{kind=link}

Utilizing historic knowledge on funds to make assumptions about future efficiency includes accurately decoding the tendencies. Over the previous six years, the U.S. has skilled an awfully uncommon interval:

- COVID bear market (01/2020 – 03/2020) with Quantitative Easing

- Federal funds deficit rising from 4.5% of GDP to six.3% (2019 to 2025) together with Gross Federal Debt to GDP rising from 105% of GDP to 119% at present

- Rising Inflation (05/2020 – 05/2022)

- The Nice Normalization bear market (02/2022 – 09/2022)

- Rising charges (03/2022 – 07/2023),

- Quantitative Tightening (11/2022 – ongoing)

- The debasement commerce with gold and cryptocurrencies rising (01/2023-ongoing)

- Excessive fairness valuations (12/2023 – ongoing)

- Federal Reserve reducing short-term rates of interest (09/2024 – ongoing)

- Unprecedented improve in tariffs (04/2025 – ongoing) adopted by the April correction

Through the subsequent six years, we’ll in all probability expertise one other bear market and modest to average inflation. Rates of interest are prone to proceed falling within the short-term, however not as little as the last decade following the monetary disaster due to much less Quantitative Easing and better deficits and nationwide debt. Excessive valuations are a headwind to fairness returns, and excessive rates of interest are a tailwind for bond returns. In January 2020, earlier than the beginning of the COVID bar market, the price-to-earnings ratio of the S&P 500 was an elevated 26 and is presently 31. I consider that the total COVID Cycle from January 2020 to December 2021 and 2025 are extra consultant of market circumstances for the following six years than the interval from January 2022 to December 2024.

Refining My Goal Portfolio

On this article, I discover how various investments and blended asset funds with versatile methods can be utilized to develop a conservative portfolio. To guage funds, I chosen thirty-six funds in twenty-three totally different Lipper Classes that had good risk-adjusted efficiency throughout the full COVID cycle and 2025. I created an optimizer utilizing Excel Solver to maximise the Martin Ratio for the total COVID cycle with constraints for portfolio focus, minimal returns, drawdowns, yields, allocation to “junk bonds”, and consistency throughout the person years and bear markets.

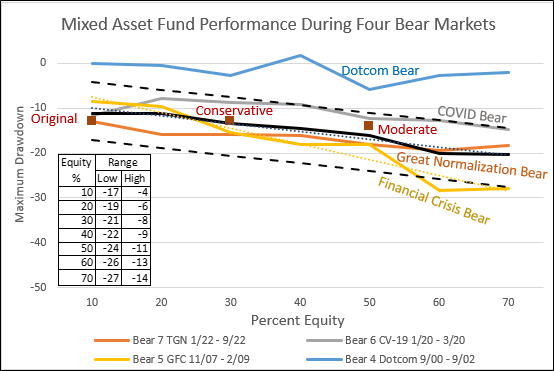

Determine #1 reveals the efficiency throughout the previous 4 bear markets by allocation to shares for the entire 461 blended asset funds within the Lipper international dataset with at the very least six years of historical past. Word that the severity of the bear market has a bigger affect on the portfolio efficiency than the of the inventory to bond ratio.

The 2 black dashed traces present a spread of possible most downturns for the three bear markets, excluding the dotcom bear market, which was related to a light recession. The three maroon squares are the utmost drawdowns of the “Conservative” and “Reasonable” portfolios that I created and the goal portfolio that I described final month in Placing My Conservative Retirement Portfolio on Cruise Management. The 2 portfolios created for this text had low to common drawdowns.

Determine #1: Combined Asset Fund Drawdowns Throughout 4 Bear Markets

Supply: Creator Utilizing MFO Premium fund screener and Lipper international dataset.

