{kind=link}

CEAT Ltd – Pushed by Objective, Powered by Progress

Based in 1958 and headquartered in Mumbai, CEAT Ltd. is one among India’s premier tyre producers. The corporate serves a various vary of segments, together with two- and three-wheelers, passenger and utility autos, industrial autos, and off-highway autos. As a flagship entity of the RPG Group, the corporate has a robust world footprint, working in over 110 international locations, with key markets spanning the US, Latin America, Africa, the Center East, India, Southeast Asia, and Europe. Its in depth distribution community includes greater than 5,700 sellers, over 61,000 sub-dealers, and 1,115+ shops throughout India. CEAT operates six manufacturing amenities and gives a large product portfolio with over 2,300 distinctive tyre variants, backed by 52 granted patents.

Merchandise and Companies

The corporate manufactures and provides a various vary of tyres, tubes and flaps for truck and buses, 2/3W, passenger vehicles and utility autos, off freeway, LCV and others.

Subsidiaries: As of FY25, the corporate has 10 subsidiaries and 1 three way partnership.

Funding Rationale

- Strategic alliances – The corporate lately accomplished the acquisition of Michelin Group’s CAMSO Development Compact Line (CCL) enterprise, marking a strategic milestone in its transformation into a world Off-Freeway Tyre (OHT) chief. The acquisition includes two superior manufacturing amenities in Sri Lanka (Midigama and Kotugoda) and consists of world rights to the CAMSO model, below a three-year licensing association following which everlasting possession will switch to CEAT. The CAMSO enterprise recorded ~US$213 million in CY2023 revenues and at present operates at ~60% capability utilisation, which CEAT expects to ramp up within the coming quarters. The transaction is anticipated to be margin accretive and to spice up CEAT’s topline by 10 – 15% within the medium time period. Importantly, with CAMSO’s sturdy model fairness throughout Europe and North America, CEAT features entry to 40+ world OEMs and premium distributors, considerably enhancing its worldwide attain and accelerating its imaginative and prescient to be a world chief in Off-Freeway mobility.

- Capability additions – CEAT is enterprise calibrated capability expansions throughout key product segments to fulfill rising home and export demand. The corporate commissioned a brand new Truck & Bus Radial (TBR) facility in FY25 with an preliminary capability of 1,500 tyres/day, and plans to scale output by an extra 2,000 models/day at its Chennai plant by FY26. Passenger Automobile Radial (PCR) capability at Chennai can be slated to rise 30–40% over the identical interval. In the meantime, a Rs.500 crore funding on the Nagpur plant will improve capability by ~30%, and growth at Ambernath will assist export-led progress. These initiatives are anticipated to strengthen CEAT’s aggressive positioning throughout passenger, industrial, and farm tyre segments, enabling it to capitalize on the structural uptick in alternative and OEM demand.

- Q2FY26 – Throughout the quarter, the corporate generated income of Rs.3,773 crore, a rise of 14% in comparison with the Rs.3,305 crore of Q2FY25 – backed by a sturdy progress within the OEM and worldwide segments. Working revenue elevated from Rs.368 crore of Q2FY25 to Rs.511 crore of Q2FY26, a progress of 39%. Gross and EBITDA margins expanded on account of working leverage and value efficiencies. The corporate reported internet revenue of Rs.186 crore, a rise by 52% YoY in comparison with Rs.122 crore of the corresponding interval of the earlier 12 months.

