Sequence 6: Non-public Fairness for the lots – Y2K version")

{kind=link}

Earlier Episodes of the Non-public Fairness (Mini) Sequence:

Non-public Fairness Mini Sequence (1): My IRR just isn’t your Efficiency

Non-public Fairness Mini collection (2) – What sort of “Alpha” are you able to count on from Non-public Fairness as a Retail Investor in comparison with public shares ?

Non-public Fairness Mini Sequence (3): Listed Non-public Asset Managers (KKR, Apollo & Co)

Non-public Fairness Mini collection (4) : “Investing like a “billionaire” for retail traders within the UK inventory market by way of PE Trusts

Non-public Fairness Mini Sequence (5): Commerce Republic affords Non-public Fairness for the lots (ELTIFs) -“Good attempt, however hell no”

Time Machine: Y2K

Among the older readers of my weblog may need lively reminiscences concerning the 12 months 2000. There was the so-called “2YK Scare” within the late 1990ies, the concern that pc methods (and planes) would crash when the 12 months 2000 would begin. After all it didn’t occur, the Dot.com bubble acquired pumped up as soon as extra and the remainder is historical past.

One other occasion that acquired much less consideration was the that again within the 12 months 2000, the now lengthy gone Dresdner Financial institution issued a Certificates (which is a well-liked construction in Germany to present retail traders publicity to something) that was really a bond linked to the long run returns of an underlying Non-public Fairness Portfolio managed by Swiss PE supervisor Companions Group. The exact same Companions Group that now has teamed up with Deutsche Financial institution to run an ELTIF.

Though I used to be not capable of find the unique prospectus (Stories on the internet web page solely return to 2019) , the attention-grabbing side of this certificates is that it has been traded since 2003 and subsequently offers us the possibly longest observe report of a real, long run “retail Non-public Fairness Efficiency”.

