{kind=link}

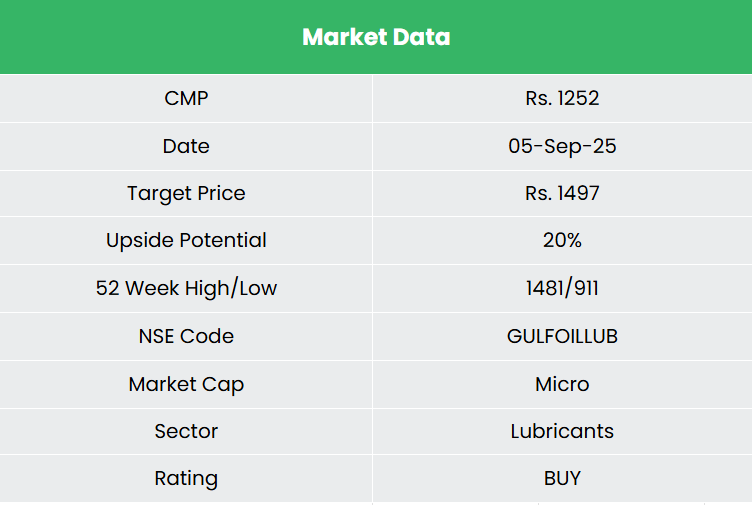

Gulf Oil Lubricants India Ltd – Bolder than Daring

Standing as a distinguished participant within the Indian lubricants business, Gulf Oil Lubricants India Ltd. (GOLIL) is a world-class automotive and industrial lubricants supplier. Included in 2008 and headquartered in Mumbai, the corporate’s enterprise is split into automotive, industrial and exports. As of 30 June 2025, the corporate has two in-house manufacturing services (in Silvassa and Chennai) with a lubricants manufacturing capability of 90,000 KL p.a. (Silvassa), 50,000 KL p.a. (Chennai) and a complete AdBlue manufacturing capability of 1,92,000 KL p.a. With an intensive distribution community, it straight provides merchandise to over 40 Unique Gear Producers (OEMs) and greater than 500 B2B clients spanning completely different industries together with infrastructure, mining, state transport companies and authorities undertakings.

Merchandise and Companies

The corporate has a various portfolio of lubricants together with automotive and industrial lubricants, specialty oils, EV fluids, marine lubricants, and AdBlue in addition to 2-wheeler VRLA batteries.

Subsidiaries: The corporate has 1 subsidiary and 1 affiliate firm.

Funding Rationale

- Strategic Initiatives and Model Energy – The corporate continues to strengthen its place within the Indian market by product innovation, strategic partnerships, and model growth. Strategic tie-ups have been central to its progress, together with a brand new 3-year partnership with Nayara Vitality, India’s largest personal gasoline retailer. This alliance supplies the corporate entry to over 6,500+ shops, considerably enhancing its model visibility and product availability throughout each city and rural markets. Moreover, the corporate renewed and expanded its long-term partnership with Piaggio till 2032, together with new product strains for high-performance 2-wheelers and prolonged collaborations within the industrial car area. These strikes spotlight the corporate’s give attention to deeper OEM integration and wider client engagement. The corporate lately launched a revamped model of its flagship 2-wheeler engine oil, Gulf Delight, with an upgraded API SP formulation and a refreshed model marketing campaign – receiving robust market response and driving progress within the B2C section.

- Capability Enlargement and Product Diversification – The corporate is actively scaling its manufacturing capability to satisfy future demand, focusing on a 70% improve – from 140 million to 240 million litres at its Chennai and Silvassa vegetation, with the complete completion anticipated by March 2027 and a deliberate capex of Rs.55 crore. It additionally maintains a structured annual capex plan of Rs.30 – 40 crore to help ongoing progress. A significant progress vector is its EV infrastructure play by Tirex, a subsidiary targeted on DC quick chargers and now increasing into AC charger manufacturing. Tirex is seeing robust traction in buyer acquisition and goals to double its income yearly, with the aim of turning into a Rs.400 – 500 crore topline enterprise within the subsequent 4 – 5 years. Tirex has turned EBITDA constructive through the quarter with a ~160% improve in income through the interval. On the innovation entrance, the corporate is diversifying into high-potential segments like information heart cooling, having developed two specialised lubricant merchandise – one artificial and one mineral-based – for thermal administration functions. These initiatives show the corporate’s strategic give attention to future-ready options and its readiness to capitalize on the transition towards electrification and energy-efficient applied sciences.

