{kind=link}

NTPC Ltd. – Main India’s Energy Sector

Established in 1975 and headquartered in New Delhi, NTPC Ltd. is an Indian Public Sector Enterprise (PSU) primarily concerned within the era and sale of bulk energy. It’s a vertically built-in firm overseeing your entire strategy of energy era and distribution. As of FY24, NTPC boasts an put in capability of 75,958 MW (together with JVs) and goals to turn out to be a 130 GW firm by 2032. The corporate’s power portfolio contains 35 coal, 11 gasoline/naphtha, 29 photo voltaic, 11 hydro, and three wind-based energy vegetation. Notably, 4 of its coal stations ranked among the many high 10 performing stations within the nation when it comes to Plant Load Issue (PLF) in FY24.

NTPC’s Product Portfolio:

Enterprise verticals of NTPC are energy era (thermal, renewable together with photo voltaic & wind, hydro, and nuclear), inexperienced hydrogen and chemical compounds, mining, waste to power, power buying and selling, consultancy companies, EV ecosystem, and ash administration.

What number of Subsidiaries does NTPC have?

As of FY24, NTPC has 10 subsidiaries and 16 three way partnership firms, enhancing its operational scope and market attain.

NTPC Development Methods

Capability Growth:

- Expanded business capability by 3924 MW in FY24.

- Elevated captive coal manufacturing by 48% from 23.20 MMT in FY23 to 34.39 MMT in FY24.

- Plans to award a further 15.2 GW of thermal capability and enhance coal mining capability to 50 million tonnes yearly inside three years.

Strategic Development Plans:

- NTPC Inexperienced Vitality Restricted (NGEL) partnerships for Inexperienced Hydrogen initiatives in Gujarat.

- MoU with Gujarat Pipavav Port Ltd. for Inexperienced Ammonia manufacturing and offshore wind farm exploration.

- Energy Buy Settlement with Damodar Valley Company for 310 MW photo voltaic tasks.

Renewable Vitality:

- Aiming for 45-50% capability from non-fossil fuels by 2030.

- Commissioned 3.6 GW of renewable power tasks with a further 8.4 GW underneath development and 11.2 GW within the tendering course of.

- MoU with the Authorities of Maharashtra for inexperienced hydrogen, pump hydro, and renewable power tasks.

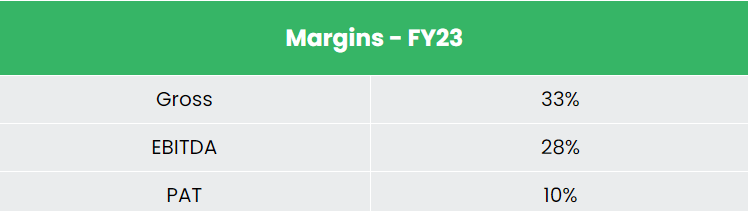

Monetary Report of NTPC:

Q4FY24:

- Income: Rs.47,622 crore, an 8% enhance from Q3FY23.

- EBITDA: Rs.13,984 crore, a 17% enhance from Q3FY23.

- Internet Revenue: Rs.6,490 crore, a 33% YoY enhance.

- EBITDA margin at 29% and web revenue margin at 14%.

FY24:

