{kind=link}

Krishna Institute of Medical Sciences Ltd – Actual Wealth is Good Well being

Established in 1973 and headquartered in Secunderabad, Krishna Institute of Medical Sciences Ltd (KIMS) is without doubt one of the nation’s main hospital networks that gives built-in, multi-disciplinary healthcare providers, specializing in tertiary and quaternary care. It has robust presence in Telangana, Andhra Pradesh, Maharashtra, Kerala and Karnataka. The corporate’s flagship hospital in Secunderabad, with a 1,000-bed capability, is without doubt one of the largest personal hospitals in India. The corporate has a widespread community of 12 hospitals, 5,500+ beds and a pair of,300+ medical doctors.

Merchandise and Companies

KIMS supplies multi-speciality care providers throughout varied divisions equivalent to neurology, cardiology, pulmonology, ENT, ophthalmology, oncology, orthopaedics, paediatrics, diagnostics and so forth.

Subsidiaries: As of FY24, the corporate has 12 subsidiaries and 1 affiliate firm.

Funding Rationale

- Enlargement plans – The corporate is planning to launch three new initiatives in Thane and two in Bengaluru in Q2FY26. In Q3FY25, it commissioned a 200-bed multispecialty hospital in Guntur underneath an Operations & Administration (O&M) mannequin. As a part of its geographic enlargement, it’s establishing three new services in Kerala. The primary facility in Kannur has already been launched and achieved breakeven inside three months. The second is being arrange by means of an settlement with Valiyath Institute of Medical Sciences Hospital in Kannur, whereas the third facility in Thrissur is predicted to grow to be operational inside 12–15 months. Moreover, the corporate plans so as to add 500 beds to its Kondapur facility, rising the whole capability to 800 beds. It has additionally entered into O&M agreements with a number of hospitals throughout Guntur, Visakhapatnam, Hyderabad, and Maharashtra. Moreover, the corporate has signed a Rs.700 crore settlement with Wipro GE Healthcare for the procurement of medical applied sciences and providers.

- Pioneering modern launches within the nation – The corporate prioritizes the mixing of cutting-edge applied sciences into its operations. Setting a brand new normal in neuro care, it has launched South Asia’s first MRI-guided centered ultrasound utilizing the Hero 3T MRI—an innovation confirmed to alleviate tremor-dominant Parkinson’s illness and important tremors. Moreover, the corporate has developed AI-powered sensible glasses to help the visually impaired. It additionally holds the excellence of being the primary personal hospital within the nation to finish 100 robotic-assisted Whipple procedures, marking a serious milestone within the therapy of pancreatic most cancers.

- Q3FY25 – Throughout the quarter, the corporate generated income of Rs.772 crore, attaining a rise of 27% as in comparison with the Rs.606 crore of Q3FY24. EBITDA improved by 37% YoY, from Rs.150 crore to Rs.205 crore. Internet revenue stood at Rs.93 crore, a rise of 21% from Rs.77 crore of Q3FY24. In comparison with the earlier yr, common income per working mattress grew by 25%, common income per affected person grew by 12% and IP quantity grew by 14%. Common size of keep has lowered from 4.18 days to three.75 days in the course of the quarter.

- FY24 – The corporate generated income of Rs.2,511 crore, a rise of 13% in comparison with FY23 income. Working revenue is at Rs.654 crore, up by 4% YoY. The corporate posted a web revenue of Rs.336 crore, a de-growth of 9% YoY.

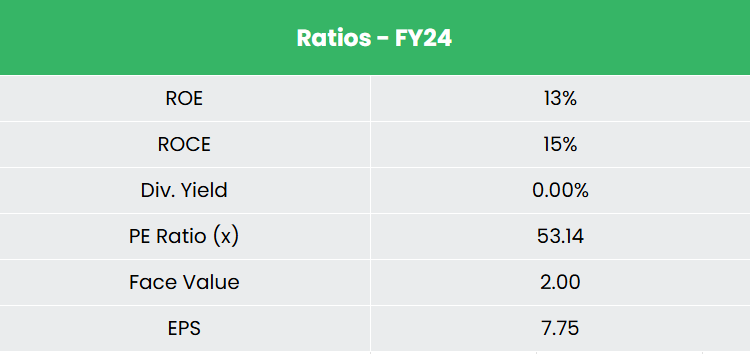

- Monetary Efficiency – The income and web revenue CAGR of the corporate for the previous 3 years is round 23% and 15% between FY21-FY24. The three-year common ROE and ROCE for the corporate is round 22% and 25% for the previous 3 years. The corporate has a wholesome capital construction with a debt-to-equity ratio of 0.89.