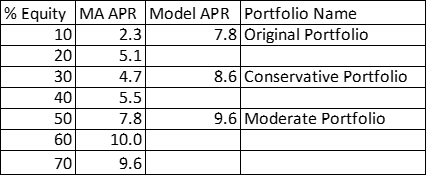

Desk #1 reveals the common annualized returns over the previous six years for the blended asset funds and the “Conservative”, “Reasonable”, and authentic goal portfolio. The 2 new portfolios outperformed each the blended asset funds and the unique goal portfolio.

Desk #1: Combined Asset Fund Returns for Previous Six Years

Supply: Creator Utilizing MFO Premium fund screener and Lipper international dataset.

Assessing Market Threat

I’m presently studying “A Crash Course on Crises: Macroeconomic Ideas for Run-Ups, Collapses, and Recoveries” by Princeton College economics professor Markus Okay. Brunnermeier and London Faculty of Economics professor Ricardo Reis, which researches the interrelationship between monetary markets and the financial system throughout a disaster. They describe a part of their viewers to be “members of the knowledgeable public wanting to soak up a number of the ideas that must be guiding each macroeconomic and monetary coverage.”

The e-book comprises some great insights into investing habits, akin to “Why don’t different, extra refined traders, lean in opposition to the bubble, stopping it from arising within the first place?” They proceed, “These traders attempt to forecast how lengthy the bubble will persist, which is ruled by the buying and selling habits of the opposite (refined) traders.” I’ve no illusions that I can predict the habits of different refined traders.

As described by Hyman Minsky, many crises are preceded by some kind of innovation (akin to synthetic intelligence) adopted by lengthy intervals of value will increase, hypothesis, and leverage. These are adopted by a interval of instability and merchants changing into risk-averse and de-leveraging. Inventory market price-to-earnings ratios have been round 18 earlier than the 1929 inventory market crash, peaked at 34 previous to the bursting of the dotcom bubble, hit 21 previous to the beginning of the monetary disaster, and at the moment are at an elevated 31.

There are often “triggering occasions” that set off chain reactions between asset markets and monetary markets that decide the severity of corrections and whether or not a macro-financial disaster outcomes. On the Nationwide Affiliation for Enterprise Economics, Federal Reserve Chairman Jerome Powell mentioned, “When COVID-19 struck in March 2020, the financial system got here to a close to standstill and monetary markets seized up, threatening to rework a public well being disaster right into a extreme, extended financial downturn.” The stage is about for a correction, and there are many potential “triggering occasions” akin to a slowing financial system, rising inflation, potential provide chain disruptions, and geopolitical threat.

