{kind=link}

The US is the envy of the world by way of monetary markets and financial efficiency.

Ruchir Sharma at The Monetary Instances outlines how that is impacting capital flows:

World traders are committing extra capital to a single nation than ever earlier than in fashionable historical past.

And the greenback, by some measures, trades at the next worth than at any time for the reason that developed world deserted fastened trade charges 50 years in the past.

The US now attracts greater than 70 per cent of the flows into the $13tn world marketplace for non-public investments, which embody fairness and credit score.

America’s share of worldwide inventory markets is way higher than its 27 per cent share of the worldwide financial system.

There are causes for the tidal wave of cash pouring into america.

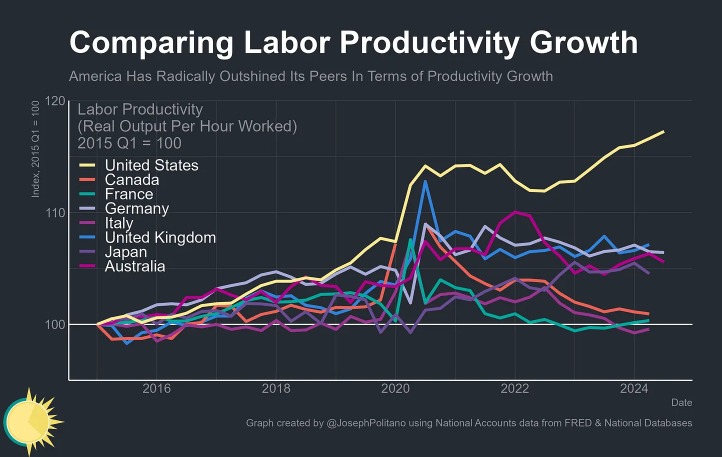

Joey Politano breaks down the productiveness increase within the U.S. and the way it compares to the remainder of the developed world:

He explains:

Productiveness development is nothing wanting the bedrock of progress–in the long term, creating extra with the identical quantity of labor is the one approach to durably improve wages, consumption, and society’s total prosperity. That makes it such a historic achievement that American financial output per hour labored has risen 8.9% during the last 5 years–sooner than the 5 years prior or any level within the 2010s–despite the COVID-19 pandemic.

We’re on an financial heater in the mean time.

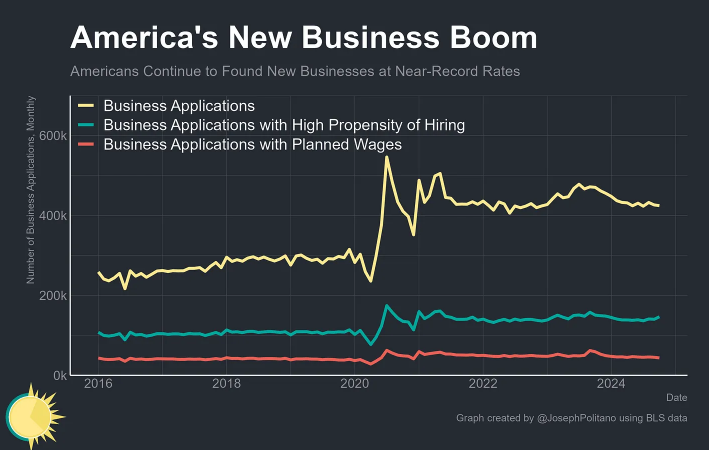

You possibly can’t supply a single variable as a purpose when coping with the complexities of one thing as giant as the worldwide financial system. However one of many principal causes for our success boils right down to being extra comfy taking danger.

Simply take a look at all the new companies which were fashioned for the reason that pandemic:

Threat-taking is a part of our tradition identical to spending cash, investing in shares and playing.

