{kind=link}

Deepak Fertilisers & Petrochemicals Corp Ltd – From Quantity to Worth

Established in 1979 and headquartered in Pune, Deepak Fertilisers & Petrochemicals Company Ltd. is a number one producer of commercial chemical compounds, crop vitamin options, and mining chemical compounds. It stands as South Asia’s largest nitric acid producer and India’s main producer of Iso Propyl Alcohol (IPA). The corporate can also be the only Indian producer of a number of ammonium nitrate variants. Working six manufacturing services, Deepak Fertilisers helps a various vary of sectors, together with prescribed drugs, agrochemicals, dyes and intermediates, defence, resins, textiles, fertilisers, mining, and agriculture.

Merchandise and Companies

The corporate’s choices are categorised throughout 4 enterprise verticals:

- Industrial Chemical substances – Isopropyl Alcohol (IPA), nitric acid, liquid carbon dioxide, methanol, and so on.

- Technical Ammonium Nitrate (TAN) – Low, excessive and medical grade ammonium nitrate, ammonium nitrate resolution. Moreover, the corporate additionally gives platinum blasting companies within the Australian mining sector.

- Crop Diet Merchandise – Bulk fertilizers, specialty fertilizers, water soluble fertilizers, micronutrient and secondary vitamins.

- Creaticity – Furnishings mall and residential decor retailer in Pune.

Subsidiaries: As of FY24, the corporate has 11 subsidiaries and no different three way partnership/affiliate firm.

Funding Rationale

- Enlargement plans – The corporate is actively increasing its manufacturing capabilities to strengthen its market place and drive long-term progress. At Gopalpur, the corporate is establishing a TAN manufacturing facility. This venture, with a capability of 376 KTPA, is predicted to be commissioned in Q4FY26 and can improve the corporate’s complete TAN manufacturing capability to 1 million tonnes each year, reinforcing its management within the section. On the similar time, the corporate is enterprise a strategic backward integration venture at Dahej, aimed toward enhancing in-house nitric acid manufacturing. The venture – comprising 300 KTPA of weak nitric acid and 150 KTPA of concentrated nitric acid can also be scheduled for commissioning in Q4FY26, with a complete funding of Rs.1,950 crore. That is anticipated to place the corporate as the biggest nitric acid producer in Asia. In FY23, the corporate additionally commissioned a 1,500 MTPD ammonia plant, considerably lowering reliance on imported uncooked supplies. Moreover, to safe its vitality necessities, it has entered into India’s largest personal sector LNG provide settlement with Norwegian vitality main Equinor, which can begin from FY26.

- Worth-driven progress method – The corporate is strategically shifting from a commodity – centered mannequin to a value-added, solution-oriented method throughout its core segments. Within the mining chemical compounds section, roughly 16% of income now comes from the B2C channel, pushed by built-in blasting companies that improve pricing energy and margin stability. Its Australian subsidiary, Platinum Blasting Companies, provides complete options past TAN provide – together with blast design and technical help – strengthening buyer relationships and shielding the enterprise from commodity value volatility. Equally, within the Crop Diet Enterprise (CNB), the specialty portfolio, which contributes 45% of CNB income, instructions a pricing premium of 40% in comparison with 15% for bulk fertilizers. The section delivered a powerful quarter, with manufactured bulk fertilizer volumes reaching 1.8 lakh MT (up 3% YoY), whereas specialty merchandise like Croptek and pencil water-soluble grades grew 73% and 21% YoY, respectively, reflecting deeper market penetration and rising farmer adoption.

- Q1FY26 – Throughout the quarter, the corporate generated the income of Rs.2,659 crore, reaching a rise of 17% as in comparison with the Rs.2,281 crore of Q1FY25. EBITDA improved by 11% YoY, from Rs.464 crore to Rs.513 crore. Web revenue stood at Rs.244 crore, an upsurge of twenty-two% from Rs.200 crore of Q1FY25. Throughout the quarter, the corporate additionally achieved a big enchancment in its internet debt-to-EBITDA ratio from 1.72x to 1.50x.

