{kind=link}

Equities have been on fairly the curler coaster in 2025. Though the tariff scenario has pushed a lot of this volatility, we discover ourselves in the same spot to the place we started the yr. Valuations stay excessive, the market continues to be relying on the expansion of the Magnificent 7 (Magazine 7), and analysts proceed to count on above-average development for the following a number of years, regardless of all of the uncertainty.

To know the equities outlook for the second half of the yr, let’s first contemplate how we received right here.

A Whirlwind of a First Half

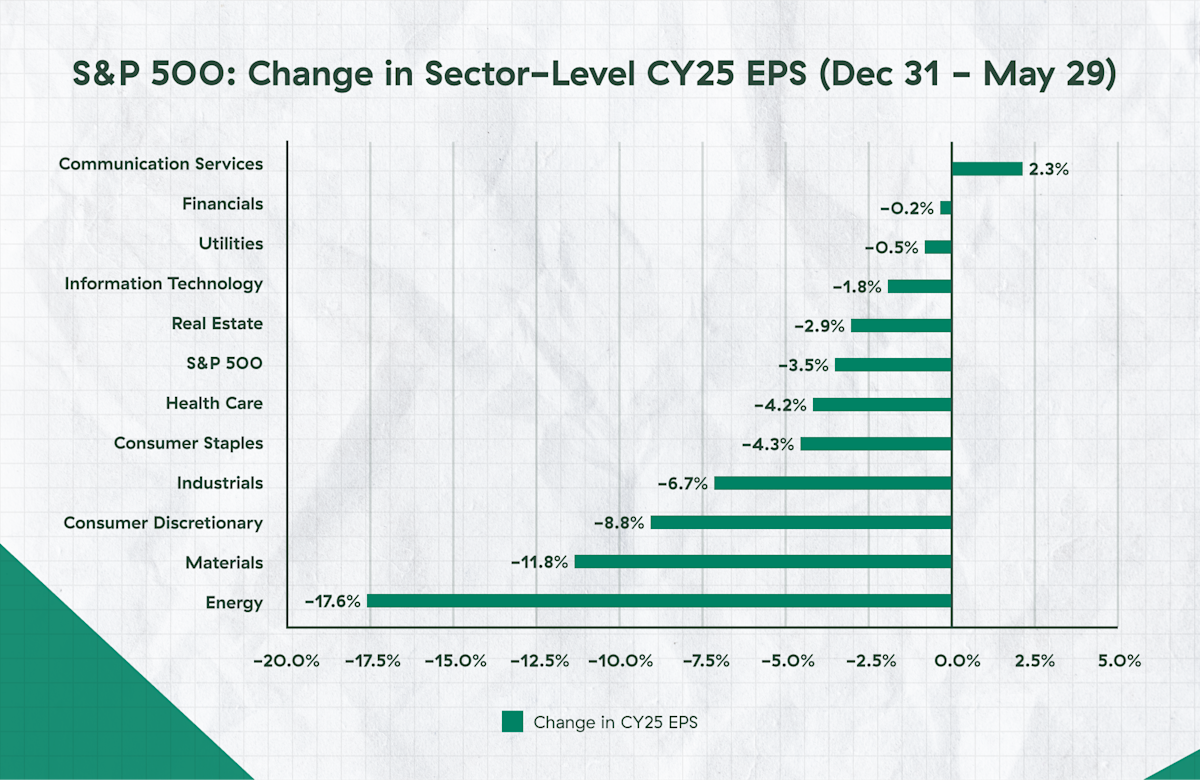

Firstly of 2025, analysts have been anticipating shut to fifteen % earnings development for the S&P 500. Within the two quarters since, we’ve seen the same story from a elementary perspective—however with some key variations as to why. Every quarter noticed earnings beat expectations by strong margins, however analysts then lowered future development expectations, offsetting a few of that optimistic information.

Within the first quarter, lowered development expectations hit the tech sector and the Magazine 7 significantly onerous. Analysts started to see a deceleration in development projections for corporations whose valuations relied on important future development projections. Within the second quarter, most of these corporations beat lowered expectations, with funding spending for AI persevering with at a robust tempo regardless of enterprise issues over tariffs and the broader financial system.

