{kind=link}

However earlier than we dive into these additional, an essential observe. The next choices are supposed to illustrate pattern portfolios and don’t represent monetary recommendation. Should you haven’t already carried out so, overview the rules behind the right way to construct a couch-potato portfolio and our overview of sofa potato investing earlier than committing your hard-earned cash to any of the investments indicated.

Choice 1: Construct a mutual fund portfolio

Most Canadian banks provide a choice of comparatively low-cost index mutual funds with which you’ll be able to construct your individual balanced portfolio. Relying in your relationship with the establishment, they could throw in recommendation at no cost.

Your mutual fund choices

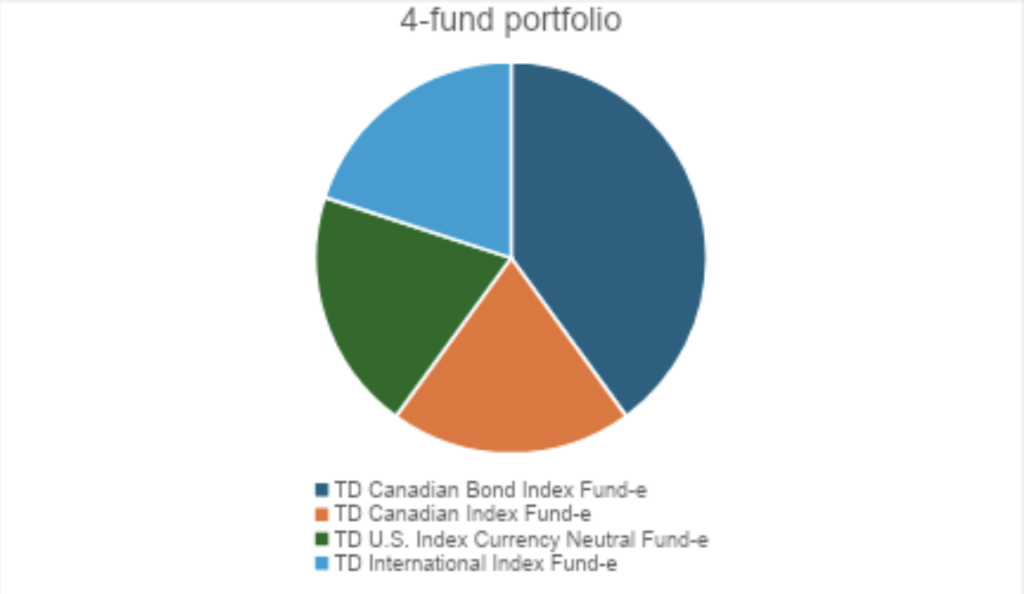

TD is the best-known supplier on this area with its e-Collection funds, however Scotiabank, RBC, and CIBC, amongst others, have comparable merchandise.

The pie chart beneath illustrates how a typical mid-career investor with a reasonable threat tolerance may assemble a portfolio utilizing e-Collection funds. Extra conservative buyers would usually improve the fixed-income allocation as excessive as 80%, whereas extra growth-oriented buyers may scale back the fastened earnings element to twenty% or much less.

Tangerine Financial institution, the web banking subsidiary of Scotiabank, allows you to simplify the method additional with a single, all-in-one product—much like the asset-allocation ETFs described beneath however marketed as a mutual fund. You will discover your selection of Tangerine Core Balanced Portfolio (60% shares, 40% bonds), Core Balanced Revenue Portfolio (70% bonds, 30% shares), Core Balanced Development Portfolio (75% shares, 25% bonds), Core Fairness Development Portfolio (100% world shares), and Core Dividend Portfolio (100% dividend shares), relying in your threat/return profile and investing fashion.

Mutual fund charges

Whereas cheaper than actively managed mutual funds, index mutual funds nonetheless are inclined to cost administration expense ratios (MERs)—annual charges represented as a portion of your complete account, deducted out of your returns—which might be larger than equal exchange-traded funds (ETFs). TD’s e-Collection has MERs of 0.25% to 0.5%. Tangerine’s full portfolios run simply over 1%.

Mutual fund professionals and cons

Examine the most effective TFSA charges in Canada

Choice 2: Construct an ETF portfolio

A core index ETF portfolio can encompass as little as two and as much as 4 ETFs. Core exposures required embrace the U.S., Canadian, and Worldwide equities markets and home fastened earnings.

The pattern portfolios listed below are balanced for reasonable threat and return potential. Extra conservative and growth-oriented buyers can alter their portfolios to skew extra in direction of fastened earnings or equities. See the part on asset-allocation ETFs beneath for examples.

