{kind=link}

If you happen to’re excited about investing in enterprise capital or any non-public fund, you must perceive these 5 key phrases: MOIC, TVPI, DPI, Loss Ratio, and IRR. With out them, it’s like strolling right into a poker recreation with out figuring out the principles. And on this recreation, the stakes—and potential payouts—are large.

I’ve been investing in enterprise capital since 2003, sometimes allocating about 10% of my investable capital to the house searching for multi-bagger winners. Since I don’t have a lot of an edge or the time as an angel investor, I’m glad to outsource the work to common companions (GPs) who supposedly do have the sting, for a charge.

My hope is that I’ll choose the appropriate GPs who will spend their careers looking for winners on behalf of me and different restricted companions. In the event that they succeed, everyone wins.

To date, I’ve had respectable success. A number of funds have returned over 20% yearly for 10 years, whereas others have solely produced excessive single-digit returns. Fortunately, I haven’t invested in a single fund that’s misplaced me cash. The identical couldn’t be mentioned if I had been investing straight in particular person offers, so watch out.

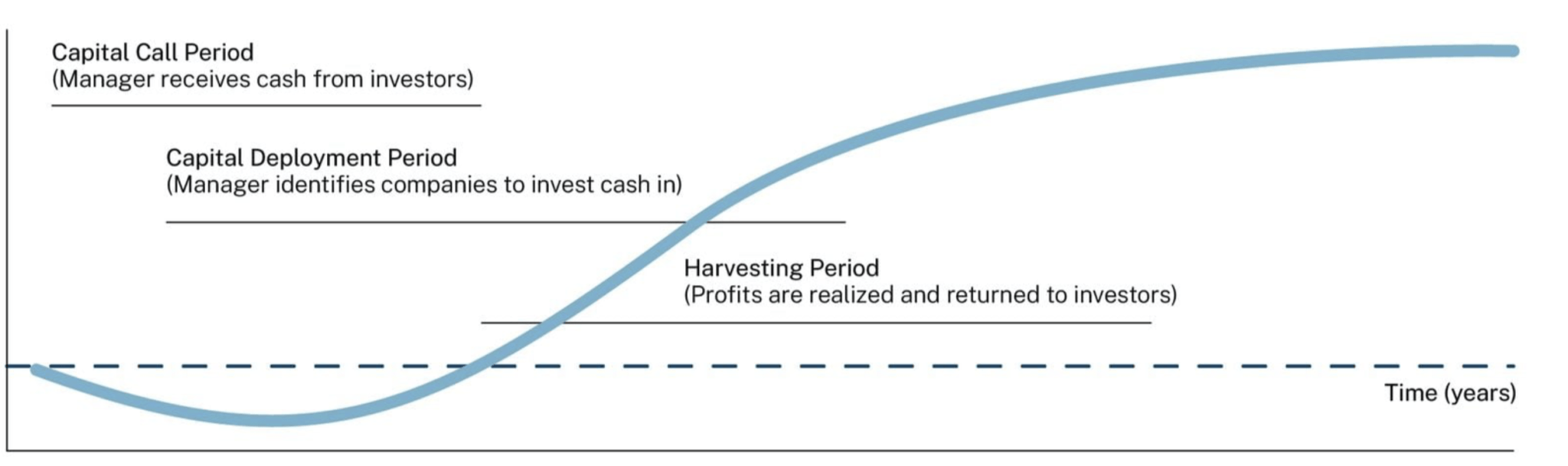

Deciding Whether or not To Make investments In A New Enterprise Capital Classic

Proper now, I’m debating whether or not to commit $200,000 to a brand new closed-end VC fund that focuses on seed and Sequence A corporations. I already dedicated $200,000 to its prior classic a number of years in the past, however to this point the outcomes have been restricted. There’s virtually all the time a loss for the primary few years till the potential income come. That is known as the “J-curve.“

At this early stage, investing is lots like betting on a promising highschool participant ultimately making it to the NBA. Roughly 80% of those corporations will go bust. About 10% will turn into “zombie corporations” or solely mildly worthwhile—like gamers who find yourself enjoying abroad. That leaves the ultimate 10% to ship outsized returns—ideally 30×—to drive the classic towards a 25% IRR over 5 years.

Let’s break down the 5 key metrics utilizing my hypothetical $200,000 funding so you possibly can see precisely how they work.

