{kind=link}

The Reserve Financial institution of India (RBI) has launched the most recent quantity (twenty seventh version) of its annual statistical publication, ‘Handbook of Statistics on the Indian Economic system (2024-25) on twenty ninth August 2025. By means of this publication, the Reserve Financial institution has been offering key knowledge on numerous Financial and Monetary indicators for the Indian financial system.

The handbook’s predominant objective is to disseminate historic time-series knowledge, permitting its readers to research newest developments and examine the efficiency of assorted monetary and financial indicators over time. This knowledge could be very essential for understanding modifications in family financial savings charges and debt ranges, that are key indicators of financial well being.

Primarily based on this statistical knowledge, I’ve been collating and publishing (since 2014) some necessary / attention-grabbing factors and developments associated to Private Funds like – Indian Family Financial savings Sample, complete investments in financial institution deposits, investments in shares & mutual funds, info on complete financial institution loans, NRI deposits, Small Saving Schemes, Financial institution Deposit & Key Lending rates of interest sample and so forth.

Indian Family Financial savings Sample 2024-25

Households’ Financial savings correspond to the entire revenue saved by households throughout a sure time period. Financial savings and investments in banks, inventory markets, Put up workplace schemes, firm deposits and so on., are thought-about as Monetary Property / Monetary Financial savings. Whereas, the investments in properties (actual property), gold, silver and so on., are Bodily Financial savings / Bodily Property.

Monetary Property Vs Bodily Property : That are the popular belongings by Indian households?

- From 1990 to 2000, Indian households most well-liked to spend money on Monetary belongings to Bodily belongings.

- From 2000 to 2007, extra financial savings had been routed to Bodily belongings.

- Apparently in 2007/08, extra investments had been made in Monetary belongings. This exhibits that retail/small buyers participated in inventory markets when their valuations had been at peak. The markets finally crashed in 2008.

- From 2008 to until 2015, we most well-liked bodily financial savings to monetary financial savings.

- The Gross Home Financial savings of family sector have seen a substantial enhance from Rs 38,44,582 crore in 2018-19 to Rs 54,61,259 crore in 2024.

- The under desk offers us an thought in regards to the gross monetary financial savings throughout 2018-2024.

| Yr | Gross Monetary Financial savings (₹ crore) | Observations |

|---|---|---|

| 2018–19 | 22,63,690 | |

| 2019–20 | 23,24,563 | Elevated from earlier estimates |

| 2020–21 | 30,67,021 | Monetary Financial savings peaked because of the pandemic (Covid), as lockdowns restricted consumption alternatives. |

| 2021–22 | 26,11,974 | Decline from the pandemic peak |

| 2022–23 | 29,27,604 | Recovering from the earlier yr’s dip |

| 2023–24 | 34,30,640 | Whereas the entire monetary belongings elevated, it was paired with a surge in liabilities. This drove down Internet Monetary Financial savings. |

- The proportion of bodily financial savings as a share of GDP declined steadily from 2012-16. The under desk offers us an thought in regards to the financial savings in Bodily Property throughout 2018-2024.

| Yr | Bodily Financial savings (₹ crore) | Observations |

|---|---|---|

| 2018–19 | 23,09,463 | |

| 2019–20 | 22,52,167 | A slight dip in bodily financial savings |

| 2020–21 | 21,35,450 | Monetary Financial savings peaked & Bodily financial savings dropped drastically because of the pandemic (Covid) |

| 2021–22 | 29,68,302 | The development reversed because the financial system reopened. Households channeled their financial savings once more into bodily belongings like real-estate & gold |

| 2022–23 | 36,14,851 | The development reversal continued |

| 2023–24 | 38,44,515 | The shift in direction of bodily belongings continued. The share of bodily financial savings was round 70% in 2023–24, in comparison with internet monetary financial savings at round 30% |

- The financial savings within the type of gold and silver ornaments have elevated from Rs 42,673 crore in 2018-19 to Rs 65,104crore in 2024.