- Q1FY26 – In the course of the quarter, the corporate achieved highest ever quarterly quantity, income, working revenue. Volumes elevated by 11% in comparison with business progress of 3-3.5%. The corporate generated income of Rs.1,016 crore, a rise of 14% in comparison with the Rs.894 crore of Q1FY25. Working revenue improved by 12% YoY to Rs.127 crore in comparison with Rs.113 crore. Web revenue stood at Rs.95 crore as towards the Rs.84 crore of Q1FY25, a rise of 13%.

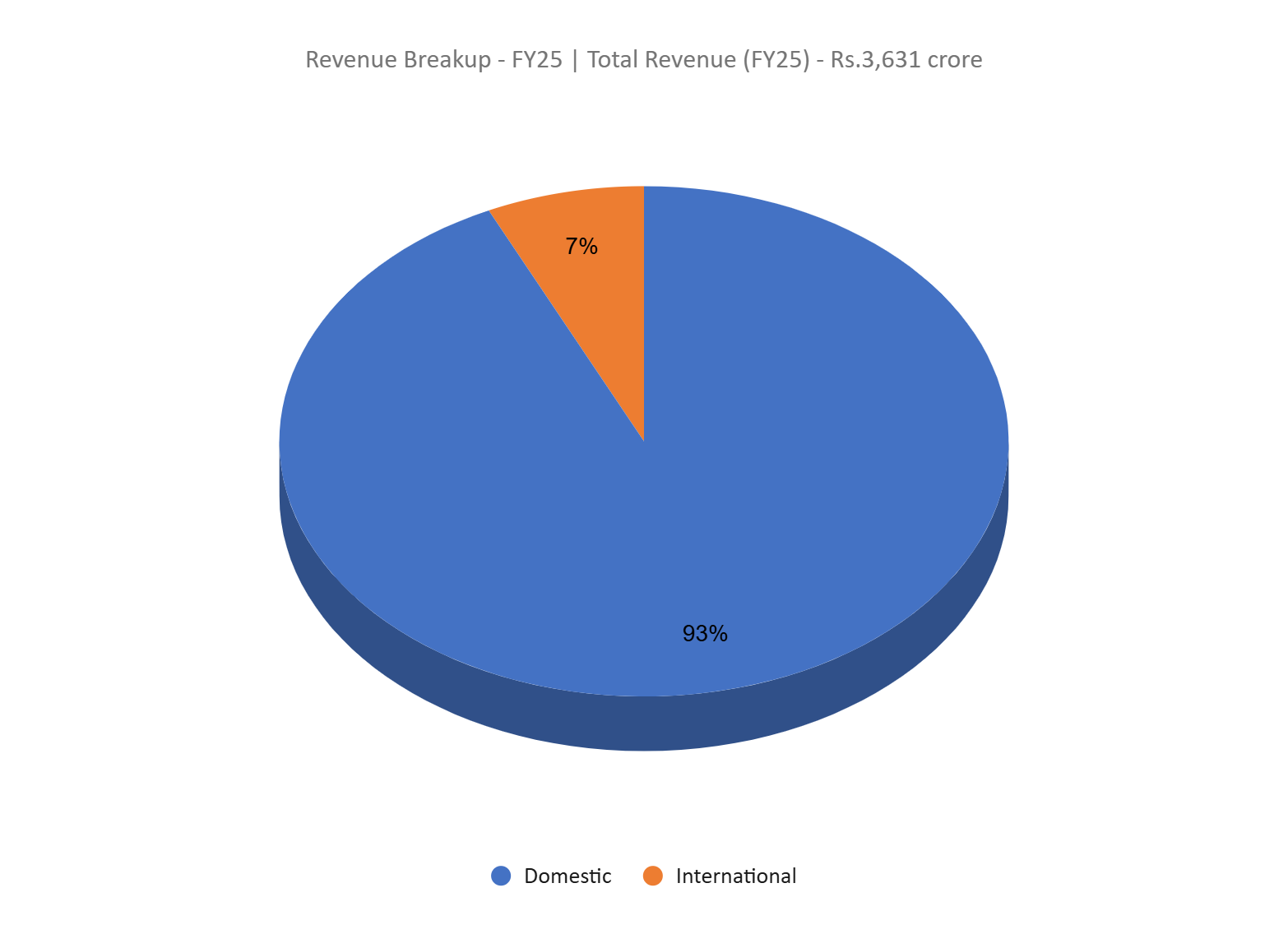

- FY25 – The corporate generated income of Rs.3,631 crore, a rise of 10% in comparison with FY24 income. Working revenue is at Rs.472 crore, up by 12% YoY. The corporate posted internet revenue of Rs.357 crore, a soar of 16% YoY.

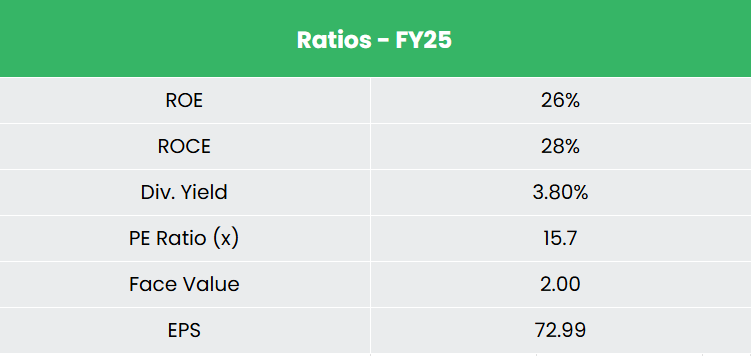

- Monetary Efficiency – The corporate has generated income and PAT CAGR of 18% and 20% over the interval of three years (FY23-25). Common 3-year ROE & ROCE is round 24% and 26% for FY23-25 interval. The corporate has strong capital construction with a debt-to-equity ratio of 0.32.

Business

India’s rising center class, rising incomes, and fast financial growth have made it the world’s third-largest car market, driving robust demand in each the automotive and auto elements sectors. This progress has positioned India as a key manufacturing and export hub, with rising give attention to R&D, electrification, and sustainable mobility. The robust efficiency of the auto sector straight fuels demand for lubricants, particularly in high-growth areas like passenger automobiles, industrial transport, and industrial equipment. Industrial lubricants additionally play a important position throughout sectors resembling development, manufacturing, agriculture, and energy technology. Moreover, tightening environmental rules are accelerating the shift towards premium, low-emission lubricants, creating important alternatives for innovation-led and sustainability-focused gamers within the business.

Progress Drivers

- 100% FDI is allowed underneath the automated route for auto elements sector.

- Authorities of India’s proposals for discount in tax burden is anticipated to spice up spending among the many increasing center class inhabitants.

- Average car penetration ranges relative to the rising inhabitants and rising revenue.

Peer Evaluation

Opponents: Castrol India Ltd, Veedol Company Ltd, and many others.

