{kind=link}

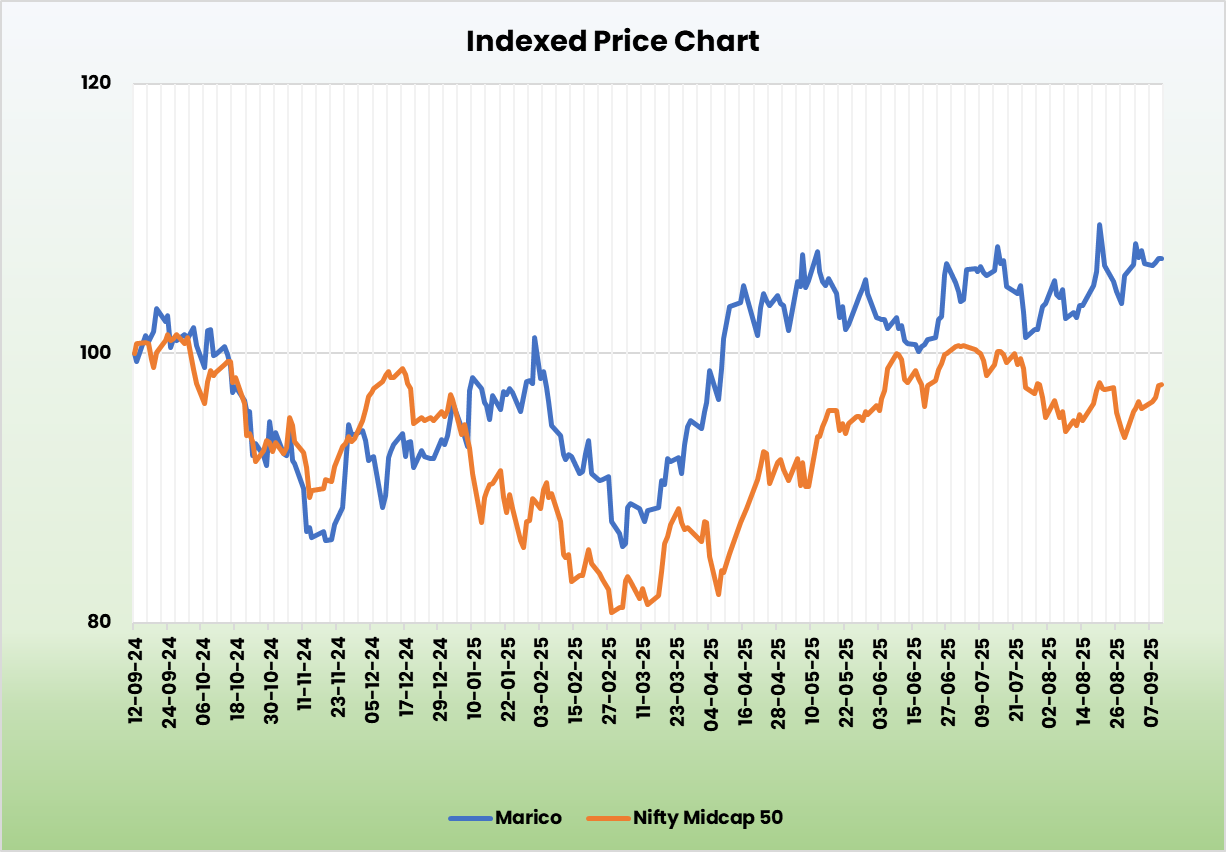

Marico Ltd – Main Shopper Wellness Model

Established in 1988 and headquartered in Mumbai, Marico Ltd. is one in every of India’s main shopper items corporations, with a robust presence within the world magnificence and wellness house. The corporate operates by a sturdy manufacturing infrastructure comprising 6 home and eight worldwide amenities, catering to numerous shopper wants. The corporate’s well-known manufacturers embrace Parachute, Saffola, Hair & Care, Nihar Naturals, Livon, Set Moist, Mediker, and Revive in India, together with worldwide manufacturers akin to Fiancée, HairCode, Caivil, Black Stylish, and X-Males. Marico boasts an enormous distribution community of over 7,500 stockists, reaching greater than 5.8 million stores throughout each city and rural India. The corporate additionally maintains a robust presence in fashionable commerce and e-commerce platforms, enabling entry to over 60,000 villages, thereby guaranteeing deep market penetration and shopper attain.

Merchandise and Providers

The merchandise supplied by the corporate might be majorly categorised underneath classes akin to coconut oil, refined edible oils, worth added hair oils, leave-in hair conditioners, male grooming and packaged meals, amongst others.

Subsidiaries: As of FY25, the corporate has 21 subsidiaries and no different associates/joint ventures.

