case of third installment. On account of quick fall in case of third installment, curiosity beneath part 234C will be levied. Curiosity will likely be levied at 1% per thirty days or a part of the month on the quick paid quantity of Rs. 3,100 (i.e. Rs. 3,125 rounded off to Rs. 3,100 as per Rule 119A). Curiosity will likely be levied for a interval of three months. In different phrases, curiosity will likely be levied on Rs. 3,100 at 1% per thirty days for 3 months. Curiosity beneath part 234C will come to Rs. 93.

4) In final installment: 100% of tax payable ought to be paid by fifteenth March. The entire tax legal responsibility of Rs. 45,500 is paid by Mr. Khushal by fifteenth March (i.e. 8,000 on fifteenth June, Rs. 11,000 on15th September, Rs. 12,000 on fifteenth December and Rs 14,500 on fifteenth March). Therefore, there isn’t any quick fee in case of final installment. Thus, Mr. Khushal won’t be liable to pay curiosity beneath part 234C in case of final instalment.

Curiosity beneath part 234 B

234 B will likely be relevant when the overall advance tax paid is lower than 90 % Tax Payable. This will likely be charged at 1% per thirty days until you pay your remaining taxes. Let’s work it out by means of an Instance:

Mr. Suraj is a businessman. His tax legal responsibility as decided beneath part 143(1) is Rs. 28,400. He has not paid any advance tax however there’s a TDS credit score of Rs. 10,000 in his account. He has paid the stability tax on thirty first July i.e. on the time of submitting the return of earnings. Will he be liable to pay curiosity beneath part 234B, if sure, then how a lot

On this case, the tax legal responsibility (after permitting credit score of TDS) of Mr. Suraj involves Rs. 18,400 (i.e. Rs. 28,400 – Rs. 10,000) which exceeds Rs. 10,000 and therefore, he will likely be liable to pay advance tax. He has not paid any advance tax and therefore, he will likely be liable to pay curiosity beneath part 234B. Curiosity beneath part 234B will likely be levied at 1% per thirty days or a part of the month. In this case, Mr. Suraj has paid the excellent tax on thirty first July and therefore, curiosity beneath part 234B will likely be levied for the interval from 1st April to thirty first July i.e. for 4 months. Curiosity will likely be levied on unpaid tax legal responsibility of Rs. 18,400. Curiosity at 1% per thirty days on Rs. 18,400 for 4 months will come to Rs. 736.

In case you pay our taxes in between April – July interval then curiosity @1% will likely be utilized solely on the stability tax payable .

On-line Advance Tax Calculators(Free)

Video on Advance Tax

This 8:32 video explains Advance Tax.

This video talks about how one can Calculate Advance Tax

The way to pay advance Tax?

You’ll be able to pay advance tax in India by means of two strategies: on-line or offline. Right here’s a breakdown of each:

On-line Cost:

- Go to the Revenue Tax Division’s e-payment web site: [income tax e payment ON Income Tax Department portal.incometax.gov.in]

- Enter your PAN and cellular quantity and proceed after verification with OTP.

- Choose the Evaluation 12 months (2024-25 for present situation) and select “Advance Tax (100)” beneath Kind of Cost.

- Fill within the challan particulars like State Code, circle code (refer web site for particulars).

- Select the fee technique (internet banking or debit card) and your financial institution.

- Preview the challan for accuracy and click on “Pay Now” to finish the fee.

Offline Cost:

- Obtain Challan 280 type from the Revenue Tax Division web site.

- Fill the challan with particulars like your PAN, evaluation 12 months, tax kind (100 for Advance Tax).

- Point out the installment quantity (relies on the due date).

- Submit the finished challan at any financial institution approved to gather tax funds.

Extra Ideas:

- Use an advance tax calculator to estimate your tax legal responsibility for correct fee.

- Make a copy of the challan (on-line fee receipt or Challan 280 copy) for record-keeping throughout ITR submitting.

- The final date for the present installment (March 2024) is March fifteenth, so make sure you pay earlier than the deadline to keep away from curiosity penalties.

Advance Tax could be paid by submitting a Tax Cost Challan,ITNS 280.Challan, at designated branches of banks empanelled with the Revenue Tax Division. Branches of ICICI, HDFC and SBI settle for Advance Tax Cost Challans. Alternatively, people may pay Advance Tax on-line by means of the Revenue Tax Dept / NSDL web site. e-Cost facilitates fee of direct taxes on-line by taxpayers. To avail of this facility the taxpayer is required to have a net-banking account with any of the Licensed Banks.

Video on The way to Pay Advance Tax

https://www.youtube.com/watch?v=uyS00Ofc6og

Confirm Advance Tax in Kind 26AS

Half C of Kind 26AS has particulars of Tax Paid (apart from TDS or TCS). You probably have paid Advance Tax or Self Evaluation Tax it will seem on this part. Please confirm that advance tax or self evaluation tax particulars are displaying up in Kind 26AS, In the event that they don’t match together with your particulars please contact the Financial institution.

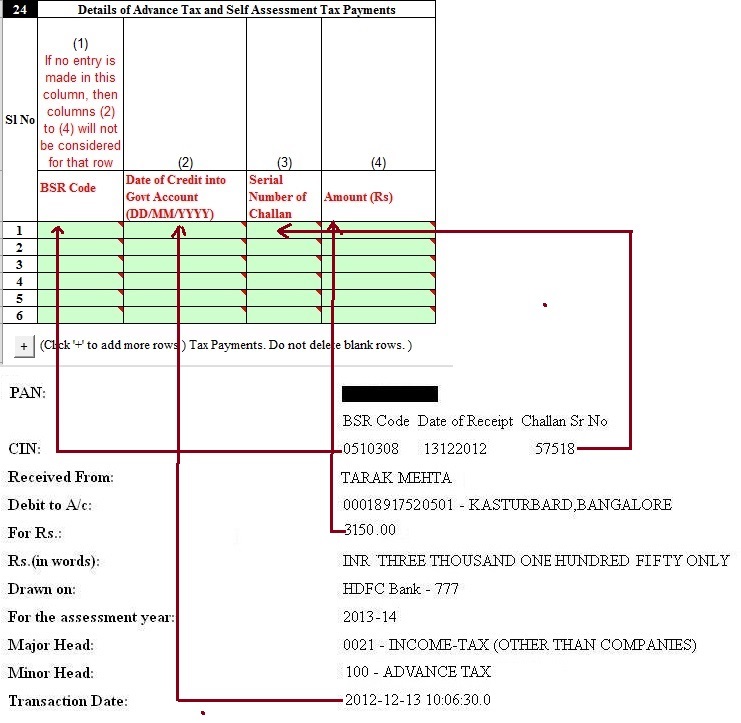

Present Advance Tax in ITR

After paying earnings tax by means of Challan 280 what subsequent? Is your duty over. No. You must present the tax paid in your ITR, You probably have paid Advance/ Self Evaluation tax by means of Challan 280 fill within the particulars in Tax paid and ensure that your tax legal responsibility is 0 earlier than submitting the return as defined for ITR1 in our article Fill Excel ITR1 Kind : Revenue, TDS, Advance Tax and proven in picture beneath.

Associated Posts:

It’s stated “Revenue tax returns are probably the most imaginative fiction being written immediately.”

Do you pay Advance Tax?