The long run development expectations for tech and communications providers additionally held up effectively, resulting in a rebound for development corporations dominated by these sectors. Regardless of a majority of cyclical sectors beating their first-quarter development estimates, corporations and analysts had issues over tariffs and the financial system, resulting in lowered future estimates.

Within the chart beneath, you may see the total affect of all of the analyst adjustments to estimates because the starting of the yr.

Supply: FactSet as of 5/30/2025

A Story of Two Markets

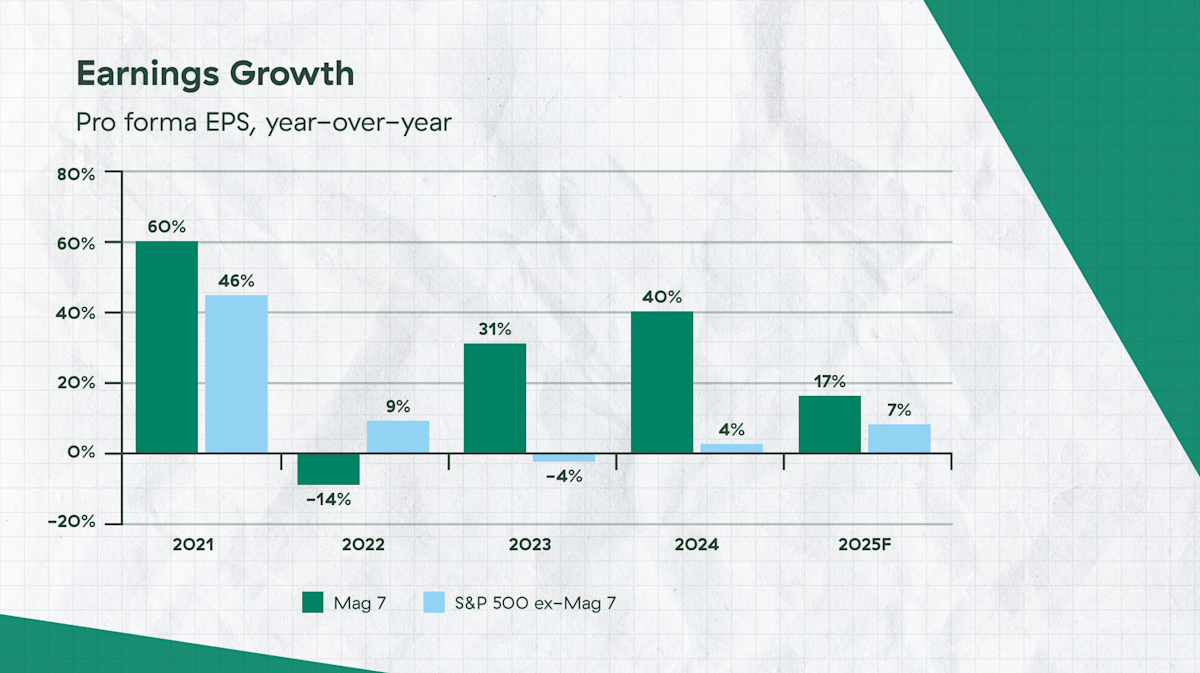

There are numerous methods to categorize the markets: large-caps versus small-caps, U.S. versus worldwide, and worth versus development. However the greatest divide for the previous few years? The Magazine 7 versus everybody else.

The recurring story over the previous yr and a half has been the expansion of the highest corporations declining towards the remainder of the S&P 500 however frequently managing to beat these expectations. Magazine 7 valuations stay effectively above the remainder of the S&P 500, however they’re nonetheless anticipated to see 17 % earnings development for 2025 versus 7 % for the remainder of the index.

Supply: FactSet, Normal & Poor’s, J.P. Morgan Asset Administration. Magnificent 7 contains AAPL, AMZN, GOOG, GOOGL, META, MSFT, NVDA, and TSLA. Earnings estimates for 2025 are forecasts based mostly on consensus analyst expectations. Information to the Markets – U.S. Knowledge as of June 6, 2025.