Funding Rationale

- Established manufacturers driving resilient efficiency – Marico’s core portfolio continues to exhibit resilience and development throughout key classes. Parachute, Saffola Oils and the Worth-Added Hair Oils (VAHO) phase stay robust contributors, marking a price development of 31%, 28% and 13% respectively throughout Q1FY26. Regardless of inflationary pressures, Parachute volumes remained secure, with the corporate taking calibrated value hikes in response to rising copra prices. The Meals enterprise, anchored by manufacturers like Saffola, True Parts, and Plix marked a sturdy worth development of 20% in the course of the quarter. The Saffola franchise is increasing with profitable new product launches akin to Saffola Twin Seed Chilly Pressed Oils and Saffola Cuppa Oats, whereas Saffola Oats continues to guide its class with double-digit development. Internationally, the corporate continues to ship double-digit fixed foreign money development, with premium portfolios now accounting for 29% of worldwide income and displaying strong traction in markets like Bangladesh and MENA. Alternate channels together with e-commerce, fashionable commerce, and fast commerce stay key development enablers, significantly in premium and health-oriented segments.

- Enlargement plans – Marico is actively investing in strategic development areas, with a pointy give attention to premiumization, digital-first manufacturers, and meals. The corporate elevated its stake in Satiya Nutraceuticals, proprietor of Plix, which is displaying accelerated momentum. The corporate additionally continues to broaden its Meals enterprise aggressively, with expectations of 25%+ development in FY26. The corporate not too long ago elevated its stake in HW Wellness, proprietor of True Parts, making it a 100% wholly owned subsidiary of the corporate. To enhance its portfolio growth, it’s investing closely in Common Commerce and distribution infrastructure. By way of Mission SETU, the corporate is enhancing its direct distribution footprint from 1 million to 1.5 million retail shops by FY27, with Rs.80 – 100 crore earmarked for the rollout. This initiative is already displaying early indicators of traction, with extra significant influence anticipated in H2FY26.

- Q1FY26 – Through the quarter, the corporate reported income of Rs.3,259 crore, reflecting a 23% YoY development over Rs.2,643 crore in Q1FY25. Working revenue rose by 5% YoY to Rs.655 crore, in comparison with Rs.626 crore within the corresponding quarter final 12 months. Internet revenue elevated by 9% YoY, coming in at Rs.504 crore versus Rs.464 crore in Q1FY25. The India enterprise recorded a robust 27% YoY income development, pushed by a 9% enhance in home volumes. In the meantime, the worldwide enterprise posted a 19% YoY development in fixed foreign money phrases.

