{kind=link}

Commonplace metrics level to an enchancment in Treasury market liquidity in 2024 to ranges final seen earlier than the beginning of the present financial coverage tightening cycle. Volatility has additionally trended down, per the improved liquidity. Whereas at the very least one market functioning metric has worsened in latest months, that measure is an oblique gauge of market liquidity and suggests a stage of present functioning that is much better than on the peak seen throughout the international monetary disaster (GFC).

Why Treasury Market Liquidity Issues

The U.S. Treasury securities market is the most important and most liquid authorities securities market on this planet, with greater than $27 trillion in marketable debt excellent (as of August 31, 2024). The securities are utilized by the Treasury Division to finance the U.S. authorities, by monetary establishments to handle rate of interest threat and value different monetary devices, and by the Federal Reserve to implement financial coverage. Having a liquid market is necessary for all of those functions and is thus of eager curiosity to market members and policymakers alike.

How Treasury Market Liquidity Is Measured

Market liquidity will be outlined as the price of rapidly changing an asset into money (or vice versa) and is measured in varied methods. As in previous work, I take a look at three frequent measures, estimated utilizing high-frequency knowledge from the interdealer market: the bid-ask unfold, order guide depth, and value influence. The measures are calculated for probably the most just lately auctioned (on-the-run) two-, five-, and ten-year notes (the three most actively traded Treasury securities, as proven in this put up) over New York buying and selling hours (outlined as 7 a.m. to five p.m., japanese time).