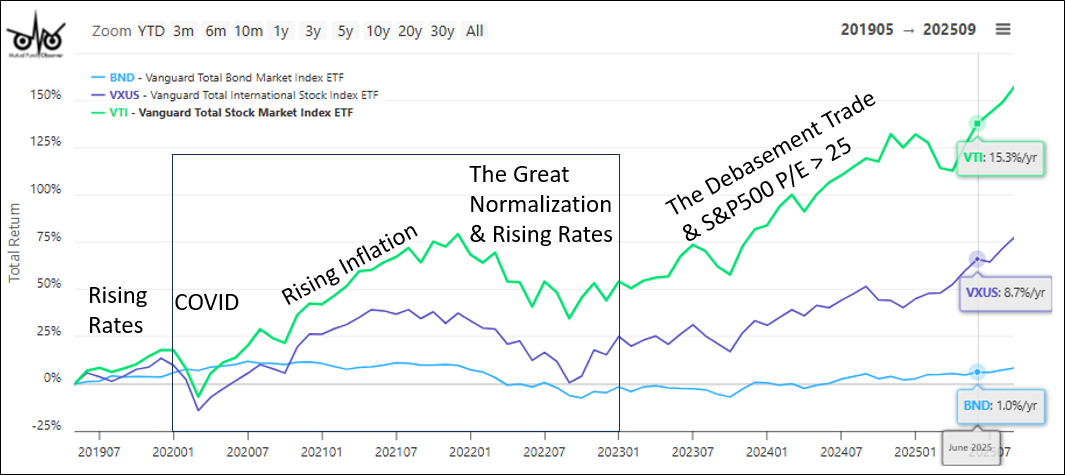

The COVID and Nice Normalization Full Cycles

Determine #2 represents the investing atmosphere for the previous six years. Fiscal and financial stimulus contained the financial fallout from the COVID bear market lasting from January 2020 via March of that yr, however Private Consumption Worth inflation rose from a half p.c following the COVID bear market to almost seven p.c by January 2022. Charles Boccadoro described The Nice Normalization (TGN) wherein rates of interest normalized to increased charges, hurting bond efficiency. The TGN bear market lasted from January 2022 to September of that yr. By December 2023, the price-to-earnings ratio had crossed the excessive valuation stage of $25 per greenback of earnings. The debasement commerce is partly the results of traders and international central banks shopping for gold and the elevated acceptance of cryptocurrency. I consider that the greenback will weaken however not get replaced as the worldwide reserve forex, and the debasement commerce is overbought.

Determine #2: The COVID and Nice Normalization Full Cycles

Supply: Creator Utilizing MFO Premium fund screener and Lipper international dataset.

The complete COVID Cycle was from January 2020 to December 2021 and consists of the COVID bear market and inflation. I count on cycles of bear markets and inflation to be extra frequent within the coming decade than within the decade following the monetary disaster. Charges are excessive, so “The Nice Normalization” of rising charges is unlikely to happen to such extremes for a few years. Lastly, valuations are presently excessive and extra prone to fall than rise both over time or in a correction with a “triggering occasion”.

Portfolio Outcomes

I arrange my Excel optimizer for each the Conservative and Reasonable portfolios to maximise the Martin Ratio for the January 2020 to December 2021 interval by altering allocations to 36 funds with constraints that I needed to have drawdowns of lower than 9 p.c for each the COVID and TGN bear markets. Most allocations have been set for Different, Bond, Fairness, and Combined Asset fund sorts to make sure diversification. The Conservative portfolio has extra constraints of getting yields at the very least 4% with lower than 13% allotted to decrease high quality “junk bonds”.