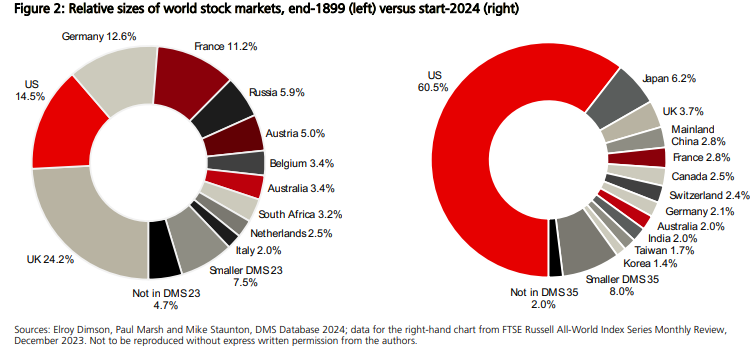

The inventory market will not be the financial system however it’s fairly wild that america makes up round 1 / 4 of worldwide financial output however almost 70% of the worldwide inventory market:

You’ll discover most different nations have comparatively comparable weightings for shares and GDP — Canada, Japan, Britain, France, Germany, and so forth. The 2 outliers listed here are China and america.

China makes up 17% of world GDP however lower than 3% of the MSCI All-Nation World Index. These numbers aren’t static after all.

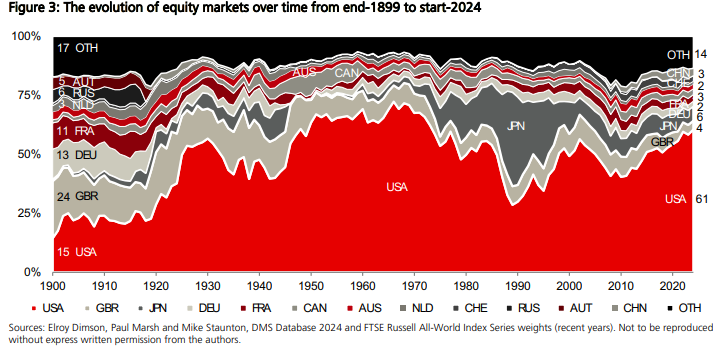

UBS World Funding Returns Yearbook yearly updates one in all my favourite charts that reveals the variations in nation weights between 1900 and now:

The US was lower than 15% of worldwide fairness markets in 1900. Now it seems to be like we’re slowly swallowing the remainder of the world.

These strikes don’t happen in a straight line although:

Within the Fifties and Sixties, the U.S. had a fair larger share of world fairness markets. Japan almost caught as much as us by 1990 however that reversed simply as rapidly. The U.S. shot up once more within the Nineteen Nineties however fell within the first decade of this century. Now it’s again on the upswing.

I’m not all that involved with the present weightings. This stuff are cyclical however the cycles are likely to play out over multi-decade timeframes.

My largest query for the long run is that this: Can anybody problem america by way of financial may?

It positive doesn’t seem to be it within the present surroundings.

Additional Studying:

The New Regular of Negativity

This content material, which incorporates security-related opinions and/or info, is supplied for informational functions solely and shouldn’t be relied upon in any method as skilled recommendation, or an endorsement of any practices, services or products. There might be no ensures or assurances that the views expressed right here will probably be relevant for any specific details or circumstances, and shouldn’t be relied upon in any method. It is best to seek the advice of your individual advisers as to authorized, enterprise, tax, and different associated issues regarding any funding.

The commentary on this “publish” (together with any associated weblog, podcasts, movies, and social media) displays the non-public opinions, viewpoints, and analyses of the Ritholtz Wealth Administration staff offering such feedback, and shouldn’t be regarded the views of Ritholtz Wealth Administration LLC. or its respective associates or as an outline of advisory companies supplied by Ritholtz Wealth Administration or efficiency returns of any Ritholtz Wealth Administration Investments consumer.

References to any securities or digital property, or efficiency information, are for illustrative functions solely and don’t represent an funding suggestion or supply to offer funding advisory companies. Charts and graphs supplied inside are for informational functions solely and shouldn’t be relied upon when making any funding choice. Previous efficiency will not be indicative of future outcomes. The content material speaks solely as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these supplies are topic to vary with out discover and should differ or be opposite to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Administration, receives cost from varied entities for ads in affiliated podcasts, blogs and emails. Inclusion of such ads doesn’t represent or suggest endorsement, sponsorship or suggestion thereof, or any affiliation therewith, by the Content material Creator or by Ritholtz Wealth Administration or any of its staff. Investments in securities contain the danger of loss. For extra commercial disclaimers see right here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see disclosures right here.