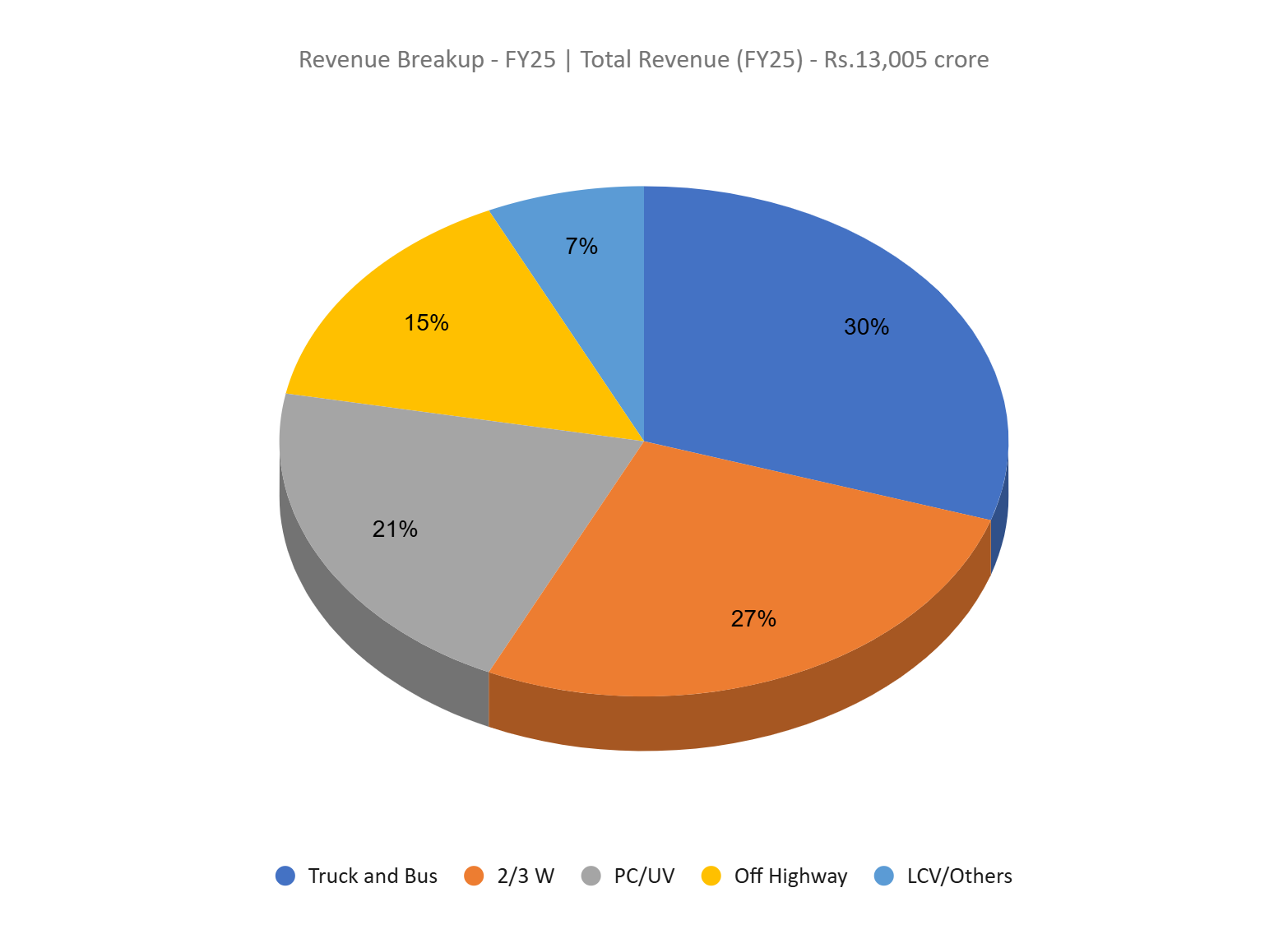

- FY25 – Throughout the FY, the corporate generated income of Rs.13,005 crore, a rise of 11% in comparison with the FY24 income. Working revenue is at Rs.1,496 crore, down by 11% YoY. The corporate reported internet revenue of Rs.473 crore, a degrowth of 26% YoY. The de-growth was because of the world uncertainties on account of tariff and non-tariff conditions in Q4FY25.

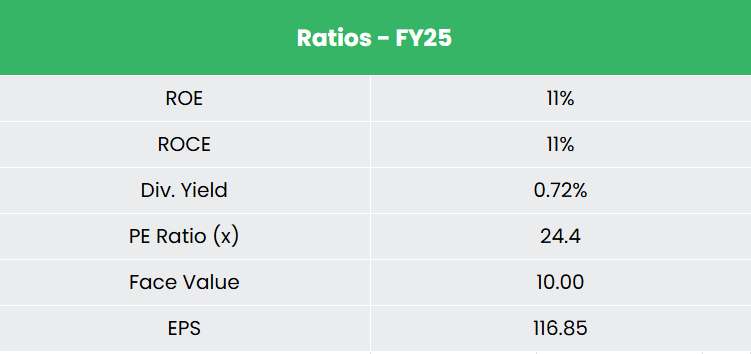

- Monetary Efficiency – The three-year income and internet revenue CAGR stands at 12% and 79% between FY23-25. Common 3-year ROE and ROCE is round 12% and 15% for FY23-25 interval. Debt to fairness ratio is at 0.49.