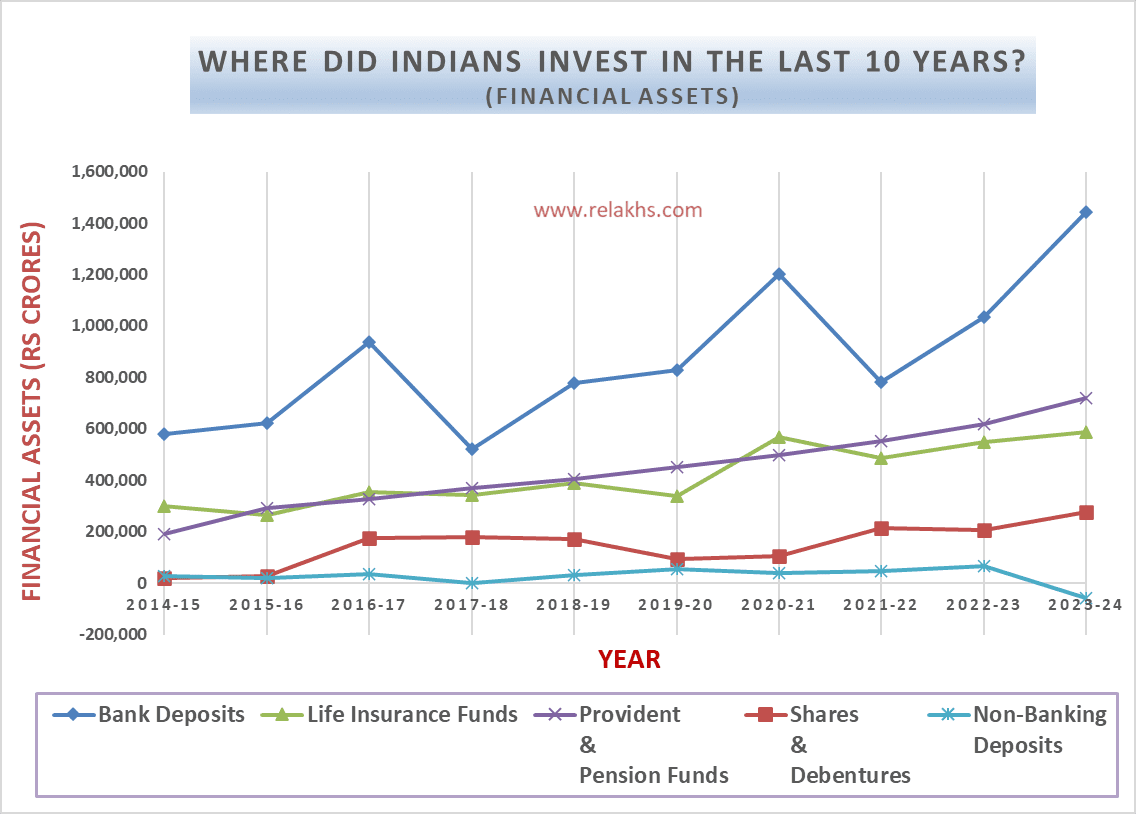

Monetary Property (Financial savings) of the Households (2014-2024)

Allow us to now perceive how the households allotted their financial savings amongst completely different funding choices;

- Fairness and Funding Funds: The share of fairness and funding funds have elevated considerably from Rs 20, 364 cr in 2014 to Rs 2,76,070 cr in 2024.

- Deposits and Foreign money Holdings: The share of deposits and forex holdings has elevated from the lows of 2021-22.

- Pension and Provident Funds: The share of pension and provident funds steadily elevated and has been steady since FY20.

- Life Insurance coverage : The funding in life insurance coverage has reached multi-year highs throughout 2024.

- NBFC Deposits : There have been important NBFC deposit withdrawals throughout 2023-24.