The largest potential driver for continued S&P 500 development stays the flexibility of corporations closely concerned within the AI revolution to beat development projections. Given the optimistic outlook from the Magazine 7 of their Q1 earnings calls and lots of of these of their provide chain, we see strong development persevering with within the second half of the yr.

Right here, it’s vital to take into account that markets are forward-looking. As we proceed by way of the yr, the main danger to the outlook is that markets begin to see the top of above-average development, which might carry valuations down. As we noticed in 2022’s “tech wreck” on account of rising charges, the drop will be fast and important. Equally, when analysts lowered future expectations earlier this yr, we noticed the Magazine 7 decline considerably. Nonetheless, the expansion of those corporations has produced actual income that may’t be ignored—however buyers could must mood expectations given the excessive valuations.

What About Every thing Else?

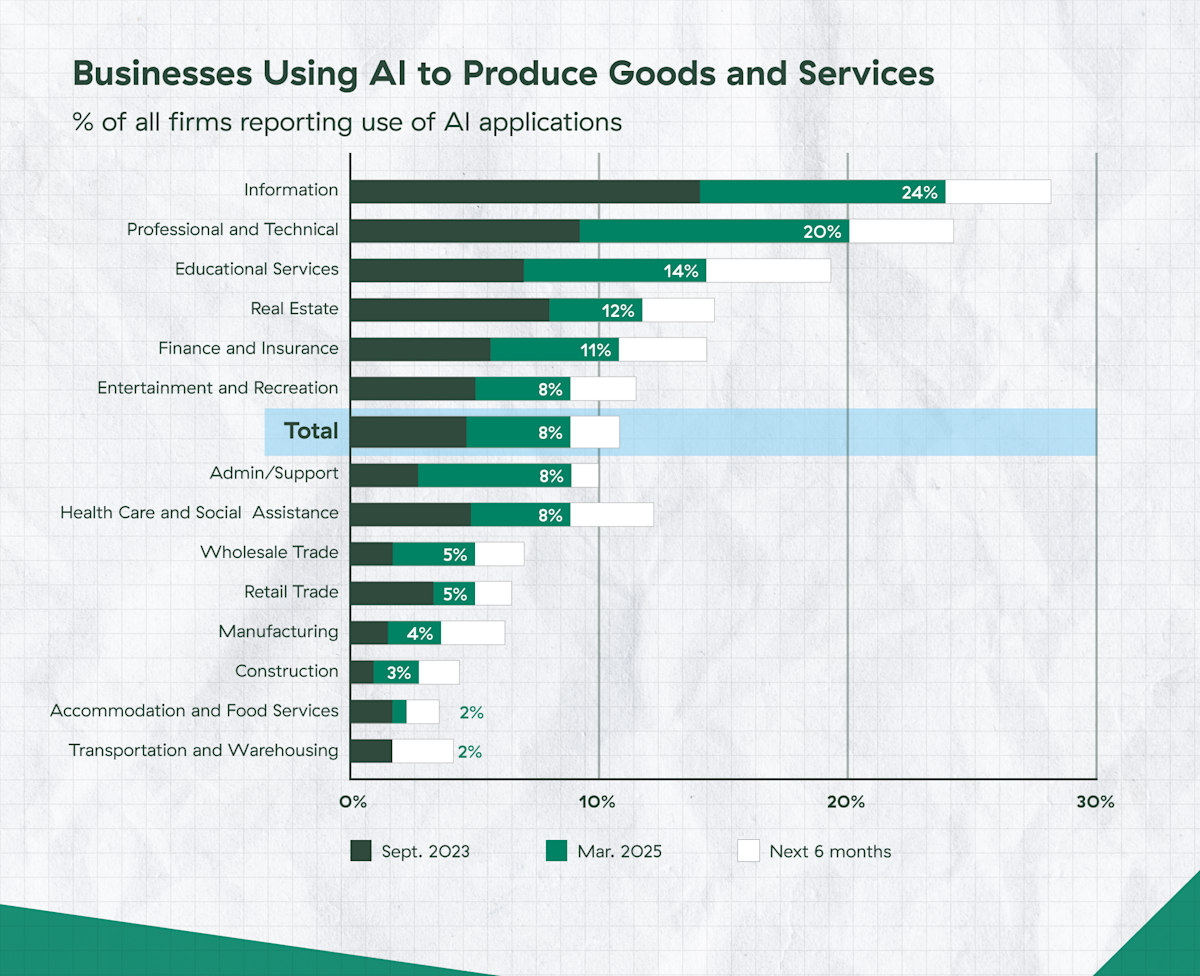

AI’s means to assist enhance productiveness in a still-tight labor market will likely be key to sustaining the Magazine 7’s excessive revenue margins, but additionally the revenue margins of many different corporations. To assist the expansion of the Magazine 7, it can additionally probably be obligatory for AI to have a significant affect on different corporations.

Supply: J.P. Morgan Asset Administration; BEA. Information to the Markets-U.S. Knowledge as of June 6, 2025.

The power to adapt and use AI is definitely prevalent in tech, however it has a number of purposes in different industries. This might assist result in rising development elsewhere (see chart beneath).

Supply: Census Enterprise Traits and Outlook Survey (AI Complement). Information to the Markets-U.S. Knowledge as of June 6, 2025.

2025 earnings development expectations for worth corporations are solely 5 %, in comparison with 14 % for development corporations. Nonetheless, they’re buying and selling at a 40 % low cost on a ahead P/E foundation. This leaves much more room for error if these corporations can’t reside as much as expectations. On condition that analyst estimates have been lowered because of the uncertainty over continued tariffs, there’s nonetheless house for enchancment if the extent of the introduced tariffs continues to say no.

At present, mid-cap corporations have the identical earnings development expectations as large-caps with decrease valuations, whereas small-caps have considerably larger development expectations. Prior to now two years, small-caps haven’t come near assembly excessive expectations, resulting in underperformance. But when projections are in keeping with analyst estimates for 30 % development, there’s important potential there.