Business

India’s rising working inhabitants and increasing center class proceed to be important drivers of demand within the automotive sector. Because the world’s third-largest car market by each worth and quantity, India is quickly establishing itself as a key world hub for auto part sourcing. The trade at present exports over 25% of its manufacturing yearly, with export values projected to achieve Rs.8,54,700 crore (US$ 100 billion) by 2030. Current years have seen India emerge because the fastest-growing main financial system globally, supported by rising incomes, elevated infrastructure investments, and beneficial manufacturing incentives. These elements have collectively accelerated progress within the car sector, making it an important pillar of the nation’s broader financial growth. The surge in home and worldwide demand has additionally fuelled the expansion of authentic tools producers (OEMs) and auto part producers, serving to India develop deep trade experience.

Development Drivers

- 100% FDI is allowed below the automated route for auto parts sector.

- The discount within the tax burden within the 2025-26 Union Finances is anticipated to spice up spending among the many increasing center class inhabitants.

- Diminished GST charges on vehicles and tyres will decrease prices for shoppers, boosting demand and driving progress in each new car gross sales and tyre replacements.

Peer Evaluation

Opponents: MRF Ltd, Apollo Tyres Ltd, and many others.

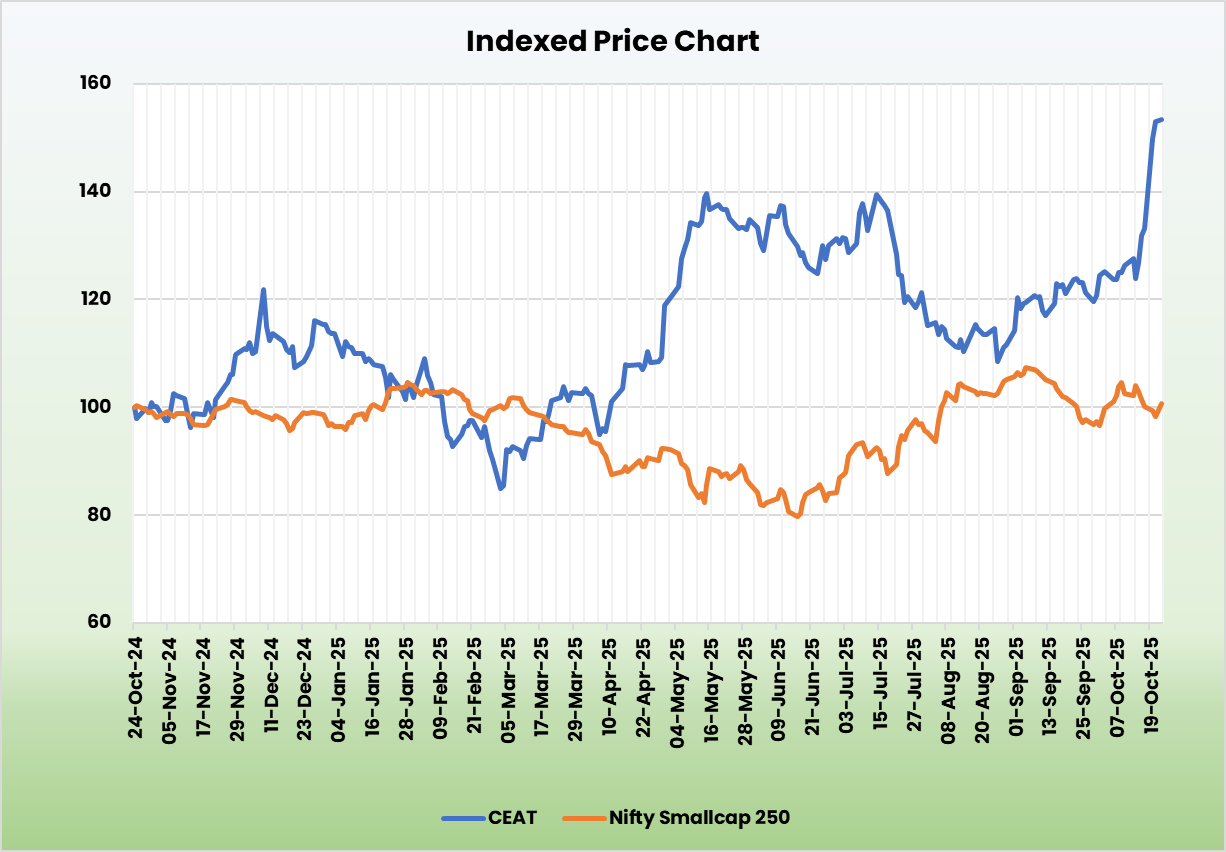