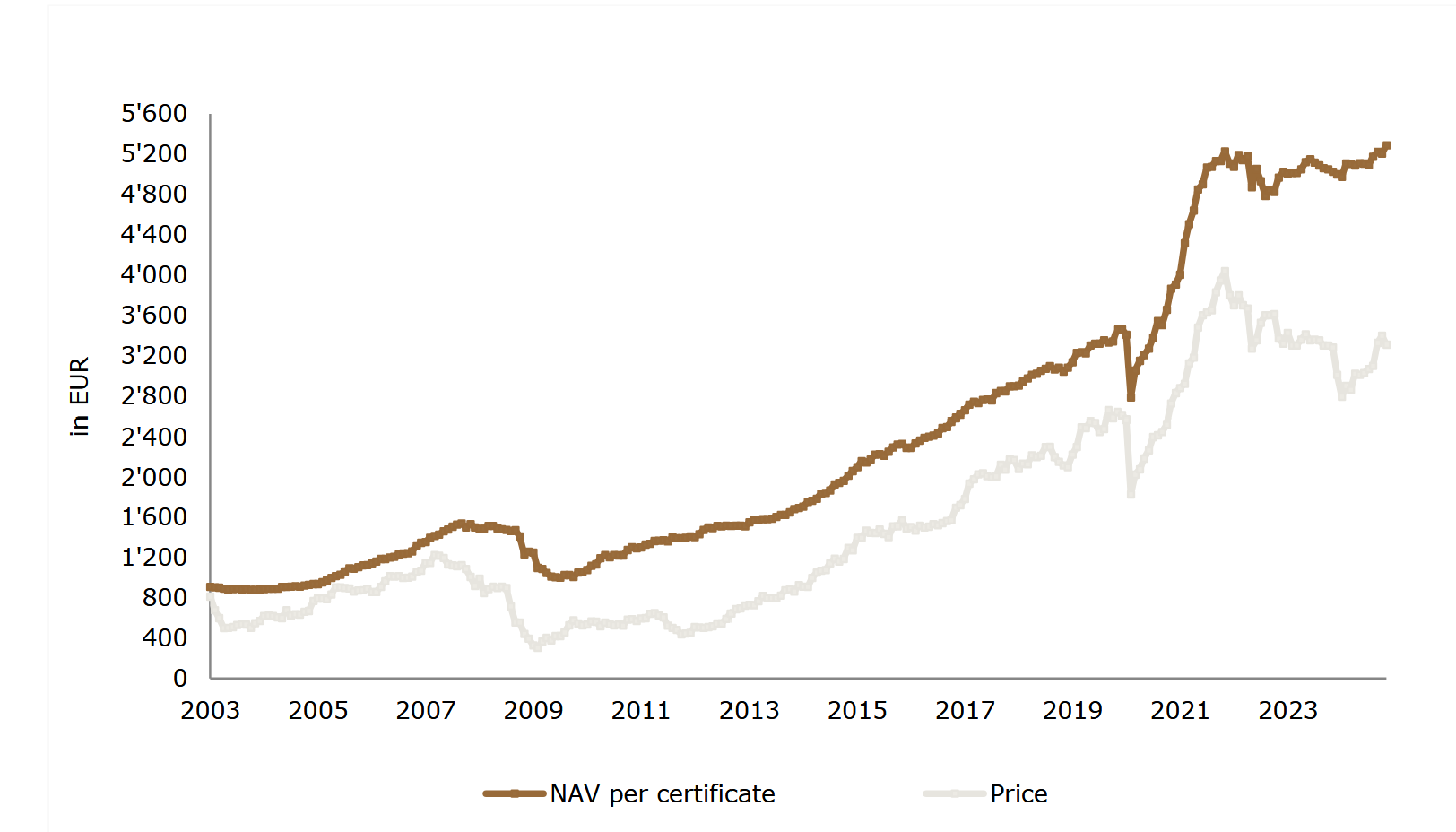

So that is how this 22 12 months chart seems like:

Sequence 6: Non-public Fairness for the lots – Y2K version")

The traded certificates doesn’t look too dangerous, however 22 years is an extended time period. So let’s examine it to the DAX and the MDAX and there it will get attention-grabbing:

Even the Sleepy DAX and MDAX outperformed that product by a large margin. Taking a look at annualized complete return, that is what Bloomberg tells us:

So this Non-public Fairness Certificates managed to return 8,31% or -2,7% p.a. lower than the DAX in the identical 22 years and 6 months. The underperformance to the MDAX which might e a greater proxy is even increased.

Even when I take the entire NAV efficiency acknowledged within the 2024 which is 428,8% and annualize it over 24 years, I get solely an annual return of ~7,2% p.a. from 2000 to 2024 for the certificates house owners.

How does that Certificates make investments & what are the charges ?

Wanting into the annual report, we will see that the underlying technique is a world, Buyout centered PE technique with a portfolio diversified over many asset managers and a excessive proportion of direct/co investments.

The payment construction is kind of just like what we’ve got seen in lots of different retail constructions: On the car degree, a payment of 1,5% flat on PE investments plus a 15% carry (5%) hurdle fee plus the charges of the underlying funds.

We can see within the annual account that the car charged the traders 13,5 mn charges and prices in 2024 primarily based on round 580 mn in complete so round 2,6% in a 12 months with low efficiency.. In 2021, which was a greater 12 months, they charged 24 mn on 700 mn, so 3,5% (plus the charges of the underlying funds which aren’t explicitly disclosed.

There isn’t any annual kickback to the distributor in comparison with the Commerce Republic EQS product.

So why is the efficiency so dangerous compared to even DAX and MDAX ?

I imply they need to have captured the perfect years of Non-public Fairness and didn’t even handle to beat the old-fashioned, non-tech DAX Index ?

One issue is clearly the present low cost of the value of the certificates to NAV, which on the time of writing is a round -35%. Even when we’d alter for this, we’d nonetheless not be capable to beat the Loser indices DAX and MDAX for 22 years.

One other issue is that they appear to have hedged out the USD. The tailwind of a robust USD is commonly included in previous EUR returns acknowledged by PE gross sales folks however will after all not essentially be repeated. So the hedged efficiency numbers are higher predictors for the longer term in my view.

The start line of the time collection in early 2003 may be a difficulty as this was roughly a decade low for the DAX index. However as we’ve got seen, the entire return since inception has solely been 7,2% and much away from the customarily talked about “double digit” returns.

Possibly they’ve chosen the improper funds ? The names within the portfolio are literally tier 1 family fund names. KKR, Cinven, Vista, Permira and so on. These are all good names. However after all, we have no idea what they did within the early years. However Companions Group is a profitable PE supervisor, so I assume that this isn’t the problem.

What’s more durable to evaluate is that if they’ve possibly gotten solely the weaker a part of the co-Funding pipeline, as a big portion of the present portfolio are co-investments.

However the “arduous reality” is:

With out all of the IRR shenanigans of Institutional PE funds and the extra payment layers of a retail product, the true efficiency of a retail PE product is simply not excellent and can almost certainly not beat a low price inventory index fund, fairly the alternative.

NAV low cost

One other attention-grabbing side of this safety is that at the least over the last 22 years, the certificates at all times traded at a major low cost to its acknowledged NAV. That is the graph from their 2024 report:

this mirrors the expertise from the UK listed autos that always commerce at vital reductions, too.

Commerce Republic introduced that they need to implement an “inner market place” the place traders can promote month-to-month. My guess is that traders will be unable to promote at NAV but when in any respect, at fairly steep reductions of 20-30%. I’m actually curious if we really see trades on this inner market place in any respect.

