{kind=link}

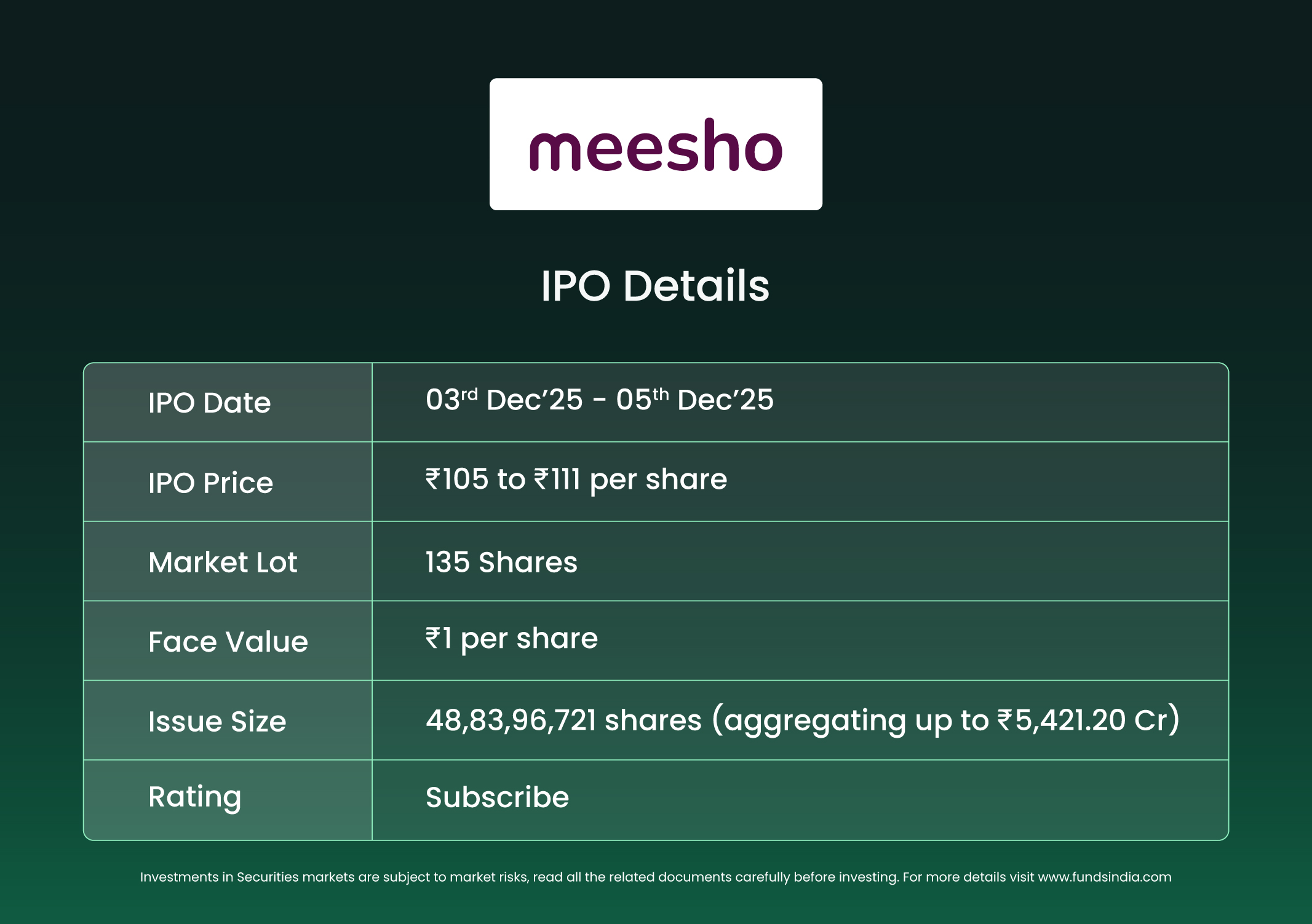

Firm overview

Included in 2015 and headquartered in Bengaluru, Meesho Ltd. operates a multi-sided e-commerce market that connects shoppers, sellers, logistics companions, and content material creators. Meesho’s working philosophy centres on increasing entry to inexpensive on-line buying throughout shopper segments, bolstered by an “on a regular basis low costs” worth proposition. The platform has turn out to be India’s largest e-commerce participant by Positioned Orders and Annual Transacting Customers for the twelve months ended June 30, 2025. The corporate follows a zero-commission market mannequin and generates income primarily by way of vendor providers moderately than shopper costs (zero-platform charges). Its core monetisation streams embrace logistics and fulfilment charges, promoting options and knowledge/perception instruments for sellers.

Objects of the provide

- Funding for cloud infrastructure within the firm subsidiary Meesho Applied sciences Pvt Ltd (MTPL).

- Cost of salaries of present and alternative hires for the Machine Studying and AI and expertise groups for AI and expertise improvement undertaken by MTPL.

- Funding in MTPL for expenditure in direction of advertising and marketing and model initiatives.