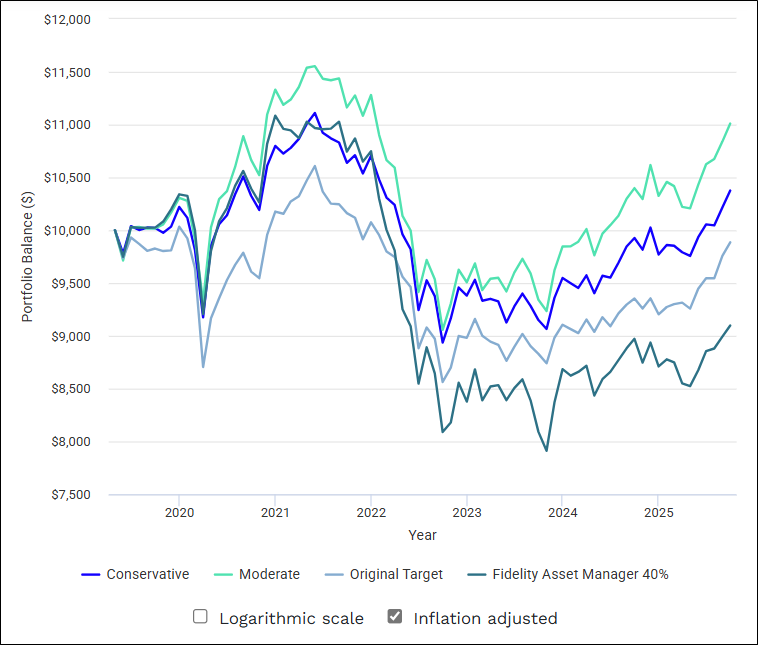

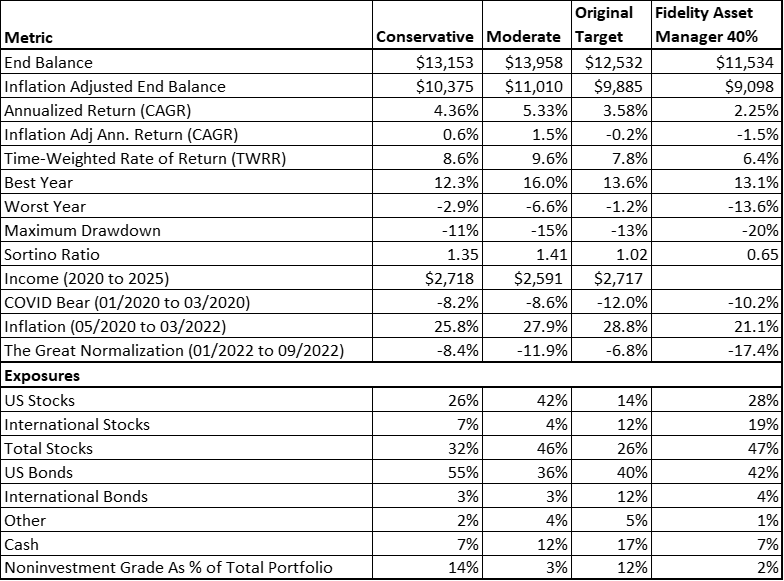

Determine #3 comprises the inflation-adjusted outcomes from Portfolio Visualizer assuming 4% annual withdrawals for the Conservative, Reasonable, and Unique Goal Portfolio in comparison with the Constancy Asset Supervisor 40% (FFANX), which is an effective international blended asset fund. The hyperlink is offered right here. The Conservative and Reasonable portfolios had related returns via 2023, with the Reasonable portfolio having increased volatility. Each beat inflation over the six years after adjusting for withdrawals. Through the interval of rising valuations and the debasement commerce, the Reasonable Portfolio has outperformed. Each outperformed the Unique Goal Portfolio from my final article due to a wider number of funds into consideration, enhancements in methodology, and a rise within the most allocation for a fund from 10% to fifteen%. All three outperformed the 40/60 baseline fund, which was negatively impacted throughout the rising charges interval.

Determine #3: Conservative and Reasonable Portfolio Development – Six Years

Supply: Creator Utilizing Portfolio Visualizer

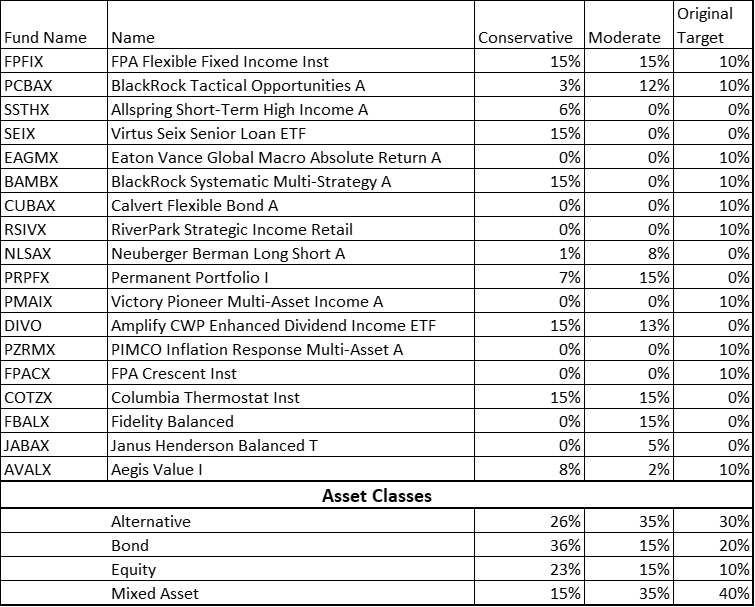

Desk #2 comprises the ensuing allocations with the funds sorted from the bottom Ulcer Ratio over the previous six years to the best. I personal shares in FPFIX/FFIRX, PCBAX, PMAIX, PZRMX, and AVALX. It would take a few years to fill out the remainder of the portfolio, relying upon money flows, and I’ll lean in the direction of the much less dangerous funds subsequent.