Your ETF choices

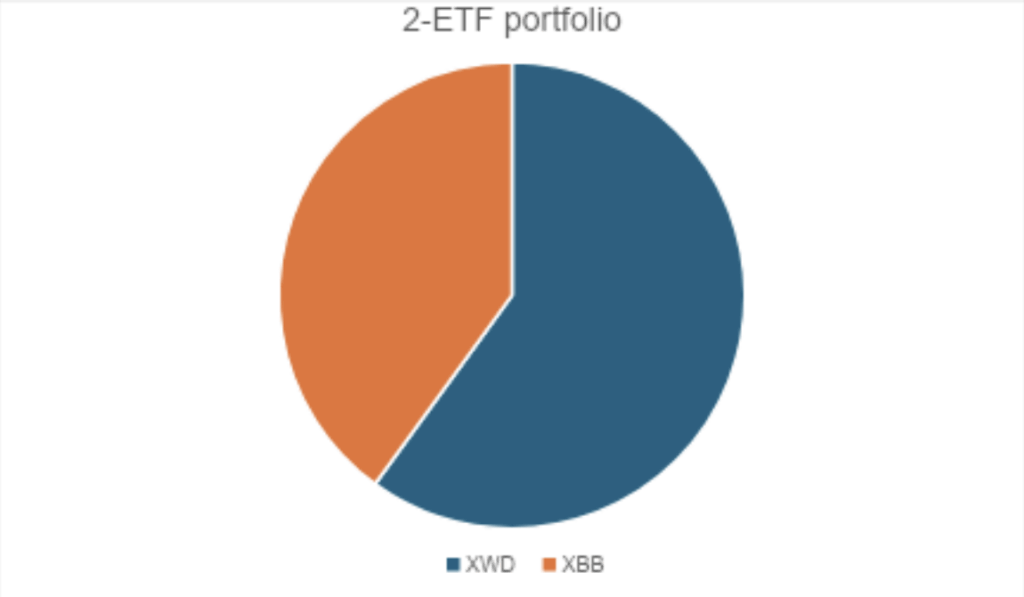

The only method is to purchase a broad bond market fund corresponding to iShares Core Canadian Universe Bond ETF (XBB) or Vanguard Canadian Mixture Bond ETF (VAB) and a worldwide fairness ETF that takes in all geographies corresponding to iShares MSCI World Index ETF (XWD). This may scale back your Canadian fairness publicity to simply 2% and lift your U.S. inventory allocation to virtually 40%— factor in some buyers’ minds, dangerous in others’. One other potential draw back is value: world funds are inclined to have MERs of 0.2%, greater than U.S. and Canadian fairness funds.

We’ve got used iShares funds within the instance beneath, however there are comparable choices from BMO, Vanguard, TD, and World X. For particular fund suggestions, try MoneySense’s yearly up to date information to the most effective ETFs.

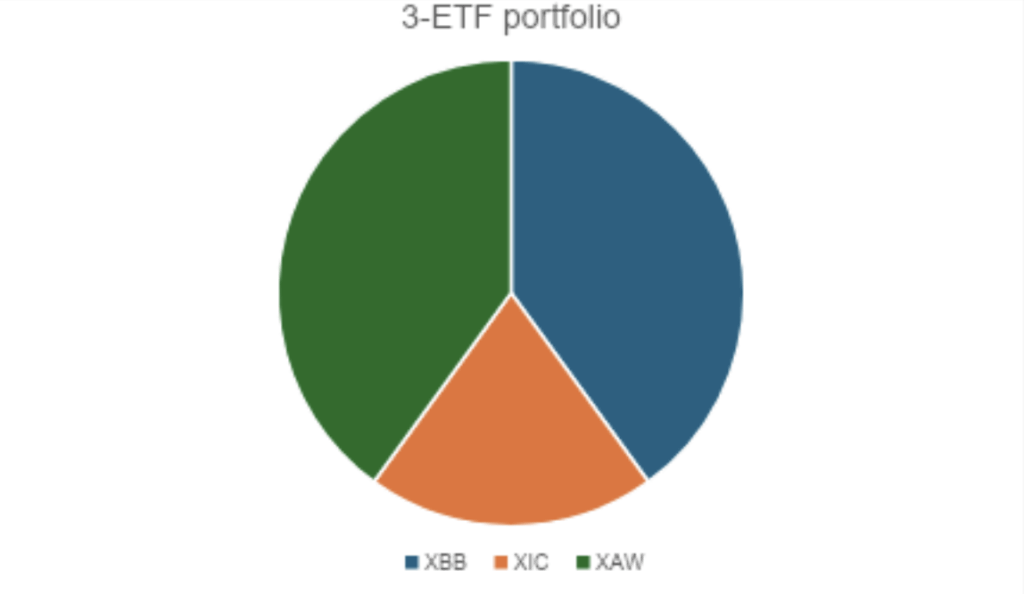

Choice 2b (beneath) options three funds: fastened earnings, world equities excluding Canada, and Canadian fairness. This allows you to set your individual most popular degree of Canadian content material, in addition to take pleasure in low Canadian fairness ETF charges and tax effectivity if the account is taxable.