Worldwide equities have been the largest story outdoors of the Magazine 7 up to now this yr. The MSCI AC World ex U.S. Index has outperformed the S&P 500 by simply over 13 % (year-to-date by way of June 6, 2025). Nonetheless, after almost a decade and a half of underperformance, these corporations are buying and selling at a big low cost relative to their 20-year historical past. Given the continued optimistic financial surprises taking place internationally, together with still-subdued valuations relative to the U.S., worldwide outperformance might proceed within the second half of the yr.

Lengthy-Time period Performs for Portfolios

Wanting towards the again half of 2025, a number of believable tales might unfold. Markets could rise considerably on the again of elevated AI development, with the remainder of the market seeing strong development and valuations persevering with to construct on elevated pleasure. Or the Magazine 7 could have a reset in valuations, whereas the remainder of the market manages to outperform expectations and markets stay flat. Then there’s the likelihood that financial development might sluggish considerably, hurting each the largest and smallest names.

The underside line is that this: fairness buyers are paid to take dangers. They have to decide what the almost certainly state of affairs is and the way a lot danger they’ll afford. Having publicity to the largest names within the index can nonetheless make sense given their profitability and development prospects. However with the valuation disconnect, worldwide equities and, to a lesser extent, small- and mid-cap names could also be engaging in the long run as the advantages from AI broaden past the Magazine 7.

Do not miss tomorrow’s publish, which is able to function a particular Midyear Outlook version of the Market Observatory.

Sure sections of this commentary include forward-looking statements which can be based mostly on our affordable expectations, estimates, projections, and assumptions. Ahead-looking statements should not ensures of future efficiency and contain sure dangers and uncertainties, that are troublesome to foretell. Previous efficiency isn’t indicative of future outcomes. Diversification doesn’t guarantee a revenue or shield in opposition to loss in declining markets.

The ahead price-to-earnings (P/E) ratio divides the present share value of the index by its estimated future earnings.[JH1]

The Magnificent 7 (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla) are a gaggle of seven corporations generally acknowledged for his or her market dominance, their technological affect, and their adjustments to client habits and financial developments.

The MSCI ACWI ex USA is a free float-adjusted market capitalization weighted index that’s designed to measure the fairness market efficiency of developed and rising markets. It doesn’t embody the US.