MOIC — A number of on Invested Capital

MOIC is easy: it’s every thing your funding is value (each the money you’ve gotten again and the businesses you’re nonetheless holding) divided by what you place in.

Instance: I make investments $200,000. Over time, I get $50,000 in money distributions and my remaining holdings are valued at $250,000. That’s $300,000 whole ÷ $200,000 invested = 1.5× MOIC. Not unhealthy, however not life-changing cash.

MOIC says nothing about how lengthy it took to realize it. That is why LPs additionally take a look at IRR (inner fee of return). A 3X in 10 years is a 11.6% IRR, however a 3X in 5 years is a 25% IRR. An enormous distinction.

IRR — Inner Fee of Return

IRR is the annualized return you’ve earned in your funding, making an allowance for each the timing and the scale of money flows out and in. It’s not nearly how a lot you made, however when you made it.

- A 2× MOIC achieved in three years might imply a 26% IRR.

- That very same 2× MOIC over ten years is simply a few 7% IRR.

For funds, IRR is commonly the quantity they brag about as a result of it captures each magnitude and pace of returns — however watch out. IRR might be gamed early on by fast partial returns that make the quantity look flashy, even when the fund’s later exits are mediocre.

TVPI — Complete Worth to Paid-In

For many functions, that is principally the similar as MOIC. It’s simply the VC means of sounding fancier. Formulation: (Residual Worth + Distributions) ÷ Paid-In Capital. So similar math, similar outcome — 1.5× in our instance.

DPI — Distributions to Paid-In

DPI is the “cash-on-cash” quantity. How a lot have you ever truly gotten again in actual, spendable cash? In our case: $50,000 ÷ $200,000 = 0.25× DPI. Paper beneficial properties don’t pay the payments, and DPI is your actuality test.

Loss Ratio

This one’s a intestine punch: the proportion of your invested capital that’s gone to zero. If $40,000 of my $200,000 is in failed startups, that’s a 20% loss ratio.

Pulling All The Enterprise Capital Funding Definitions Collectively

Seven years in, our $200,000 would possibly seem like this:

- Distributions: $50,000

- Unrealized worth: $250,000

- Losses: $40,000

- MOIC/TVPI = 1.5× ($300,000 / $200,000)

- DPI = 0.25× ($50,000 / $200,000)

- Loss Ratio = 20% ($40,000 / $200,000)

Finest-Case State of affairs (5× MOIC)

Prime tier enterprise capital companies return a 5X MOIC over a 10-year interval. Let’s check out what that might seem like.

- $500,000 in distributions + $500,000 in unrealized worth for a complete of $1,000,000

- DPI = 2.5× ($500,000 / $200,000)

- Loss Ratio = 10% ($10,000 / $200,000)

- IRR = 26.23% over 10 years

A 26.23% inner fee of return (IRR)—the annualized fee at which an funding grows over time—over 10 years is phenomenal, about 16% greater than the S&P 500’s common annual return. Simply pretty much as good is that the enterprise capital restricted associate stayed invested for the total decade, partly as a result of they needed to. With public equities, it’s far simpler to panic promote or lock in income early, which might derail long-term compounding.

Reasonable Worst-Case State of affairs (0.7× MOIC)

Backside tier enterprise capital companies return a 1X MOIC or much less. Here is what a 0.7X MOIC might seem like on a $200,000 funding.

- $50,000 in distributions + $90,000 in unrealized worth ($140,000 / $200,000)

- DPI = 0.25× ($50,000 / $200,000)

- Loss Ratio = 40% ($80,000 / $200,000)

- IRR = –4.24% over 10 years

So despite the fact that the unhealthy fund “solely” loses ~30% of its worth on paper, the time issue drags the annualized return deep into damaging territory. If the S&P 500 returned 10% a yr over the identical 10-year interval, you’d have $519,000 versus simply $140,000. That’s an enormous hole, which is why selecting the best enterprise capital funds is crucial.

Betting on a brand-new VC is dangerous as a result of lack of a observe document. To offset this, the overall associate must both decrease their charges and carry, or seed the portfolio with some early winners to scale back the J-curve interval of losses and enhance the chances of reaching a robust MOIC and IRR.

Enterprise Capital Is A Hit-Pushed Enterprise

The fact is most investments fail, a couple of go sideways, and one or two residence runs make the fund. A excessive MOIC with a low DPI means you’re “paper riches.” A excessive loss ratio tells you the supervisor is swinging for the fences, however lacking usually. Ensure the ratios align with what you need.