In comparison with its opponents, CEAT seems fairly valued and demonstrates stronger capital allocation effectivity, as mirrored in its efficiency metrics and gross sales progress.

Outlook

CEAT’s progress outlook stays constructive, supported by the CAMSO acquisition, ongoing capability expansions, and wholesome demand throughout OEM and alternative segments. The CAMSO transaction enhances CEAT’s world presence within the premium Off-Freeway Tyre market and is anticipated to be margin accretive within the medium time period. Q2FY26 efficiency mirrored sturdy topline progress and margin enchancment, indicating working leverage advantages. Regardless of near-term headwinds in FY25 from world commerce disruptions, steadiness sheet metrics stay wholesome with prudent leverage and bettering returns. With deliberate capex of Rs.1,000 crore in FY26, CEAT is positioned to ship regular volume-led progress and margin stability over the medium time period.

Valuations

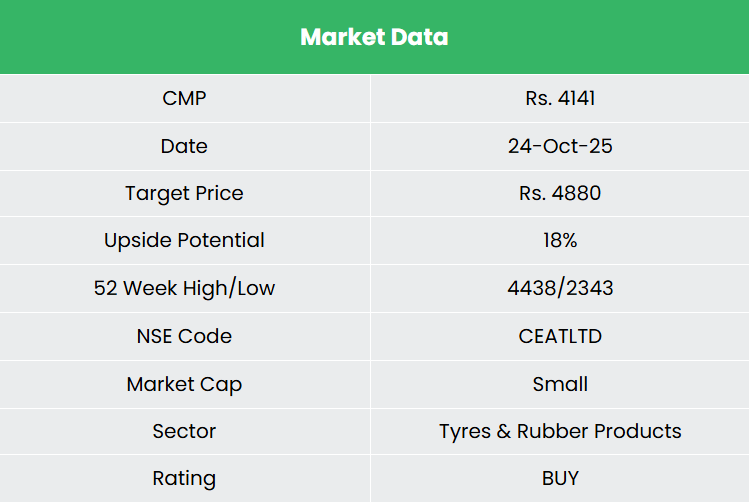

With a robust market place, increasing capability base, and bettering model fairness, we imagine CEAT is properly positioned to learn from the anticipated upcycle in car demand. We suggest a BUY ranking within the inventory with the goal value (TP) of Rs.4,880, 26x FY27E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back danger successfully.

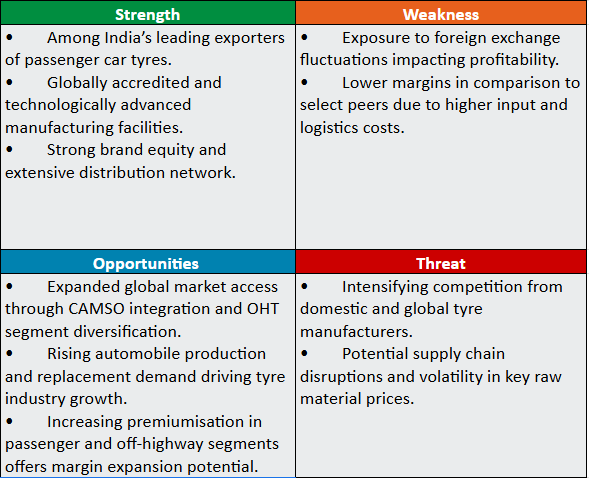

SWOT Evaluation

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please word that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles you might like

Submit Views:

39