- Funding inorganic development by way of acquisitions and different strategic initiatives and normal company functions.

Funding Rationale

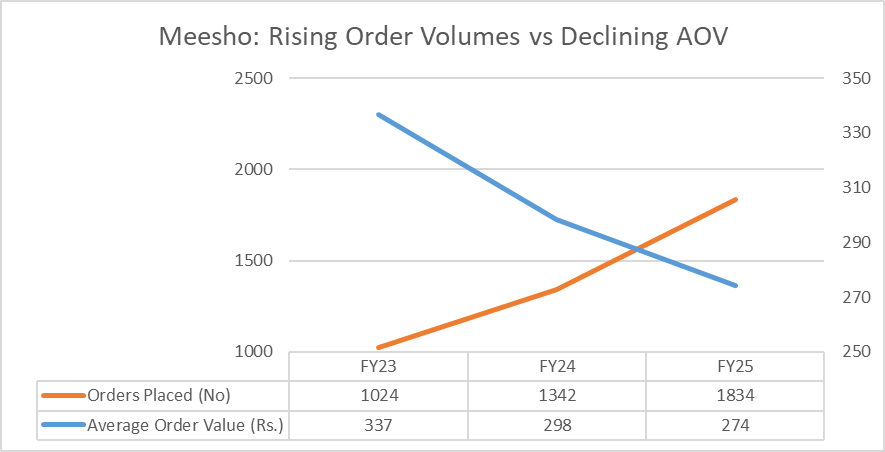

- Centered Penetration in India’s Worth-Aware Shopper Section – Meesho’s core shopper base spans various revenue teams in India, however its strongest adoption comes from value-conscious buyers searching for inexpensive merchandise throughout a large assortment at a single vacation spot. Girls account for 54%+ of its buyer base, reflecting robust traction in on a regular basis way of life and family classes. Whereas India’s total e-commerce person base grew solely 11 – 12% throughout FY23 – 25, Meesho’s annual transacting customers expanded by 46% over the identical interval. This outperformance was pushed largely by semi-urban and rural shoppers (88% orders from exterior Prime 8 cities in India) – segments characterised by regional preferences, vernacular content material consumption, and heavy utilization of low-end smartphones. With 62M month-to-month transactors and 5.1M day by day delivered orders the corporate is driving development of mass market e-commerce in tier 2 and under markets in India. This scale and development have come at close to break-even profitability for Meesho. This shift has additionally resulted in decrease common order values however considerably larger order frequencies, validating Meesho’s positioning because the platform of alternative for high-volume, low-ticket retail.

- Low value and asset mild enterprise mannequin – Meesho operates a technology-led, asset-light market with a zero-commission construction for sellers and no platform charges for shoppers, enabling low-cost order fulfilment. This allows sellers to supply a large, inexpensive assortment spanning unbranded items, regional labels and nationwide manufacturers, reinforcing Meesho’s value-led positioning. Scale advantages and ecosystem integration have allowed the corporate to introduce complementary initiatives corresponding to low-cost native logistics community and monetary providers, forming the 2 enterprise segments of Market and New Initiatives. The corporate’s “on a regular basis low costs” moderately than Low cost cycles and event-based sale spikes proposition ensures shoppers entry inexpensive merchandise with out dependence on flash gross sales or time-bound reductions. As scale expands, the common value charged to sellers continues to say no, reflecting working leverage and platform efficiencies.

- Proprietary Platform Underpinned by Self-Reinforcing Flywheels – The Firm operates a multi-sided expertise platform that drives e-commerce in India by connecting 4 key stakeholders: shoppers, sellers, logistics companions, and content material creators. This platform is constructed on multiple-scale self-reinforcing flywheels, which generate huge quantities of information concerning shopper preferences, pricing developments, vendor efficiency, and content material attractiveness. This data-driven method allows the Firm to adapt quickly and constantly to enhance its choices, supporting long-term competitiveness and development.

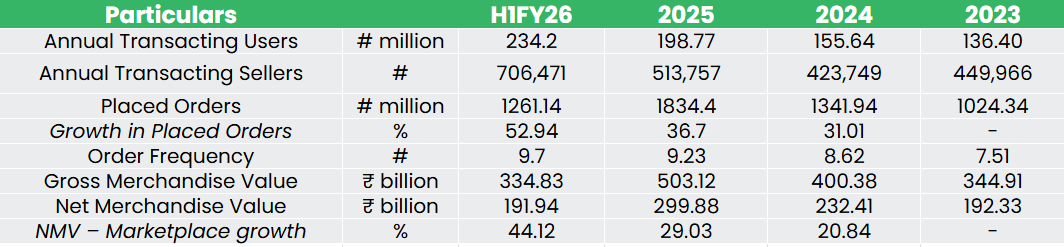

- Robust operational KPIs with current acceleration in NMV and Order Development – Meesho’s working metrics replicate robust platform momentum, with Annual Transacting Customers rising from 136 million in FY23 to over 234 million by H1Y26 and a rising vendor base exceeding 7,06,471, which collectively improve assortment depth and pricing competitiveness. The corporate’s current NMV and order development charges have exceeded expectations, registering a forty five% YoY improve in NMV and a 51% YoY development in customers in H1FY26. Next few quarters of margin consolidation, the corporate has shifted its focus again to larger development, from mid-20s to mid-40s now. The corporate goals to keep up this development trajectory over the following 24 months. The constant rise throughout customers, sellers, orders and NMV additionally demonstrates rising working leverage and reinforces Meesho’s capability to maintain its on a regular basis low-price worth proposition, rising engagement and platform stickiness.

