: “Investing like a “billionaire” for retail buyers within the UK inventory market through PE Trusts")

Non-public Fairness Mini sequence (4) : “Investing like a “billionaire” for retail buyers within the UK inventory market through PE Trusts

That is the 4th a part of my Non-public Fairness “mini” sequence. The earlier posts could be discovered right here:

Non-public Fairness Mini Collection (1): My IRR isn’t your Efficiency

Non-public Fairness Mini sequence (2) – What sort of “Alpha” are you able to count on from Non-public Fairness as a Retail Investor in comparison with public shares ?

Non-public Fairness Mini Collection (3): Listed Non-public Asset Managers (KKR, Apollo & Co)

Background:

Unsure if that is primarily a German phenomenon, however you may’t hearken to a German finance podcast with out being fairly aggressively marketed on how Non-public Fairness is lastly being democratized by some “revolutionary” retail choices that just about at all times are fairly sophisticated and include one other layer of charges on prime of what the PE guys are charging.

The principle pitch is that now even the small man on the road can do what beforehand solely billionaires may do: Make investments into Non-public Fairness and make boat a great deal of cash.

The onerous fact is that Non-public Fairness has been democratized way back within the UK however nobody provides a sh** about it.

UK listed Non-public Fairness Trusts

Within the UK, there’s a custom that just about any unlisted or listed asset class will get repackaged as an open ended fund or “Belief” which generally could be traded as straightforward as some other inventory on the UK inventory market.

The Glorious Verdad capital weblog just lately had a submit about these trusts specializing in two facets:

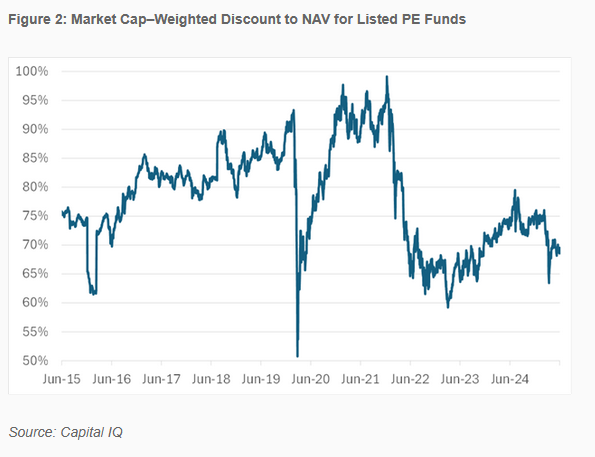

- These traded funds present (after all) a a lot increased volatility than the underlying “smoothed” NAVs

: “Investing like a “billionaire” for retail buyers within the UK inventory market through PE Trusts")

These clearly exhibits that in actuality, PE belongings are usually not much less unstable than public markets, they simply look much less unstable due to the is aware of points (Quarterly valuations, “Volatility laundering” and so forth.)

- On common, these funds commerce at 70 cents on the greenback. So not solely does this asset class supply entry to retail buyers, however even at “juicy” reductions:

Diving deeper

So let’s dive somewhat bit deeper into these trusts

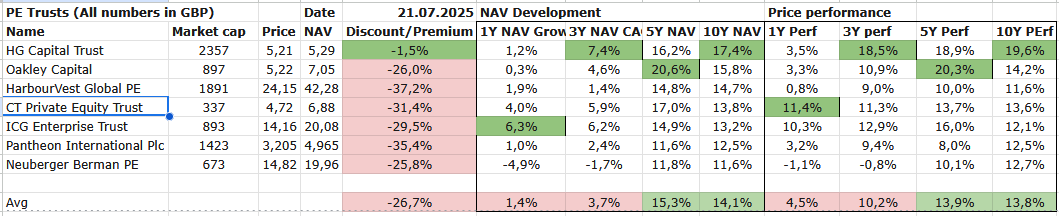

Citywire provides us in precept 13 totally different listed PE Trusts. I’ve chosen 7 of them that truly have at the very least 5 yr historical past and a PE focus.

Listed below are the NAV reductions and Efficiency Numbers (NAV & Share value) over 1.3,5 and 10 years.

NAV Reductions

What we are able to see is that every one 7 trusts commerce at reductions, on common a whopping -27% to NAV.