Desk #2: Portfolio Allocations

Supply: Creator Utilizing MFO Premium fund screener and Lipper international dataset.

Desk #3 comprises the portfolio metrics for the interval Might 2019 to September 2025 from Portfolio Visualizer. Annualized returns are after withdrawals, whereas Time-Weighted Price of Return displays funding efficiency.

Desk #3: Portfolio Efficiency

Supply: Creator Utilizing Portfolio Visualizer

Fund Evaluation

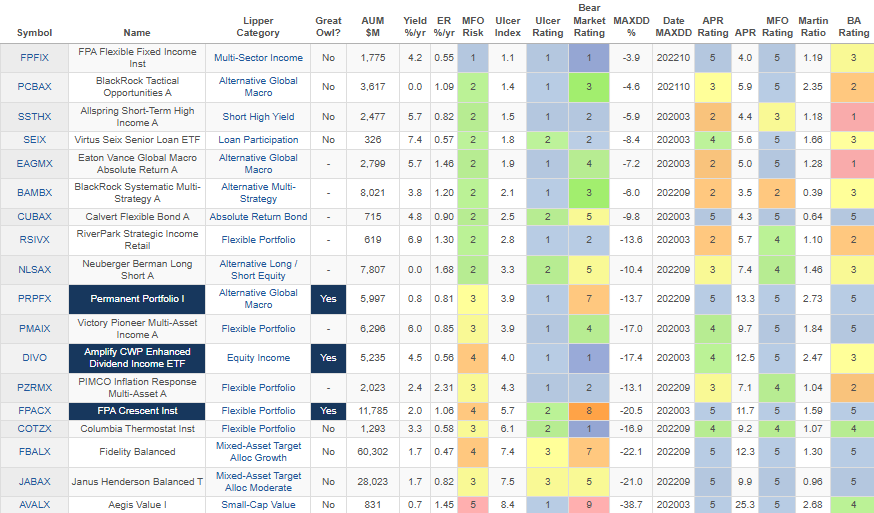

Desk #4 comprises the metrics and scores from MFO for the funds for the previous six years. They’re sorted from the bottom Ulcer Index, which measures the depth and period of drawdowns from the bottom to the best. MFO Threat is predicated on the Ulcer Index evaluating all funds, whereas the Ulcer Score is for funds throughout the similar class friends. Martin Ratio is the risk-free return divided by the Ulcer Index. The MFO Score is predicated on the Martin Ratio for funds throughout the similar Lipper Class. The Batting Common Score (BA) is predicated on the proportion of the months {that a} fund beat its friends. One takeaway is that a number of the funds outperformed throughout down markets however lagged friends total.

Desk #4: Fund Metrix – Six Years

Supply: Creator Utilizing MFO Premium fund screener and Lipper international dataset.