For the Canadian fairness portion, we’ve got chosen iShares Core S&P/TSX Capped Composite Index ETF (XIC). You will discover extra good Canadian fairness ETF choices in our ETFs information. For World fairness, we used iShares Core MSCI All Cap World ex-Canada Index ETF (XAW). Once more, you could find equivalents from rival fund corporations corresponding to Vanguard and BMO.

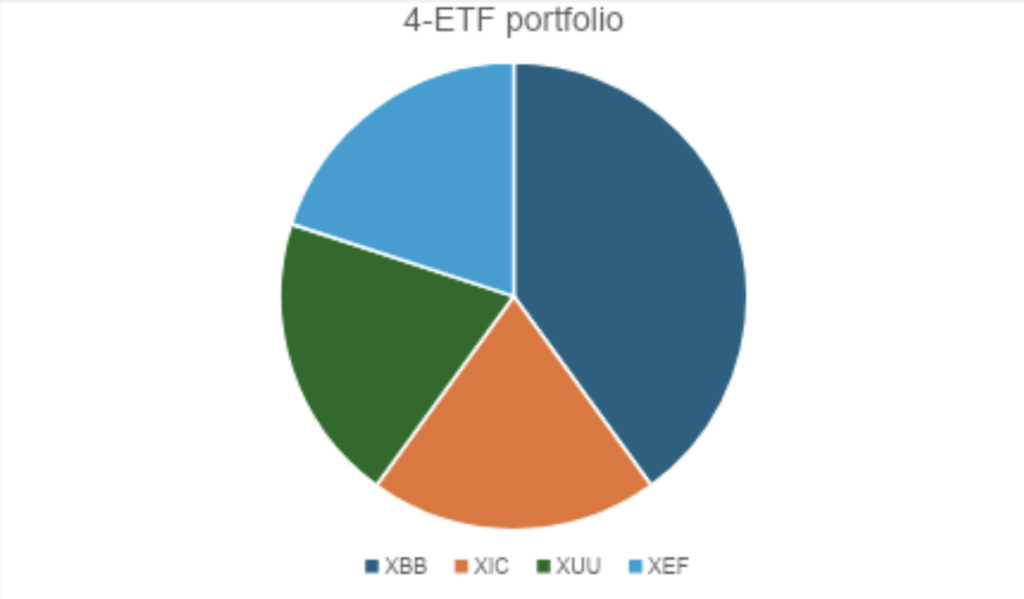

Choice 2c takes in separate funds representing fastened earnings, U.S. equities, Canadian equities, and worldwide equities (developed markets exterior North America). The better complexity brings with it potential value financial savings, but in addition a better want to observe the portfolio and rebalance.

Together with XBB and XIC, we’ve got sampled iShares Core S&P US Complete Market Index ETF (XUU) and iShares Core MSCI EAFE IMI Index ETF (XEF). Discover extra appropriate funds for these core positions in our most up-to-date finest U.S. Fairness ETFs and finest Worldwide Fairness ETFs surveys.

ETF charges

Barring frequent buying and selling that incurs brokerage charges, the index ETF portfolio is the lowest-cost method obtainable to couch-potato buyers. Mixed, your fastened earnings and fairness allocations may have common MERs round 0.1% per yr (barely larger for worldwide fairness). You’ll barely discover it.

ETF professionals and cons

Choice 3: Purchase an asset-allocation ETF

“Asset allocation ETF” is the time period most frequently used within the funding business, however they’re variously often called one-ticket, all-in-one, one-decision and multi-asset ETFs. Primarily, they make investments normally within the fund firm’s personal index ETFs to supply an entire portfolio’s price of publicity in a single funding. Simply purchase one, set your brokerage account desire to DRIP (dividend reinvestment program) in order that quarterly distributions get invested in additional items, and you actually can “set it and neglect it.”

Your asset-allocation ETF choices

There isn’t loads to separate the main ETF suppliers within the asset-allocation area. The larger determination you need to make is the place you need to fall on the danger/return spectrum. Essentially the most conservative possibility, for cash you may want within the subsequent yr or two, is to not use a multi-asset fund in any respect, however as an alternative one invested in excessive curiosity financial savings accounts (HISAs) or the cash market. (See MoneySense’s finest money different ETFs for solutions.)