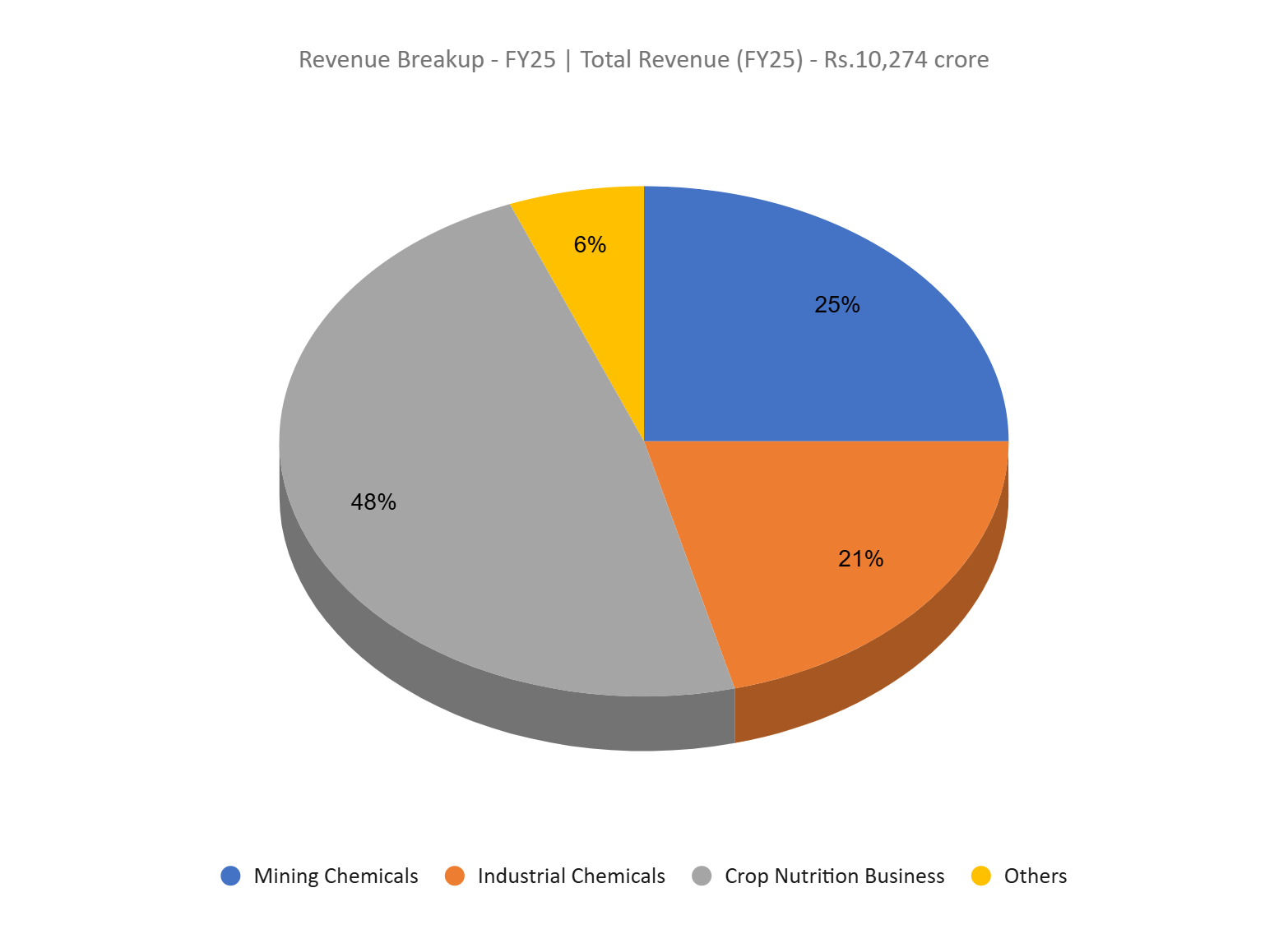

- FY25 – Throughout the monetary yr, firm’s income elevated by 18% to Rs.10,274 crore, working revenue elevated by 50% to Rs.1,925 crore and internet revenue elevated by 107% to Rs.945 crore.

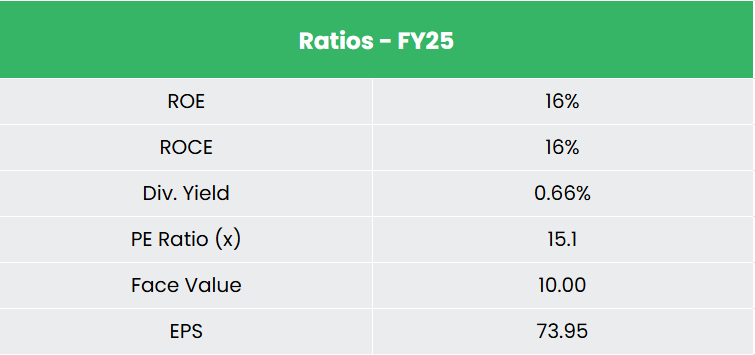

- Monetary Efficiency – The income and internet revenue CAGR of the corporate for the previous 3 years is round 10% and 12% between FY23-FY25. TTM gross sales and internet revenue progress is at 23% and 82% respectively. The three-year common ROE and ROCE for the corporate is round 16% and 17% throughout FY23-25. The corporate has a wholesome capital construction with a debt-to-equity ratio of 0.67.