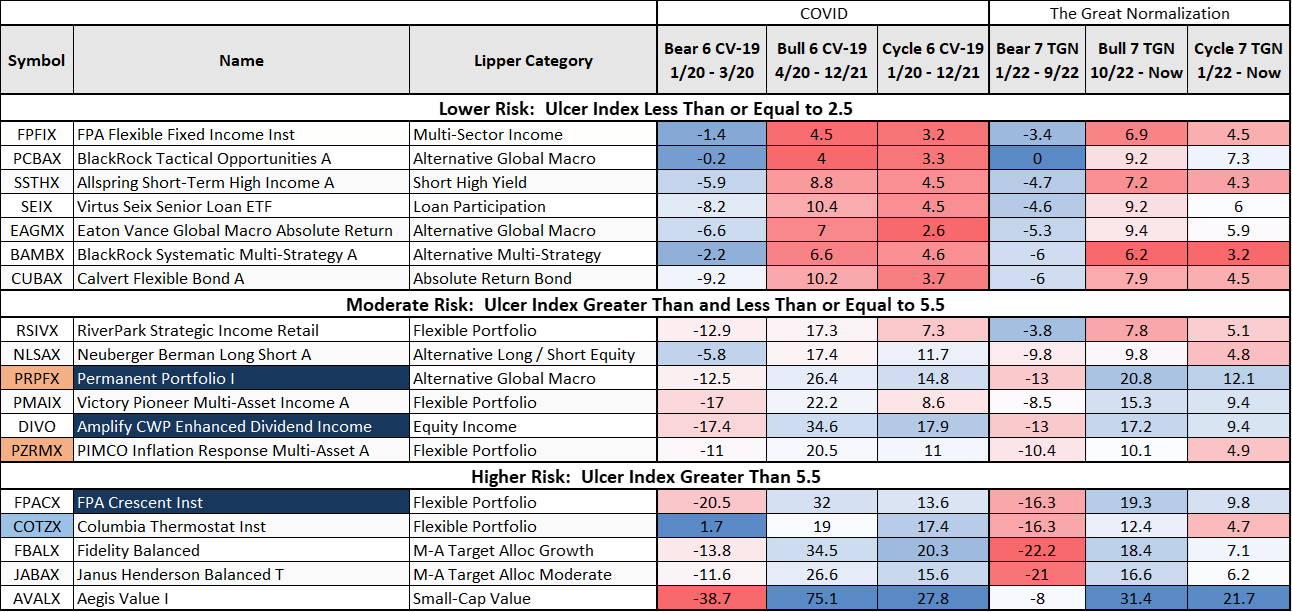

Optimization is determined by having funds with low correlations to one another. Discover that some funds had their most drawdowns throughout the COVID (2020) bear market, and a few had them throughout the Nice Normalization (2022) bear market.

Desk #5 reveals how the funds carried out in every of the bear markets and the bull markets. The lower-risk funds present some security throughout downturns, whereas the riskier funds present progress potential. Blue shaded cells point out one of the best performers, and purple are the worst performers.

Desk #5: Fund Efficiency Throughout COVID and Nice Normalization Cycles

Supply: Creator Utilizing MFO Premium fund screener and Lipper international dataset.

Fund Highlight – COTZX, PRPFX, PZRMX

Columbia Thermostat (COTZX, CTFAX)

Columbia Thermostat bases its inventory to bond allocation on valuations. Through the monetary disaster, the technique was to put money into all shares or bonds, and it didn’t carry out effectively. It has improved its technique to have a spread of allocations relying on value ranges and carried out effectively throughout the COVID bear market. The Reality Sheet signifies that the fund is presently 70% invested in fastened earnings and 30% invested in fairness. It comprises the allocation to shares by the S&P 500 stage.

BlackRock Tactical Alternatives (PBAIX, PCBAX)

BlackRock Tactical Alternatives (PBAIX, PCBAX) is an Different International Macro fund that has carried out effectively because the 2008 monetary disaster, however throughout the monetary disaster fell practically 27% in 2008 and returned 26% in 2009. I personal shares in PCBAX, however restrict allocations to alternate options as a result of they use derivatives, which will be much less predictable throughout a disaster. Eaton Vance International Macro Absolute Return (EAGMX) is one other good Different International Macro fund that had a most drawdown of seven% throughout the monetary disaster. I included it within the authentic goal portfolio from final month.