As soon as once more: Don’t play within the On line casino, personal the On line casino

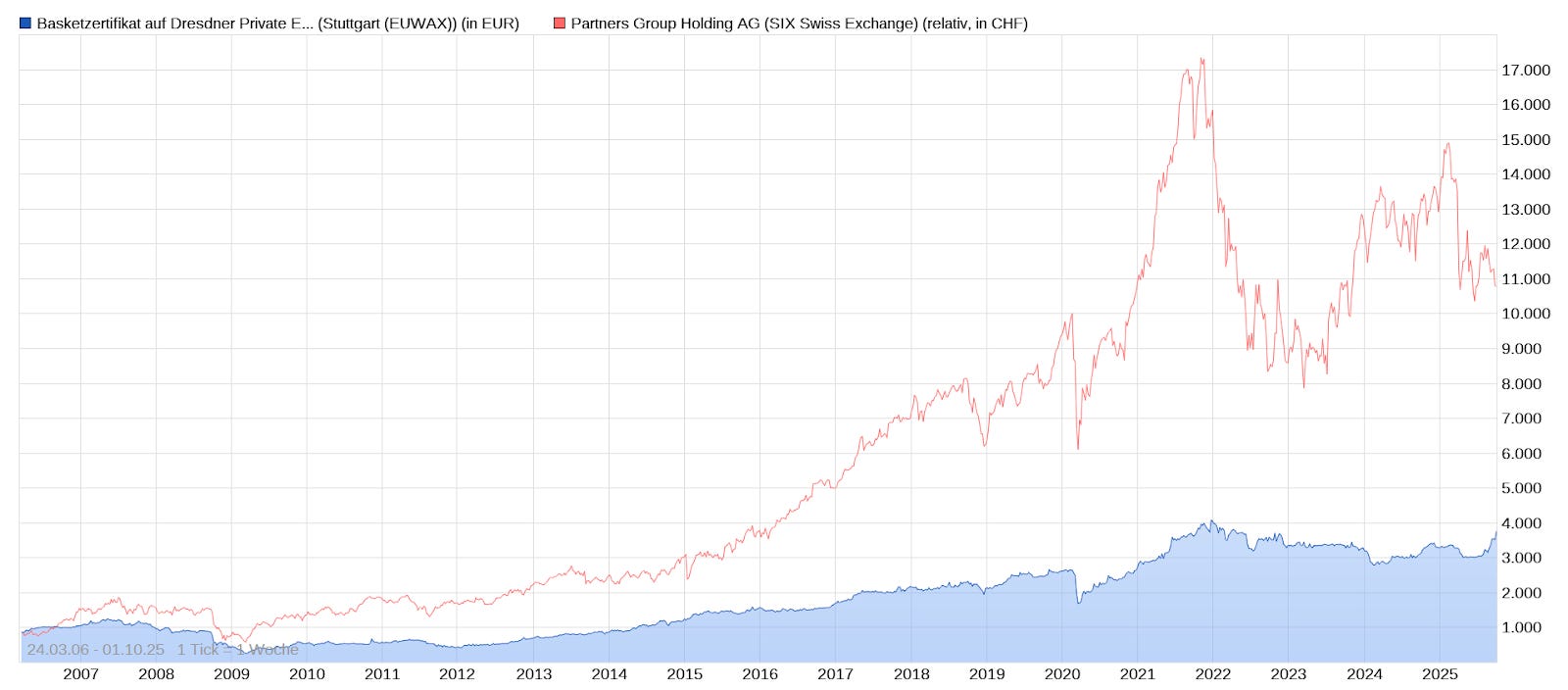

And final however not least, my favourite comparability: Companions Group was one of many earliest PE outlets to go public in 2006. That is how the inventory of companions Group did in comparison with the certificates that they handle:

As anticipated, you’ll have made multiples of the cash investing into the GP as an alternative of the underlying property. And that is clear: As a partial proprietor of the GP, you achieve from excessive charges and a possible constructive improvement of the underlying property, however your draw back is restricted, as it’s not your individual cash.

As a good friend would say: Losers play within the On line casino, winners purchase the On line casino.

So as soon as once more, my advice is obvious: In the event you consider in the way forward for Non-public Fairness, shopping for the GP by way of their listed shares will almost certainly be the higher alternative than going by excessive payment retail merchandise.

As a cliffhanger, within the subsequent episode I’ll take a look at one instance of a safety that provides you a comparatively truthful publicity to PE funds should you actually desperately search for it.

Abstract:

The Dresdner Financial institution PE Certificates issued in 2000 provides a really practical view of what retail traders can count on in “actual world efficiency” for Retail Non-public Fairness providing.

Over a interval of twenty-two years and 6 months (since this product is buying and selling), any retail traders would have outperformed this product with a easy and straightforward DAX Index fund by a large margin of two,7% p.a. As a substitute of a 6x with the Certificates, good outdated DAX would have given you a 10x in the identical interval.

The commonly marketed double digit returns (after charges) for Retail PE merchandise are in my view a complete fantasy and are constructed upon previous, “massaged” IRR numbers that aren’t an excellent information for actual world efficiency.

I’m actually curious, what number of retail traders will get sucked into these traps. Possibly these articles assist a few of my reader (and their associates) to keep away from these merchandise.