What’s perhaps not stunning is the truth that one of the best performing fund over 10 years, Hg capital has the bottom low cost. What I discover fascinating is that the remainder of the trusts don’t present a transparent sample. Oakley, which has a nonetheless first rate efficiency over 10 years, has the identical low cost because the Neuberger Berman automobile that carried out considerably worse.

Efficiency

Probably the most fascinating side of this complete train is for my part that we are able to see right here “actual” efficiency as these automobiles really reinvest money flows in comparison with the standard IRR numbers of single PE funds.

Wanting on the chart once more it is vitally hanging, that for the previous 1 yr and three years, NAV efficiency and Value efficiency was fairly weak on common for the entire group..

My interpretation is as follows: Most PE funds have “smoothed” over destructive 2022 efficiency. Nonetheless, as Non-public Fairness is usually small- to midcap targeted, they couldn’t take part within the massive cap rally of 2023 and 2024.

However nonetheless, the ten yr numbers look fairly first rate. Nonetheless, these are efficiency numbers in GBP and the efficiency has benefitted from a stronger USD as many of the funds have important USD publicity. In USD, 10 yr efficiency can be round -1,6% p.a. decrease.

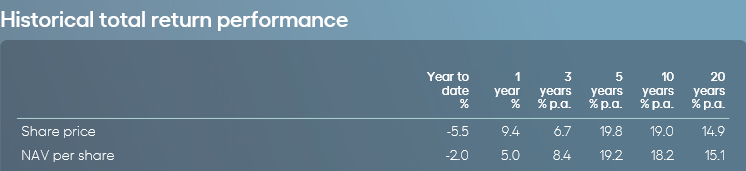

For these funds which have an extended monitor report, 20 yr numbers are decrease than 10 yr numbers.

Hg as an illustration seems to be as follows:

Over 20 Years, the FX tailwind was round 2,5% p.a., adjusted for this, an investor has made round 12,5% p.a. which is nice however clearly not out of this world. For my part, one thing round 12-15% actual world return is one of the best you get from a prime class Non-public Fairness fund in the long term. On common, after charges, that quantity is clearly decrease, not a lot totally different from public markets for my part.

One other fascinating truth is that the 2 finest performing funds, Hg Capital and Oakley each make investments straight into their very own offers, whereas all of the others are extra oblique “fund of fund” automobiles that make investments into Funds and/or Co.Investments of different PE GPs.

Charges, Charges, Charges. & Prices

Initially, I needed to do a comparability of the charges between the automobiles, but it surely turned out to be an excessive amount of of a trouble. Some Trusts report the charges fairly transparently, for some it’s actually onerous to seek out the essential info on charges.

ICG is sort of clear and has the bottom value & Charges with a complete cost of 1,38% at automobile stage. Nonetheless, a major a part of the portfolio is invested into different funds which once more cost charges that aren’t included within the 1,38%.

As talked about, Oakley and Hg solely make investments into their very own funds and haven’t any further Administration charges on belief stage however after all “typical” PE funds charges that may be 4% p.a. in a very good yr.

The Neuberger Berman automobile solely invests into low payment co-investments type different GPs however this clearly doesn’t assist the efficiency a lot.

Enjoyable truth: German “Neo PE for the lots” participant Liqid is providing a product (Liqid NEXT) that appears to have the very same technique just like the NB automobile simply packaged as an “ELTIF II automobile”. Nonetheless, the Liqid product consists of some provisions (deal by deal carry) that can make it even worse for buyers.

For my part, being so opaque about charges and prices isn’t a bug however a function of the entire Non-public Fairness business. The business has gotten away with charging terribly excessive charges for a number of a long time now and I ponder how lengthy it will stay to be so.

Valuations

One other concern is that not each PE fund is clear concerning the valuation of the portfolio firms. Sure, a 30% low cost to NAV sounds good, however a reduction for one thing that’s extraordinarily overpriced could be a foul deal.