Comparability of Everlasting Portfolio versus PIMCO Inflation Response Multi-Asset

The Everlasting Portfolio (PRPFX) is predicated on the ideas developed by Harry Browne within the Nineteen Eighties to supply regular, long-term progress with low volatility with out making an attempt to time the market. The fund managers describe Everlasting Portfolio (PRPFX) as, “Designed as a core portfolio holding, Everlasting Portfolio seeks to protect and improve the buying energy worth of every shareholder’s account over the long-term, no matter present or future market circumstances, via strategic investments in a broad array of various asset courses.” It invests fastened percentages of its internet property in greenback property (35%), gold (20%), aggressive progress shares (15%), actual property and pure useful resource shares (15%), Swiss Franc property (10%), and silver (5%).

The PIMCO Inflation Response Multi-Asset (PZRMX) is described by the fund managers as “By investing in a mix of inflation-related asset courses, the fund seeks to assist protect and develop buying energy, improve portfolio diversification, and guard in opposition to market shocks throughout various inflation environments.” It presently has a composition of Inflation Linked Bonds 68%), Commodities (22%), Currencies (15%), REITS (10%), and Treasured Metals (10%). I personal shares in PZRMX.

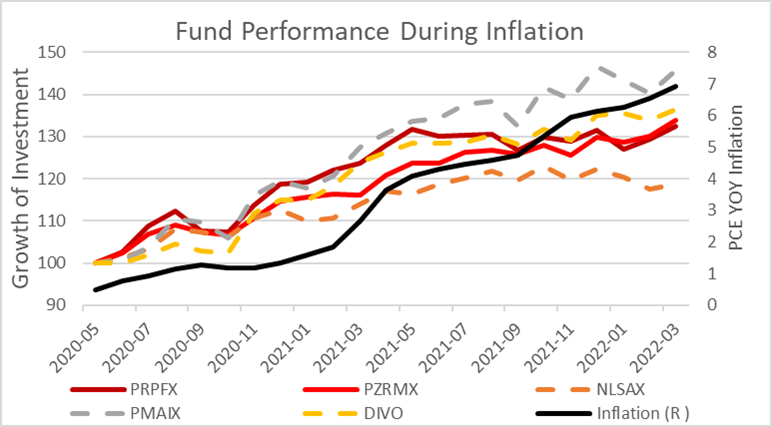

Determine #4 comprises a number of the funds that did effectively throughout 2020 to 2022 with excessive inflation. These are principally within the Versatile Portfolio Lipper Class plus DIVO in fairness earnings, Everlasting Portfolio (PRPFX, maroon line) within the Different International Macro class, and the PIMCO Inflation Response Multi-Asset (PZRMX, purple line) within the Versatile Portfolio Class. Through the interval in between the bear markets, the S&P 500 rose 89% whereas core bonds rose a paltry 2.5%.

Determine #4: Fund Efficiency Throughout Inflation (2020 – 2022)

Supply: Creator Utilizing MFO Premium fund screener and Lipper international dataset and St. Louis Federal Reserve FRED database.

From 2012 via 2019, Everlasting Portfolio (PRPFX) and PIMCO Inflation Response Multi-Asset (PZRMX) had very related efficiency. From 2019 via 2021, PRPFX outperformed PZRMX and tremendously outperformed beginning in 2023. I want proudly owning PRPFX and PZRMX to instantly proudly owning gold as a result of it’s way more risky.

Closing

Over the previous yr, I decreased my allocation to inventory from 65% to 50% which is a small lower in threat. Rebalancing throughout excessive market valuations and downturns is a modest manner of “shopping for low and promoting excessive”. I consider that threat risk-adjusted efficiency of bonds to be better than equities for the following few years. Utilizing the bucket method to match threat property with spending wants and utilizing bond ladders does extra to scale back portfolio threat than decreasing the allocation to shares.

As a qualifier, I take advantage of monetary advisors to handle the vast majority of my portfolio utilizing a conventional, globally diversified 60/40 portfolio. I’m creating this “Conservative Portfolio” technique for a subset of the portfolio that I handle along with conventional bond funds and bond ladders to have liquidity out there in any market situation, and with some progress potential.