Business

The Indian chemical trade is very diversified, comprising over 80,000 merchandise and using greater than 2 million individuals. It contributes round 7% to the nation’s GDP and ranks because the sixth largest globally and third in Asia. Sturdy demand from end-user industries corresponding to meals processing, private care, and residential care is driving speedy progress within the specialty chemical compounds section. Valued at roughly US$ 220 billion, the trade is projected to develop to US$ 300 billion by 2030 and attain US$ 1 trillion by 2040. Regardless of international uncertainties, the sector stays a hub of alternative, with Indian firms increasing capability to satisfy rising home and worldwide demand. The trade spans key segments together with bulk chemical compounds, specialty chemical compounds, agrochemicals, petrochemicals, polymers, and fertilizers.

Development Drivers

- Union Funds 2025-26 allocation of Rs.1,61,965 crore (US$ 18.7 billion) to the Ministry of Chemical substances and Fertilizers.

- A 2034 imaginative and prescient for the chemical compounds and petrochemicals sector has been arrange by the federal government to discover alternatives to enhance home manufacturing, scale back imports and appeal to investments within the sector.

- Ministry of Chemical substances and Fertilisers is working in direction of implementing the Manufacturing Linked Incentive (PLI) for the specialty chemical compounds sector.

Peer Evaluation

Opponents: SRF Ltd, Rashtriya Chemical substances & Fertilizers Ltd, and so on.

In comparison with the above opponents, the corporate is producing substantial returns from the capital invested backed by a secure progress in gross sales.

Outlook

The corporate’s ahead and backward integration initiatives are anticipated to considerably decrease dependence on imported uncooked supplies, improve value management, and supply a cushion towards commodity value volatility – components that collectively help margin stability and strengthen long-term profitability. Moreover, the Authorities of India has elevated the export quota for TAN from 20,000 to 50,000 metric tonnes, opening up better worldwide market alternatives. With upcoming services on each the western and jap coasts, the corporate will function via a dual-location manufacturing mannequin, which is probably going to enhance logistical effectivity and scale back freight prices for home and export clients alike.

Valuation

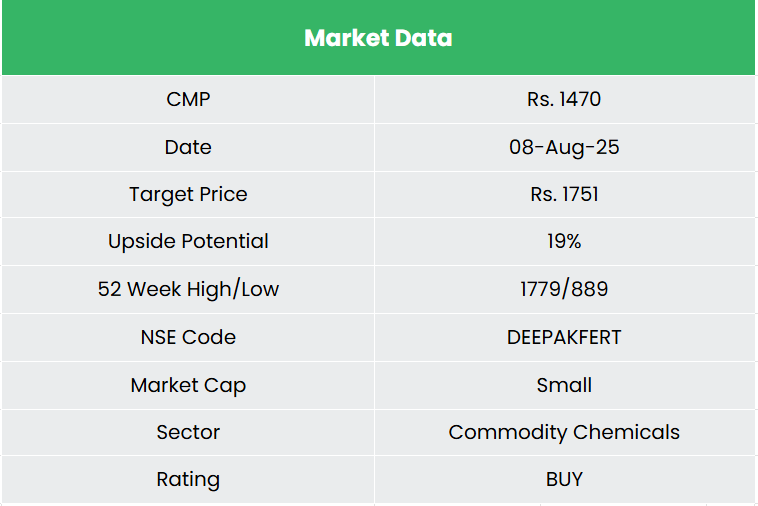

With its give attention to value-added progress, margin growth, and demand backed capability additions, we imagine Deepak Fertilisers is well-positioned to ship sustainable long-term returns. We advocate a BUY ranking within the inventory with the goal value (TP) of Rs.1,751, 17x FY27E EPS.

Word: We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back danger successfully.

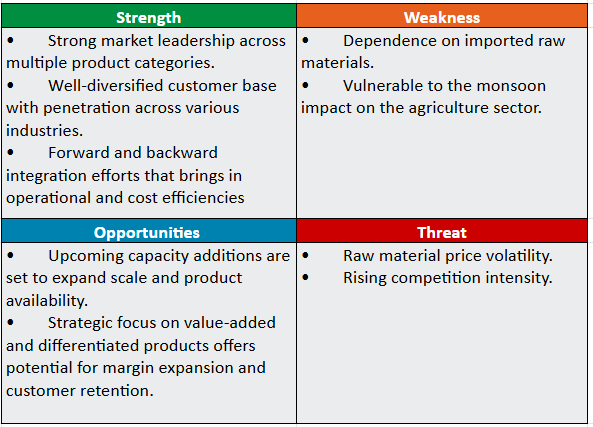

SWOT Evaluation

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please word that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles chances are you’ll like

Submit Views:

63