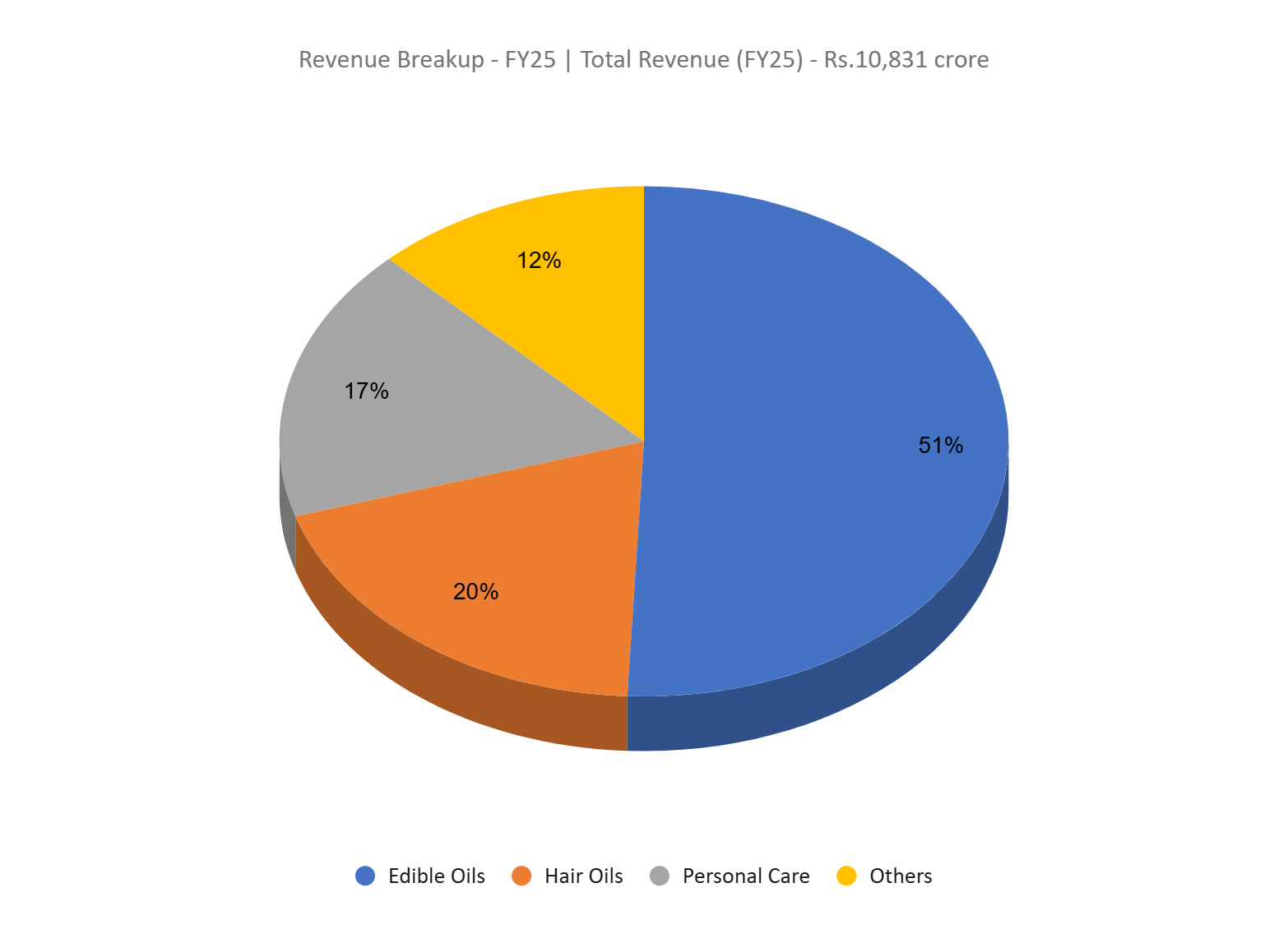

- FY25 – Through the monetary 12 months, the corporate generated income of Rs.10,831 crore, a rise of 12% in comparison with the FY24 income. Working revenue is at Rs.2,139 crore, up by 6% YoY. The corporate reported internet revenue of Rs.1,593 crore, a rise of 8% YoY.

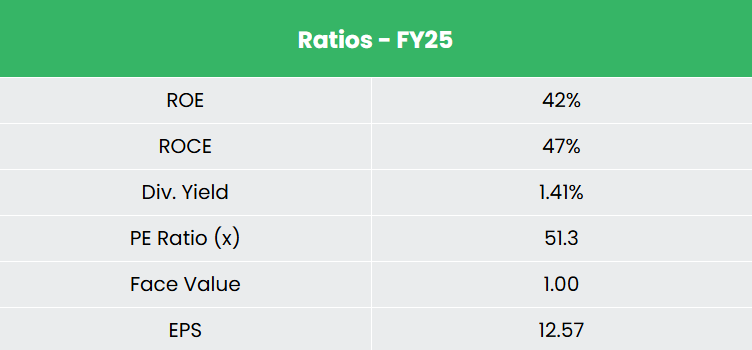

- Monetary Efficiency – The corporate has generated income and internet revenue CAGR of 4% and 10% over the interval of three years (FY23-25), whereas the TTM income and internet revenue development is at 17% and 10%. The common 3-year ROE & ROCE is round 39% and 43% every for the FY23-25 interval. The corporate has a robust steadiness sheet with a sturdy debt-to-equity ratio of 0.14.

Business

The Indian FMCG sector is witnessing strong development, pushed by rising incomes, urbanization, and evolving shopper preferences. The meals processing market is predicted to develop at a CAGR of 9.5% to succeed in US$ 547.3 billion by 2028, whereas the net grocery market is projected to surge at a CAGR of 32.7% by 2032. Fast commerce, fuelled by demand for comfort and digital adoption, has seen FMCG gross sales develop 50 – 100% in FY25 alone. E-commerce continues to broaden, supported by improved digital infrastructure and cost methods. Rural consumption is rising, with rising demand for branded merchandise and a shift in direction of organized retail. Concurrently, India’s Magnificence and Private Care (BPC) market, presently valued at US$ 21 billion, is predicted to develop at 10 – 11% CAGR to succeed in US$ 34 billion by 2028, making it the fastest-growing BPC market globally.

Development Drivers

- The Union Finances 2025 – 26 provides a robust impetus to shopper spending by elevated allocations and tax reforms, immediately benefiting FMCG demand.

- Authorities proposals to scale back the tax burden are anticipated to reinforce disposable incomes, encouraging larger consumption among the many rising middle-class inhabitants

- Evolving shopper life, coupled with larger entry to digital platforms and e-commerce, are accelerating demand for branded and convenience-driven FMCG merchandise.