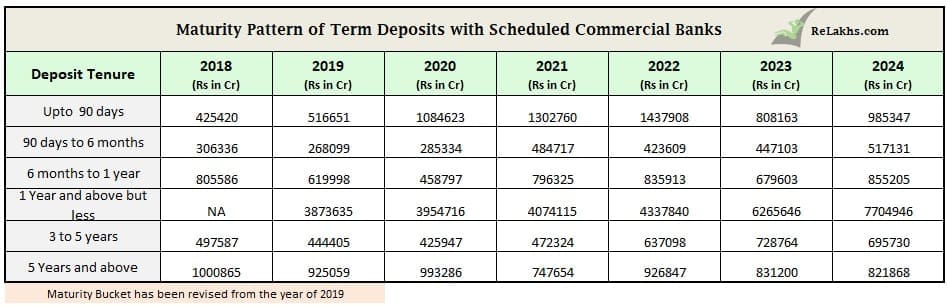

Financial institution Fastened Deposits & Maturity Sample

The above desk offers us an thought in regards to the complete excellent quantity saved in Financial institution Time period Deposits based mostly on the tenure of the deposits. Besides Time period deposits of three to five yeas and above 5 years length, all different time deposits have proven a constructive development in 2024.

Financial institution Deposits by NRIs

Beneath are the excellent NRI Financial institution Deposits (in crores) from 2015 to 2024;

| Yr | NRE Deposits | FCNR Deposits | NRO Deposits |

|---|---|---|---|

| 2015 | 392832 | 268106 | 60059 |

| 2016 | 474068 | 300593 | 67294 |

| 2017 | 539544 | 136173 | 82033 |

| 2018 | 585625 | 143264 | 91848 |

| 2019 | 636491 | 160271 | 105390 |

| 2020 | 676338 | 181451 | 119521 |

| 2021 | 742720 | 148235 | 136428 |

| 2022 | 767881 | 128879 | 162281 |

| 2023 | 787776 | 159199 | 194842 |

| 2024 | 822264 | 214549 | 229459 |

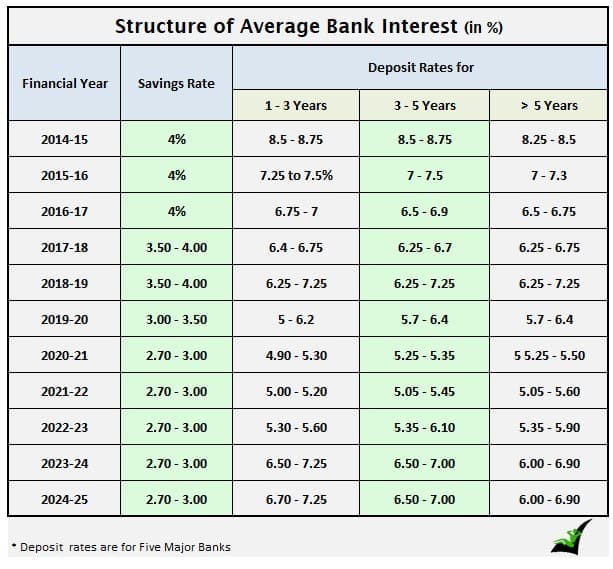

Curiosity Charges sample of Financial institution Deposits (2014 to 2024)

Beneath desk offers us an thought in regards to the deposit charges sample in India during the last 10 years.

In early 2025, the RBI started an easing cycle, decreasing the repo fee in a phased method to stimulate financial development and deal with easing inflation. As of August 2025, a number of banks have adjusted their mounted deposit (FD) rates of interest downwards according to the repo fee cuts.

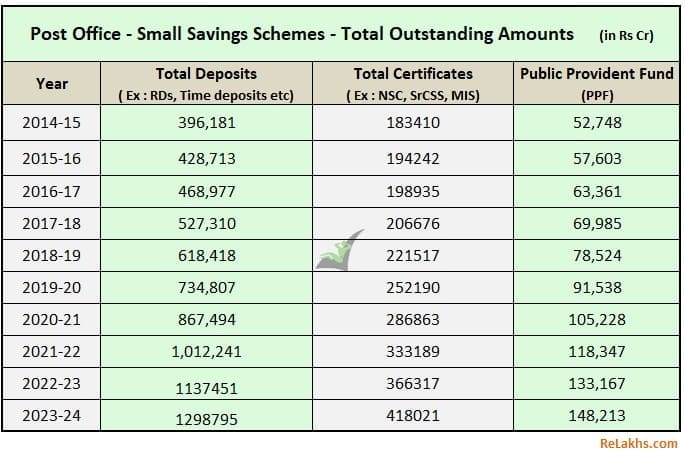

Deposits in Put up workplace Small Financial savings Schemes (SSS)

- Indian households’ financial savings in Put up workplace time deposits and PPF have been growing steadily since 2011.