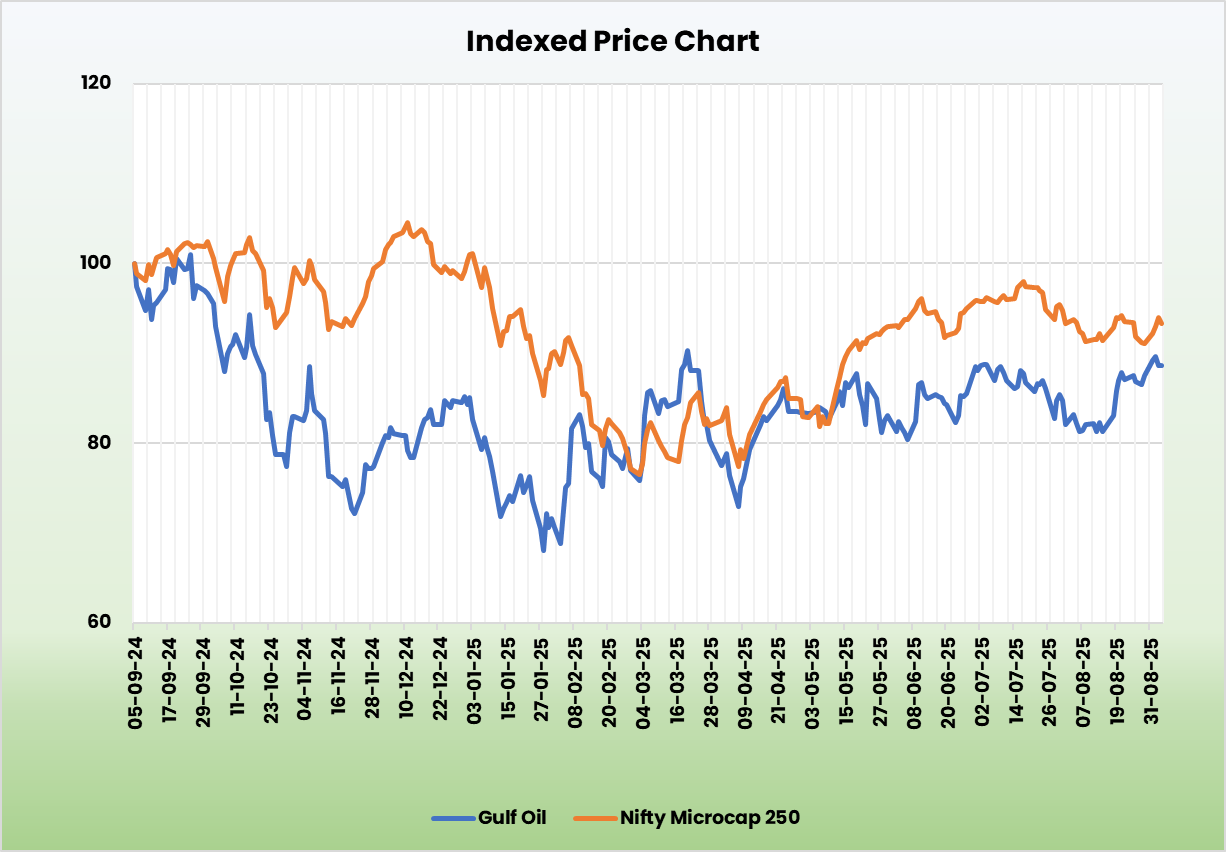

In comparison with the friends, Gulf Oil demonstrates stronger general monetary and operational efficiency, mirrored in its superior gross sales progress and constant returns on capital employed.

Outlook

Gulf Oil presents a compelling funding alternative pushed by its constant outperformance in quantity progress – focusing on 2 – 3x the business fee – whereas sustaining wholesome EBITDA margins steerage within the 12 – 14% vary. The corporate’s strategic give attention to innovation, capability growth, EV infrastructure, and powerful OEM and retail partnerships positions it effectively for long-term progress. Its debt-free stability sheet and strong money reserves of Rs.1,000 crore present monetary power and suppleness to fund future initiatives with restricted leverage danger.

Valuation

With a confirmed monitor file, clear progress roadmap, and give attention to high-potential segments we consider, Gulf Oil stands out as a steady and forward-looking participant within the Indian lubricants business. We advocate a BUY ranking within the inventory with the goal worth (TP) of Rs.1,497, 16x FY27E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry worth to handle potential draw back danger successfully.

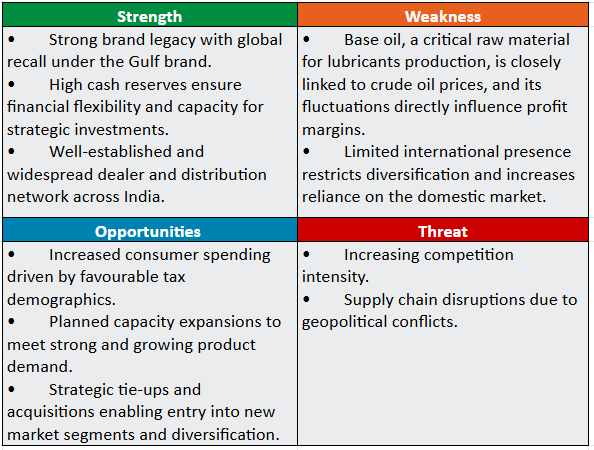

SWOT Evaluation

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please be aware that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles you could like

Put up Views:

63