Peer Evaluation

Rivals – Patanjali Meals Ltd, AWL Agri Enterprise Ltd, and so on.

In comparison with its friends, Marico demonstrates extra environment friendly capital allocation, mirrored in its superior monetary efficiency. The corporate additionally enjoys considerably larger working margins of 19%, outperforming Patanjali (5%) and AWL’s (3%), highlighting its operational power and premium portfolio combine.

Outlook

Marico is on a robust development trajectory, with administration guiding for 25% income development in FY26 and aiming to double income from Rs.10,000 crore in FY25 to Rs.20,000 crore by FY30. The corporate expects to maintain double-digit income and revenue development, supported by 6 -7% base quantity development and a pointy give attention to high-potential segments. The Meals enterprise is projected to develop 25% in FY26, with vital headroom in Common Commerce. Current acquisitions – Plix and True Parts – have scaled quickly and turned EBITDA-profitable, anticipated to cross a mixed Rs.1,000 crore ARR in FY26. Strategic initiatives like Mission SETU are enhancing distribution, visibility, and profitability.

Valuation

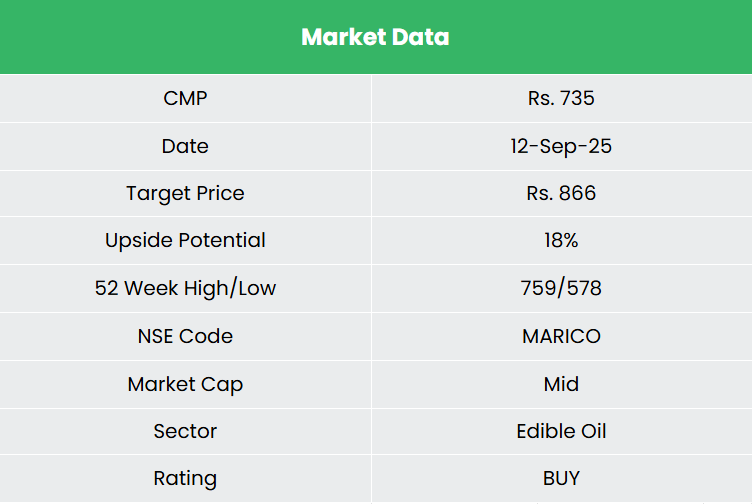

We imagine Marico presents a compelling funding alternative, pushed by its strategic give attention to strengthening distribution channels and its monitor file of constant quantity development. We advocate a BUY ranking within the inventory with the goal value (TP) of Rs.866, 41x FY27E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back threat successfully.

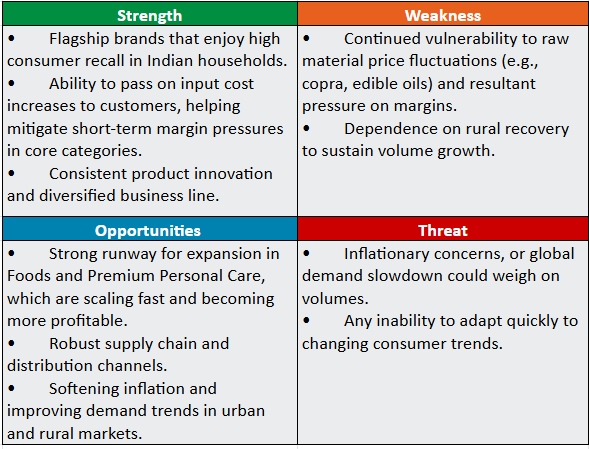

SWOT Evaluation

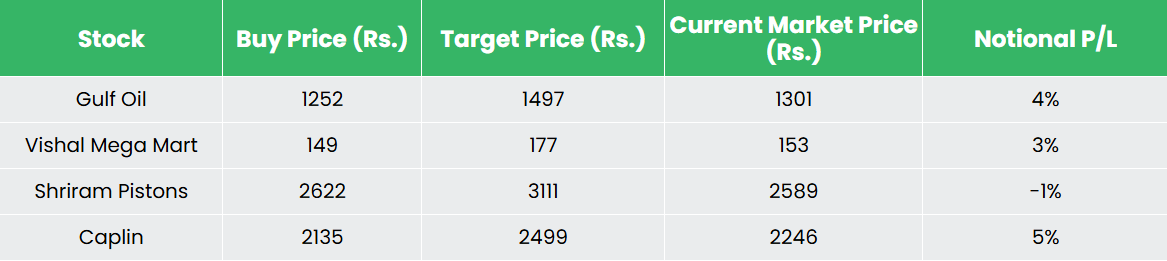

Recap of our earlier suggestions (As on 12 September 2025)

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please observe that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles chances are you’ll like

Put up Views:

78