Earlier than writing a test, all the time:

- Verify the observe document — throughout a number of funds and vintages (years), not simply the shiny final one.

- Ask in regards to the loss ratio — you’ll shortly see in the event that they’re disciplined or gamblers.

- Discover out the time to liquidity — as a result of a 5× MOIC in yr 15 is lots much less thrilling than it sounds.

- Be trustworthy about your personal threat tolerance — might you watch 90% of your portfolio corporations fail with out shedding sleep?

Figuring out MOIC, TVPI, DPI, Loss Ratio, and IRR gained’t magically make you choose the subsequent Sequoia Capital. However it would cease you from investing blind. And in enterprise capital, avoiding massive errors is necessary. You do not need to lock up your capital for 10-plus years solely to considerably underperform. The chance price could also be too nice to bear.

Various Selection: Open-Ended Enterprise Capital Funds

If you need publicity to enterprise capital with out the painful drawbacks, open-ended VC funds are value a tough look. These autos don’t simply provide liquidity, additionally they allow you to see the portfolio earlier than you make investments. That’s type of like sitting down at a Texas Maintain’em desk already figuring out your opponents’ playing cards and seeing the flop earlier than it’s revealed.

With that type of visibility, you possibly can determine whether or not the businesses are thriving or floundering and place your bets with a real edge. Positive, the flip and river can nonetheless deliver surprises, however not less than investing is not a complete leap of religion like the best way you might be with conventional closed-end funds. Over time, that information benefit could add up.

Your Age Issues When You Make investments In Enterprise

The older I get, there threat there’s in locking up cash for a decade with much less visibility and liquidity. With closed-end VC funds, you often don’t understand how issues are going till yr three, on the earliest.

10 years is a very long time to attend for returns and capital again. At 48, I can’t assure I’ll even be alive at 58 to benefit from the beneficial properties. If an emergency arises, I additionally need the choice of tapping some liquidity, which conventional funds merely don’t enable. That’s why you need to solely spend money on them with cash you’re 100% positive you gained’t want for a decade.

Then there’s the 20%–35% carry charge. I get it. Common companions earn their maintain by discovering high-return corporations. As an economist, I ought to settle for paying if I’m nonetheless earning profits. But when there’s an alternate approach to spend money on non-public corporations with out coughing up that hefty slice of income, why wouldn’t I take it? That is the place platforms like Fundrise Enterprise shine.

Personally, I’m diversified throughout early-, mid-, and late-stage VC, however my candy spot is Sequence A, B, and C. These corporations often have actual traction, recurring income, and product-market match. As an alternative of praying for a 100X moonshot from a seed-stage gamble, I’ll fortunately take “constant” 10–20X winners. At this stage in my life, likelihood and visibility matter way over chasing lottery tickets.

Flexibility And Visibility Are Engaging Attributes To Investing

Open-ended VC funds provide you with one thing uncommon in non-public investing: flexibility and readability. They scale back lock-up threat, eradicate hefty carry charges in some circumstances, and provide you with visibility into what you’re truly shopping for. You may skip the J-curve with an open-ended VC fund.

For youthful buyers with a long time to attend, conventional closed-end funds makes extra sense. The capital calls over a three-to-five-year interval are nice for constant investing. However for these of us who or older and worth optionality, open-ended funds really feel just like the extra pragmatic alternative.

So there you have got it. Now you recognize the principle enterprise capital funding phrases and choices that can assist you higher allocate your capital. Keep in mind to remain disciplined as you construct extra wealth for monetary freedom.

Readers, are you a enterprise capital investor? In that case, what proportion of your investable capital do you allocate to the asset class? With development corporations staying non-public for longer, why don’t extra buyers put extra capital into non-public markets to seize that upside?

Subscribe To Monetary Samurai

Hear and subscribe to The Monetary Samurai podcast on Apple or Spotify. I interview consultants of their respective fields and focus on a few of the most fascinating matters on this website. Your shares, rankings, and evaluations are appreciated.

To expedite your journey to monetary freedom, be part of over 60,000 others and subscribe to the free Monetary Samurai e-newsletter. It’s also possible to get my posts in your e-mail inbox as quickly as they arrive out by signing up right here. Monetary Samurai is among the many largest independently-owned private finance web sites, established in 2009. All the things is written primarily based on firsthand expertise and experience.