Treasury Market Liquidity Continues to Enhance

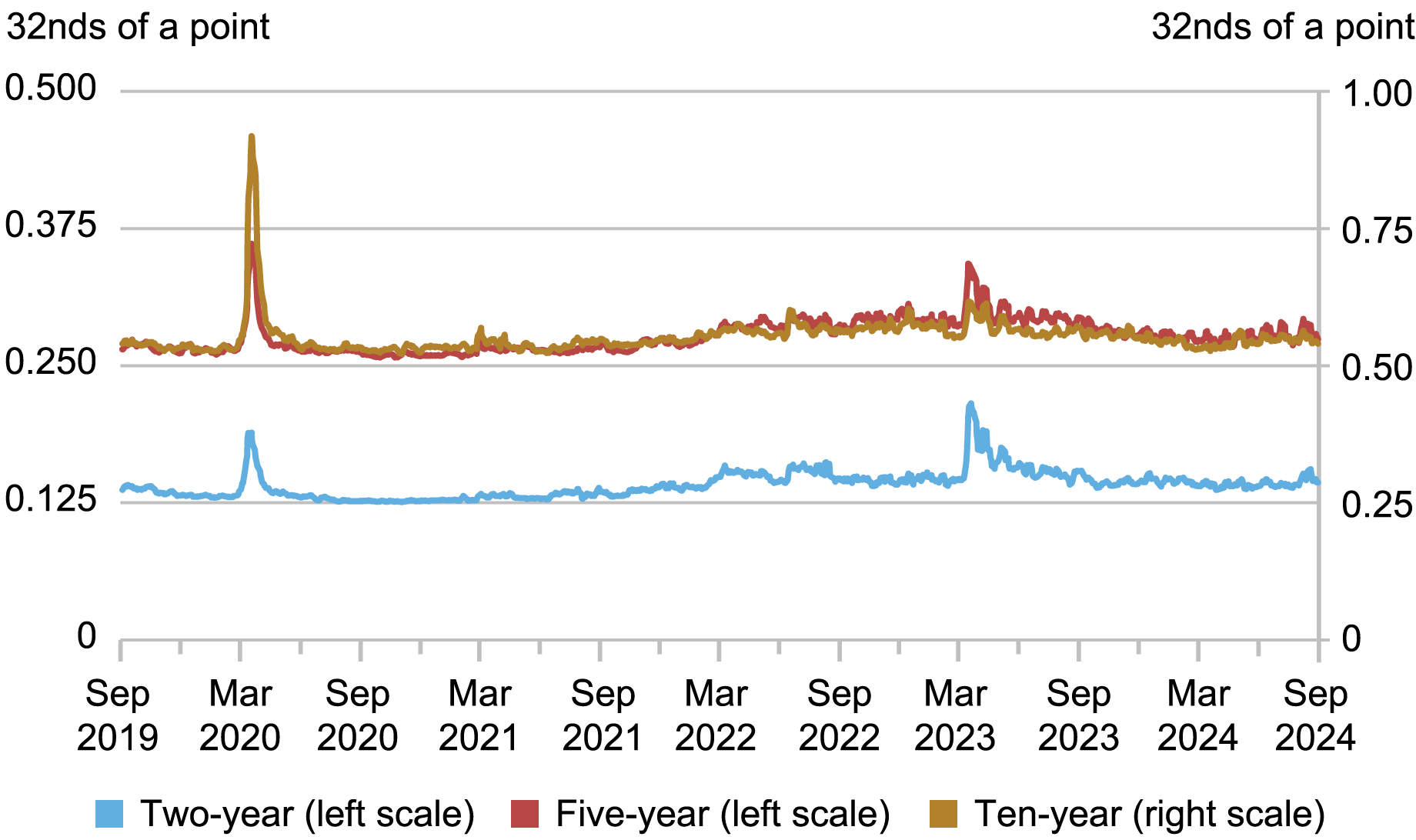

The bid-ask unfold—the distinction between the best bid value and the bottom ask value for a safety—is among the hottest liquidity measures, with wider spreads implying worse liquidity. As proven within the chart beneath, bid-ask spreads widened throughout the COVID-related disruptions of March 2020 (examined in this put up) and once more across the banking failures of March 2023, however narrowed rapidly after each episodes. Since mid-2023, spreads have been slim and steady.

Bid-Ask Spreads Stay Slender

Supply: Creator’s calculations, based mostly on knowledge from BrokerTec.

Notes: The chart plots five-day shifting averages of common each day bid-ask spreads for the on-the-run two-, five-, and ten-year notes within the interdealer market from September 1, 2019 to August 31, 2024. Spreads are measured in 32nds of a degree, the place a degree equals one p.c of par.