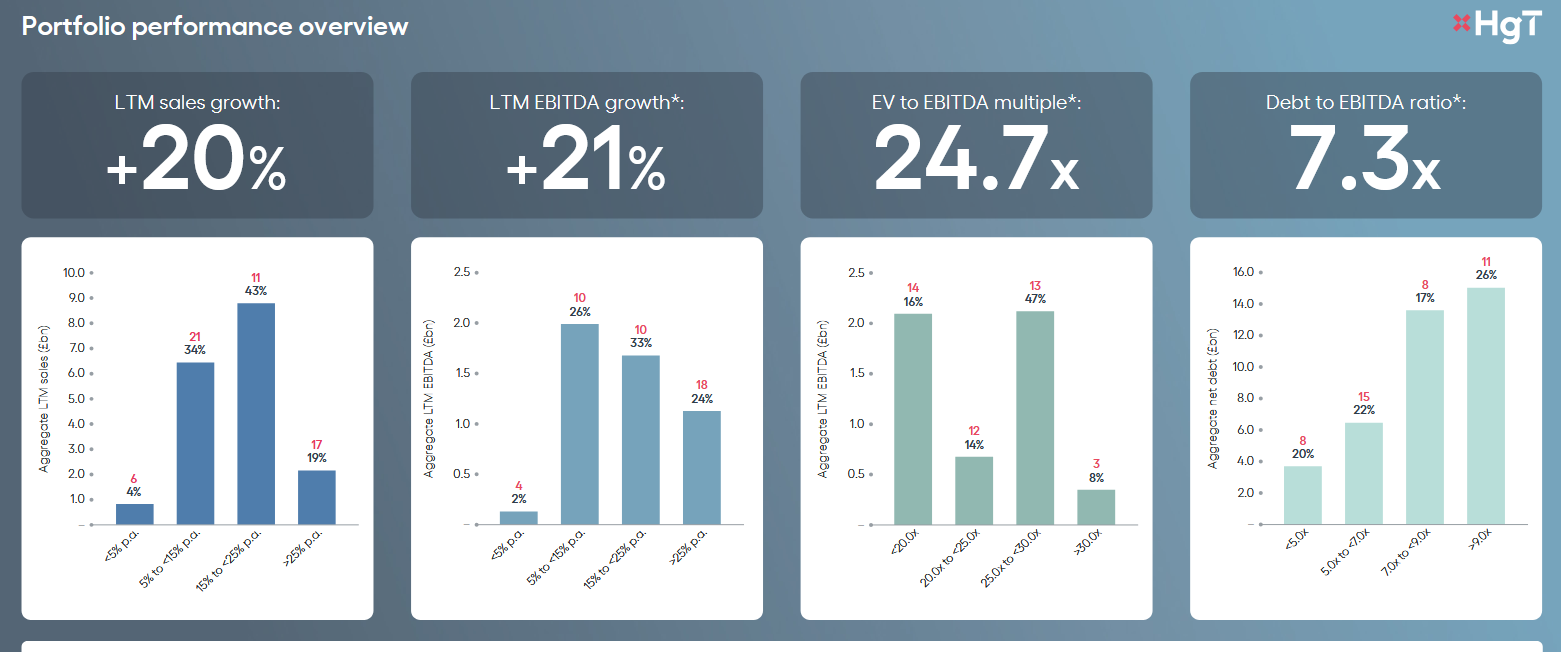

Wanting on the Scoreboard chief HG Capital, they’ve at the very least a fairly informative valuation slide:

A mean valuation of ~25x EV/EBITDA is clearly errrm not low-cost. Nonetheless, their firms are rising however debt can also be fairly excessive. Hg capital is usually a Software program PE investor.