- Monetary Efficiency – Income from operations elevated from Rs.57.3 billion in FY23 to Rs.93.9 billion in FY25, reflecting larger order frequency and improved vendor monetisation. Profitability metrics tracked a gradual enchancment on the again of fulfilment value efficiencies and working leverage. The three months ended June 30, 2025, nonetheless, mirrored a better loss run-rate attributable to distinctive restructuring bills, elevated ESOP costs and quickly larger logistics/cloud prices, moderately than weakening fundamentals. Excluding these one-off gadgets, enterprise momentum continued to development positively. General, the monetary trajectory displays a scaled market with bettering unit economics, growing monetisable throughput and a narrowing path to breakeven.

- Consecutive Quarters of Robust Money-Movement Technology, Nicely Capitalized with $629M in Financial institution – Meesho has pushed consecutive quarters of PAT break-even and robust cashflow, producing 591 Cr. of Free Money Movement in FY25 pushed by 15 days of damaging working capital. The Firm continues to stay very properly capitalized with $629M (INR 5,536 Cr.) money in financial institution. A $275M tax legal responsibility is but to be realised (stemming from the entity flip from Delaware to India) and the Firm is elevating $300M within the IPO which can take the money place again to ~$650M submit IPO.

Business Tendencies

The Indian retail market, valued at roughly Rs.83 trillion (USD978 billion) in FY25, is projected for sustained growth at a CAGR of 8 -10% to Rs.123 – Rs.135 trillion (USD1.4 – 1.6 trillion) by FY30. This development is basically supported by India’s favorable macroeconomic components, growing urbanization, and vital consumption uptake throughout Tier 2+ cities. The provision aspect stays extremely fragmented, with regional manufacturers and unbranded merchandise forecasted to retain a considerable share of 70 – 74% of whole retail spends by FY30. Organizing this fragmented provide is essential, positioning organized retail (together with e-commerce) to seize 32 – 34% of the market by FY30. Inside this section, e-commerce is the fastest-growing format, projected to develop robustly at a 20 – 25% CAGR to achieve Rs.15 – 18 trillion (USD174 – 214 billion) by FY30. The first driver for this future development lies in non-electronics classes, the place penetration stays low (roughly 5%). Worth-focused e-commerce platforms are strategically designed to deal with India’s affordability-led demand by effectively aggregating fragmented provide, a enterprise mannequin that has confirmed dominant in mature markets corresponding to China.

Key dangers

- Sustained Profitability Nonetheless Unproven – Regardless of robust scale advantages and bettering unit economics, the corporate stays loss-making. Profitability is delicate to fulfilment prices, cloud bills and employee-related prices; any delay in value optimisation or larger spending to drive development may lengthen the trail to break-even.

- Aggressive Depth & Replication Danger – Present gamers and new entrants have the monetary capability to focus on the worth/everyday-low-price section and make investments aggressively in logistics and incentives. Replication of Meesho’s mannequin – particularly in Tier-2/3 markets and low-AOV classes – may stress margins and retention.

- Energy of high quality management programs – As a result of Meesho permits very giant variety of small, usually unbranded or casual sellers (together with home-based sellers, small producers, reseller/distributors, and many others.), the variability in high quality manufacturing requirements, packaging, and compliance stays excessive.

Outlook

The corporate has constructed a defensible place within the value-first, low-AOV section, concentrating on semi-urban and rural India the place e-commerce penetration stays underdeveloped. Continued scale advantages and working efficiencies – particularly by way of its proprietary logistics platform, Valmo – are anticipated to drive additional margin enchancment. Whereas the corporate has traditionally incurred losses since inception, current operational momentum exhibits enchancment, having achieved optimistic Final Twelve Months Free Money Movement (LTM FCF) in FY24 and FY25.

On valuation, Meesho’s implied Worth-to-Web Merchandise Worth (P/NMV) for LTM seems cheap relative to listed friends. The corporate’s implied P/NMV of ~1.54× is positioned under Everlasting (~3.45×), Swiggy (~1.96×) and considerably decrease than Nykaa (~8.93×), inserting it on the decrease finish of the peer spectrum. The low cost positioning on a P/NMV foundation supplies valuation assist.

Whereas near-term earnings visibility stays restricted, the long-term development alternative, robust market match, and bettering fundamentals assist participation with a medium-term outlook. Based mostly on the above views, we offer a “Subscribe” score for the IPO.

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please notice that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you might like

Publish Views:

48