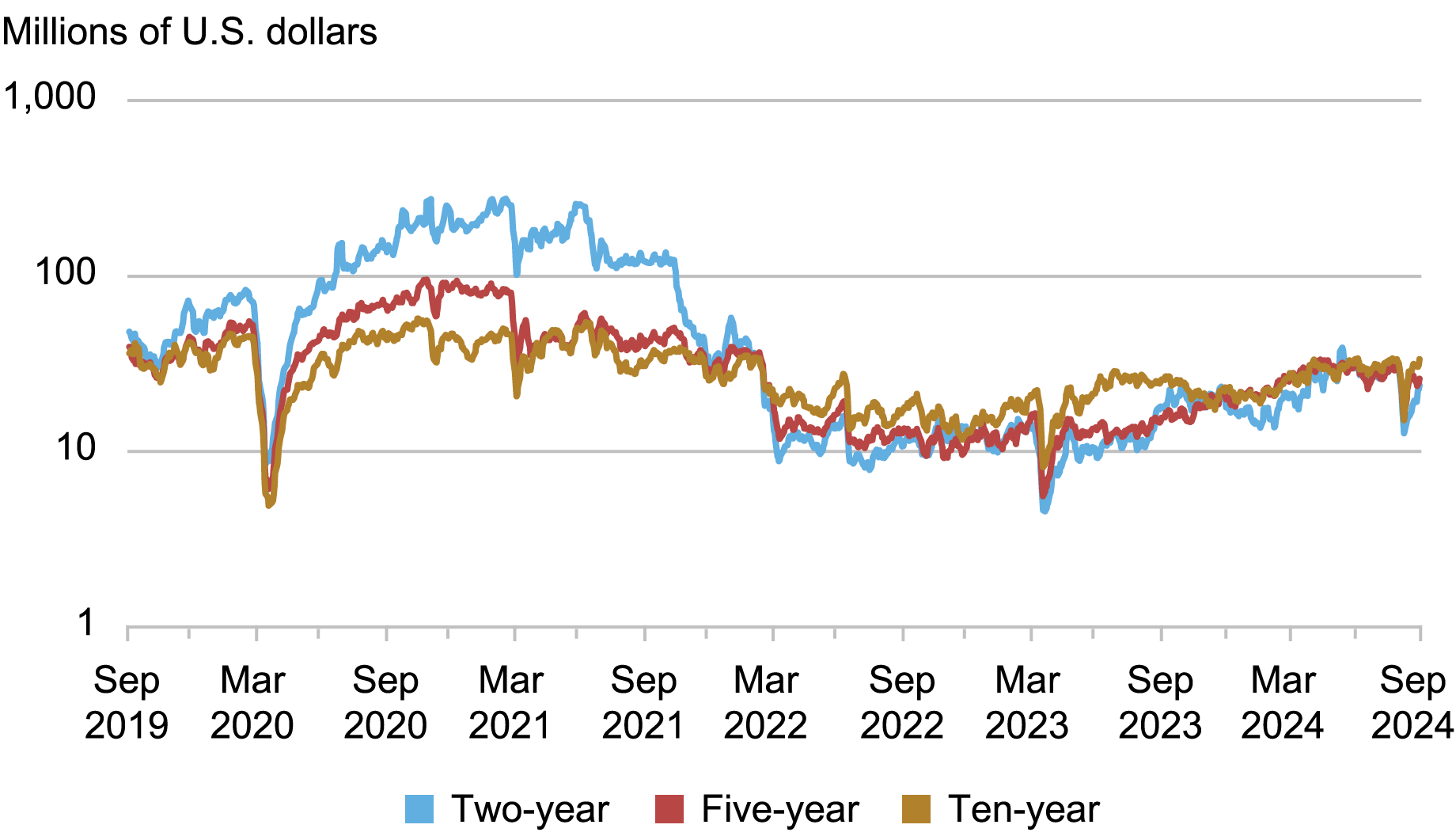

The subsequent chart plots order guide depth, measured as the common amount of securities out there on the market or buy at the perfect bid and provide costs. Decrease depth implies worse liquidity. Depth plunged in March 2020, recovered thereafter, after which declined once more within the months across the begin of the present coverage charge tightening cycle in March 2022 and across the banking failures in March 2023. Depth has typically been rising since March 2023, hitting ranges corresponding to these of early 2022, however declined briefly in early August 2024 round a weaker-than-expected employment report and international fairness market declines.

Order Ebook Depth Is Rising

Supply: Creator’s calculations, based mostly on knowledge from BrokerTec.

Notes: The chart plots five-day shifting averages of common each day depth for the on-the-run two-, five-, and ten-year notes within the interdealer market from September 1, 2019 to August 31, 2024. Knowledge are for order guide depth on the inside tier, averaged throughout the bid and provide sides. Depth is measured in tens of millions of U.S. {dollars} par and plotted on a logarithmic scale.