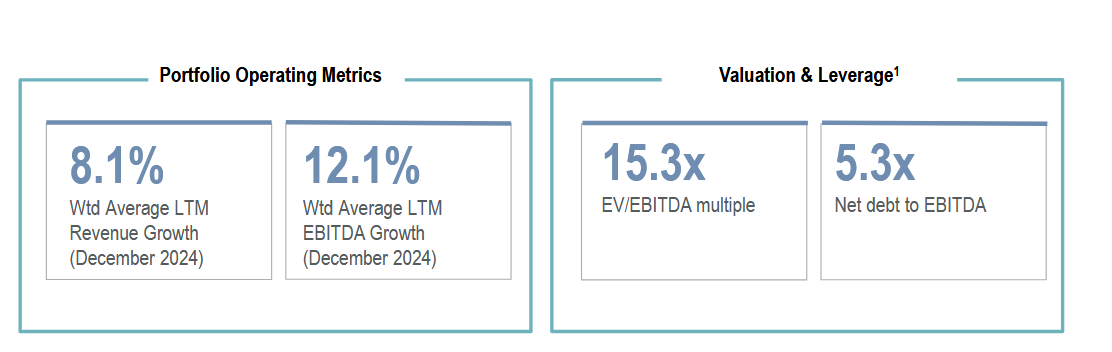

NBPE has a considerably extra basic decrease development portfolio, however a valuation of 15x EV/EBITDA isn’t low-cost both:

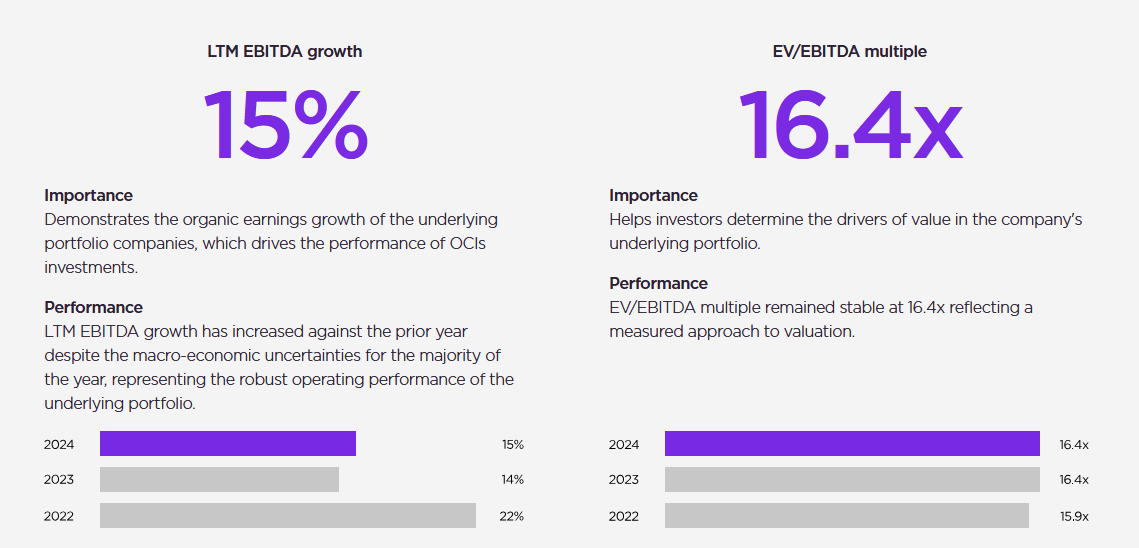

Oakley is someplace in between with ~15% development and 16,4x EV/EBITDA

In abstract, at the very least to me, valuations look fairly stretched. If I wish to pay 15xEV/EBITDA, I’ve a large alternative of prime notch high quality firm in public markets. Even at a 30% low cost, that is nonetheless not dust low-cost, particularly contemplating the slightly excessive leverage of many of those firms.

I guews that is additionally the principle drawback for the PE GP’s: At these valuations, it’s not that straightforward to IPO any of those firms, until you’re a Protection/AI firm/AI Chip firm.

Abstract – what now ?

I’m not right here to offer funding recommendation, however in the event you desperately want PE publicity, this listing could be one of the best place to take a look at as a retail investor.

If I had been pressured to purchase 2 of these trusts, I might more than likely go for Oakley (good monitor report, first rate low cost) or ICG (low charges). A 3rd can be Hg as that is actually a prime notch PE, however you might want to be snug with Progress firm valuations.

For me personally as a price investor, regardless of the reductions, the general valuation seems to be considerably streched. On the present valuation of those funds, I might assemble a fantastic high quality portfolio that, with out the PE charges, will more than likely outperform the PE guys in the long term.

In comparison with the flowery new “ELTIF II” automobiles, these trusts are clearly less complicated, extra clear and liquid every day. The one benefit of ELTIF buildings is that you simply don’t see the volatility.