Trade

The healthcare sector in India is without doubt one of the largest industries, each when it comes to income and employment. It encompasses hospitals, medical gadgets, medical trials, outsourcing, telemedicine, medical tourism, medical health insurance, and medical tools. In 2023, India’s hospital market was valued at US$ 98.98 billion, with projections indicating a CAGR of 8.0% from 2024 to 2032, reaching an estimated worth of US$ 193.59 billion by 2032. This development is predicted to be fast, pushed by increasing protection, improved providers, and rising investments from each private and non-private sectors. India can also be a cheap choice in comparison with different international locations in Asia and the West, making it a gorgeous vacation spot for worldwide sufferers and contributing to the rise of medical tourism. The Indian medical tourism market was valued at US$ 7.69 billion in 2024, with expectations to develop to US$ 14.31 billion by 2029.

Progress Drivers

- Authorities allocation of Rs.99,858 crore (US$ 11.50 billion) to the healthcare sector within the Union Funds 2025-26, a 9.78% improve in comparison with the earlier yr.

- FDI of Rs.97,208 crore (US$ 11.19 billion) into the hospitals and diagnostics sector between April 2000-September 2024.

- Rising revenue ranges, ageing inhabitants, rising well being consciousness and larger penetration of medical health insurance.

Peer Evaluation

Opponents: International Well being Ltd, Aster DM Healthcare Ltd, and so forth.

We imagine KIMS is pretty valued relative to its friends, supported by its stable fundamentals, sturdy income development, and constant returns on invested capital.

Outlook

KIMS is aiming for a development fee of 18–20% in FY26, pushed by the launch of latest hospitals and operations & administration (O&M) contracts. Over the following two years, the corporate plans so as to add between 2,000 and a pair of,500 beds, with greater than 2,300 beds already underneath development. Its strategic enlargement into Tier-2 and Tier-3 cities, together with the enhancement of providers in its core areas, seems promising—supported by sturdy infrastructure and a succesful crew. Moreover, KIMS’s deal with introducing modern healthcare options is predicted to spice up its buyer base and strengthen its model worth.

Valuation

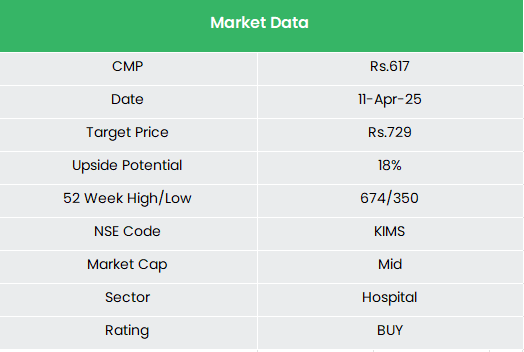

We anticipate the corporate to maintain its development momentum given the a number of capex plans in progress by means of varied greenfield and brownfield initiatives. We suggest a BUY ranking within the inventory with the goal value (TP) of Rs.729, 50x FY26E EPS.

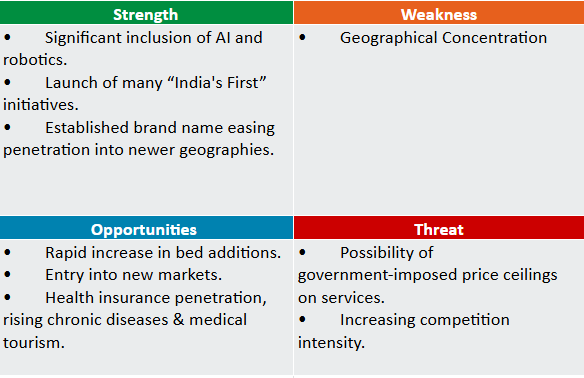

SWOT Evaluation

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please be aware that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles it’s possible you’ll like