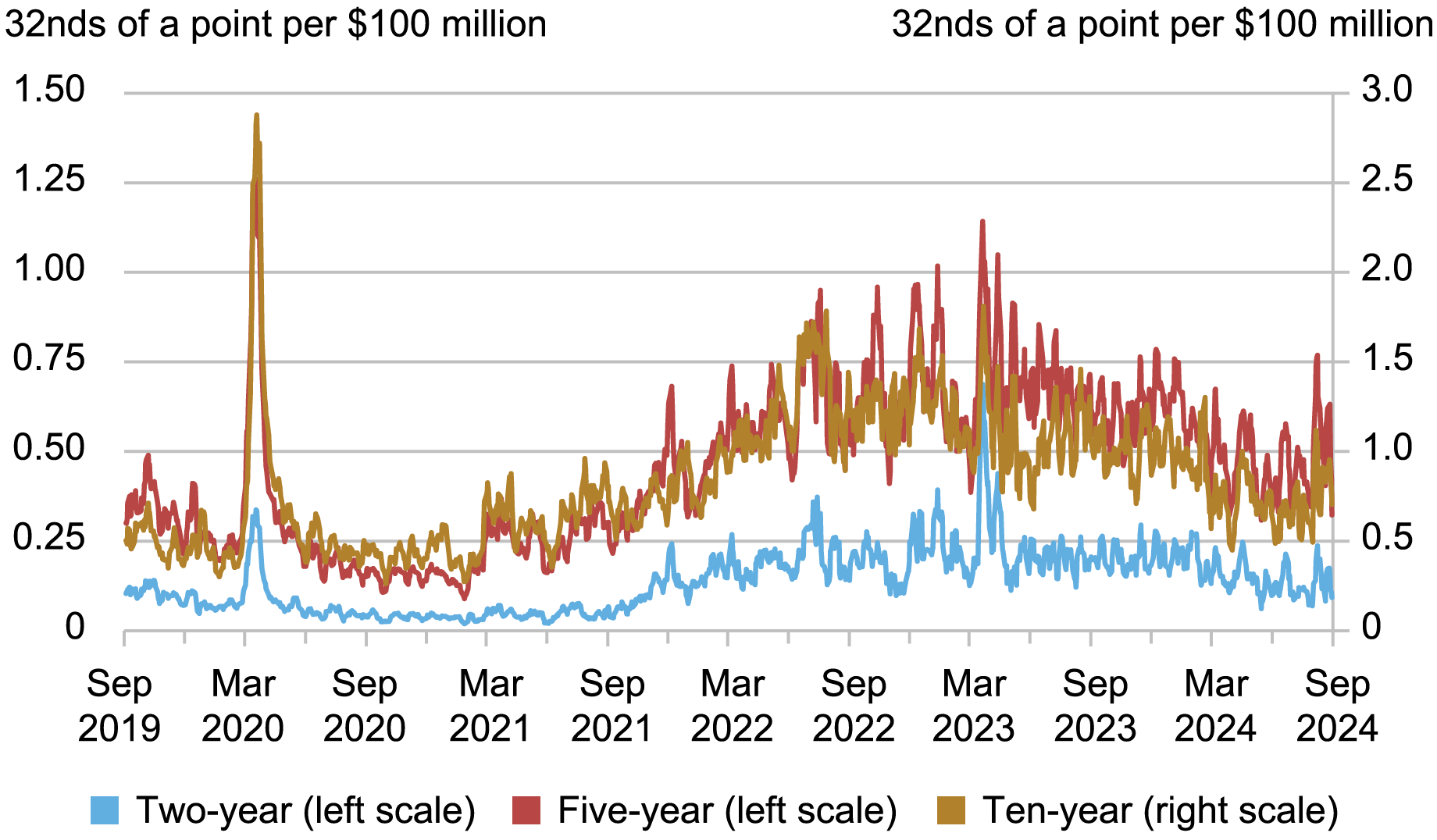

Measures of the value influence of trades additionally recommend an enchancment in liquidity. The subsequent chart plots the estimated value influence per $100 million in internet order movement (that’s, buyer-initiated buying and selling quantity much less seller-initiated buying and selling quantity). A better value influence signifies worse liquidity. Worth influence rose sharply in March 2020, declined thereafter, after which elevated once more within the months previous and following the beginning of the present tightening cycle. Worth influence rose sharply once more in March 2023, after which trended all the way down to ranges final seen in late 2021 or early 2022, earlier than rising briefly in early August 2024.

Worth Influence Is Declining

Supply: Creator’s calculations, based mostly on knowledge from BrokerTec.

Notes: The chart plots five-day shifting averages of slope coefficients from each day regressions of one-minute value modifications on one-minute internet order movement (buyer-initiated buying and selling quantity much less seller-initiated buying and selling quantity) for the on-the-run two-, five-, and ten-year notes within the interdealer market from September 1, 2019 to August 31, 2024. Worth influence is measured in 32nds of a degree per $100 million, the place a degree equals one p.c of par.

Treasury Volatility Continues to Reasonable

Posts in 2022 and 2023 emphasised the destructive relationship between liquidity and volatility. Volatility causes market makers to widen their bid-ask spreads and put up much less depth at any given value and for the value influence of trades to extend. It’s then not stunning to seek out that the development in liquidity over the previous eighteen months has been accompanied by a lower in value volatility. Furthermore, the present stage of liquidity is per the present stage of volatility, as implied by the historic relationship between the variables.

A Conflicting Measure?