- Throughout 2012-16 there was a decline in investments in NSCs, KVP certificates and different standard schemes like Senior Citizen Financial savings Schemes or Month-to-month Revenue Scheme (MIS), nevertheless this development was reversed throughout 2016-18.

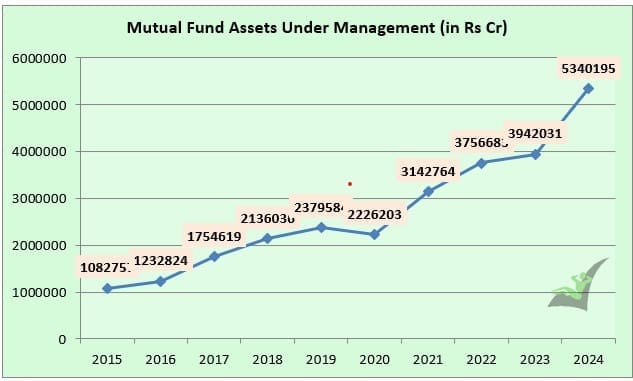

Mutual Fund Schemes : Property Underneath Administration (2014-2024)

There was round 7% decline in AUM of Mutual Funds in India throughout 2019-20 as a consequence of covid influence. Nevertheless, the inventory markets have recovered properly and therefore we are able to discover the research elevate within the AUM of the mutual fund homes. The truth is, there was a 35% enhance in AUM in 2024.

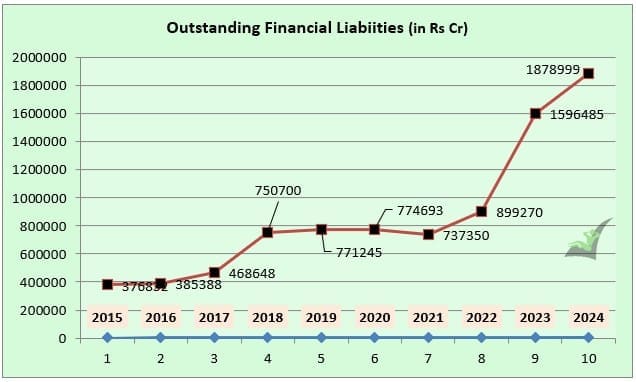

Monetary Liabilities of Indian Households (2024)

- The overall Monetary liabilities (loans & advances) of the Indian family sector had been round Rs 18,78,999 crore throughout 2023-24. This can be a whopping enhance of greater than 200%. This determine was round Rs 8,99,270crore for the FY 2021-22.

- Whereas the entire monetary belongings throughout 2023-24 elevated, it was paired with a surge in liabilities. This drove down the Internet Monetary Financial savings of Indian family.

Although the share of Gross monetary financial savings and bodily financial savings are nearly equal, the surge in monetary liabilities have drove down the online monetary financial savings. The mixture of declining monetary financial savings and rising liabilities has led to a major drop in internet monetary financial savings. Internet monetary financial savings, or the excess after accounting for liabilities, declined by greater than 30% from the pandemic peak.

Causes for concern – Growing family debt burden and monetary fragility, particularly with rising unsecured loans. Challenges for the banking sector, as deposit development lags credit score development.

In conclusion, whereas the share of monetary and bodily financial savings may seem balanced at a look, the rise in monetary liabilities has considerably eroded the online monetary financial savings of Indian households, elevating issues in regards to the long-term financial stability and funding capability of the nation.

I hope you discover this put up informative and helpful. The place do you save and make investments? That are your most well-liked funding avenues? What’s your view on the growing monetary liabilities (loans) of Indian family?

(Put up first printed on : 02-Sep-2025)