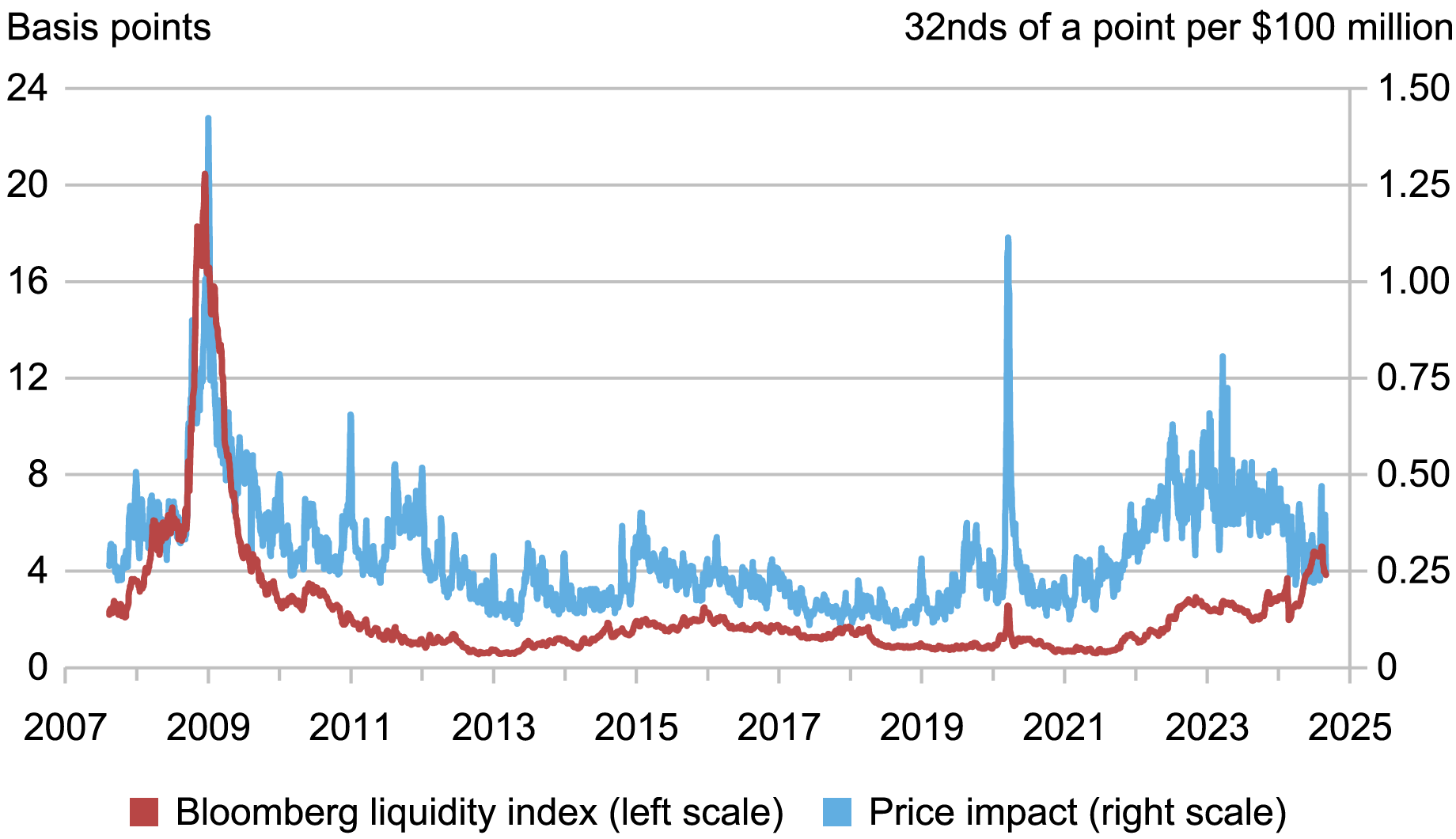

Whereas the measures mentioned to date level to liquidity that’s enhancing and much better than it was in March 2020, this isn’t true for all measures. So-called yield curve “noise” measures, which gauge the dispersion of particular person Treasury safety yields round a smoothed yield curve, have just lately risen, suggesting decreased liquidity. Whereas dispersion doesn’t measure liquidity instantly, it’s thought to replicate the quantity of arbitrage capital out there and therefore function a proxy for liquidity (as defined in this paper). The chart beneath plots one such model of the measure, the Bloomberg U.S. Authorities Securities Liquidity Index, in opposition to our value influence measure since 2007.

Completely different Measures Evolve Otherwise

Sources: Creator’s calculations, based mostly on knowledge from Bloomberg and BrokerTec.

Notes: The chart plots five-day shifting averages of the Bloomberg U.S. Authorities Securities Liquidity Index and common value influence for the on-the-run two-, five-, ten-, and thirty-year securities. Worth influence is calculated for every safety as described within the previous chart’s word, with every safety’s value influence then weighted by the inverse of its normal deviation in calculating the cross-security common. The pattern interval is August 7, 2007 to August 31, 2024.

Whereas the Bloomberg measure has just lately risen, it stays far beneath its peak throughout the GFC. Furthermore, it remained far beneath its GFC peak in March 2020 even when direct liquidity measures approached GFC ranges and the Fed unleashed large asset purchases to deal with the dysfunction then roiling the market (described in this paper). It follows that the latest habits of the Bloomberg index appears much less notable when examined in an extended historic context. The explanations behind the disparate performances of the completely different measures are an fascinating space for future analysis.

Continued Watchfulness

Whereas Treasury market liquidity continues to enhance, continued watchfulness stays prudent. The market’s capability to easily deal with giant buying and selling flows has been of ongoing concern since March 2020 (as mentioned in this paper), debt excellent continues to develop, and latest empirical work exhibits how constraints on intermediation capability can worsen illiquidity. Shut monitoring of Treasury market liquidity, and continued efforts to enhance the market’s resilience, stay acceptable.

Michael J. Fleming is the top of Capital Markets Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Find out how to cite this put up:

Michael Fleming, “Has Treasury Market Liquidity Improved in 2024?,” Federal Reserve Financial institution of New York Liberty Road Economics, September 23, 2024, https://libertystreeteconomics.newyorkfed.org/2024/09/has-treasury-market-liquidity-improved-in-2024/.

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).