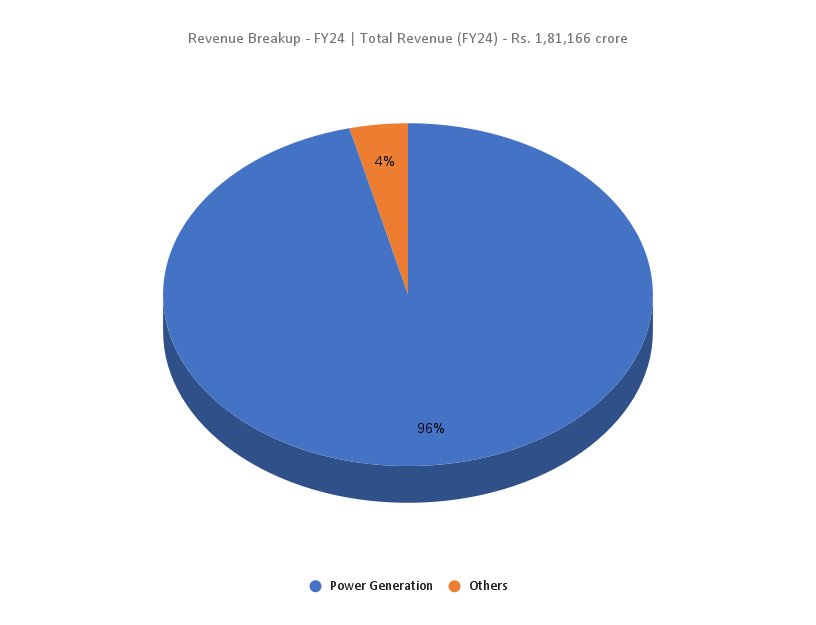

- Income: Rs.1,81,166 crore, a 2% YoY enhance.

- Working Revenue: Rs.51,093 crore, a 7% YoY enhance.

- Internet Revenue: Rs.21,332 crore, a 25% YoY enhance.

- Generated 422 Billion Models, up 6% from FY23.

- Common PLF of NTPC coal stations at 77.25%, 8% above the nationwide common.

Monetary Efficiency:

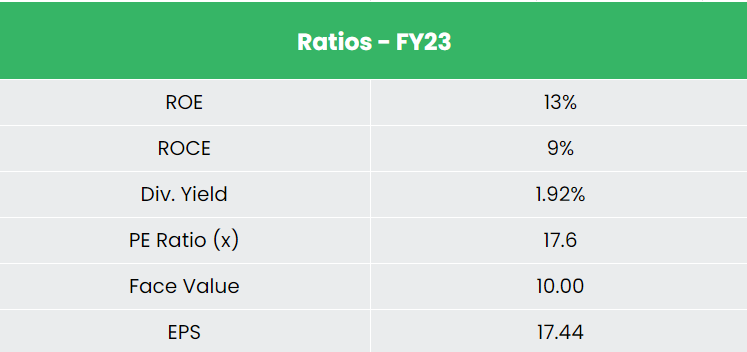

- Income and PAT CAGR of 17% and 9% over FY21-24.

- Common 3-year ROE & ROCE at round 13% and 10%, respectively.

Trade Outlook:

- Numerous Energy Sector: India’s energy sector contains coal, lignite, pure gasoline, oil, hydro, nuclear, wind, photo voltaic, agricultural, and home waste sources.

- Future Development: Projected energy requirement of 817 GW by 2030.

- Renewable Vitality Growth: CEA estimates a rise in renewable power era share from 18% to 44% by 2030.

- Thermal Vitality Discount: Anticipated lower in thermal power share from 78% to 52% by 2030.

- Authorities Initiatives: Plans to determine a renewable power capability of 500 GW by 2030.

Development Drivers:

- Growing Electrification: Rising inhabitants and per-capita utilization.

- Authorities Assist: Vital price range allocation for inexperienced hydrogen, solar energy, and green-energy corridors.

- FDI: 100% Overseas Direct Funding within the energy sector, attracting US$ 18.17 billion from April 2000 to December 2023.

Comparability with NTPC’s Opponents:

Amongst opponents like Tata Energy and Energy Grid Company, NTPC stands out as probably the most undervalued inventory with steady returns on capital and wholesome income progress.

Outlook:

- Thermal Capability Growth: Plans to award 15.2 GW thermal capability by FY26.

- Renewable Vitality Targets: 60 GW by 2032.

- Capex Plans: Rs.35,000 to Rs.50,000 crore over the subsequent 2-3 years.

- Sustained Demand: Advantages from constant electrical energy demand.

- Authorities Backing: Offers sustained income visibility for medium to long run.

- Futuristic Plans: Concentrate on renewable power and strategic partnerships.

Valuation:

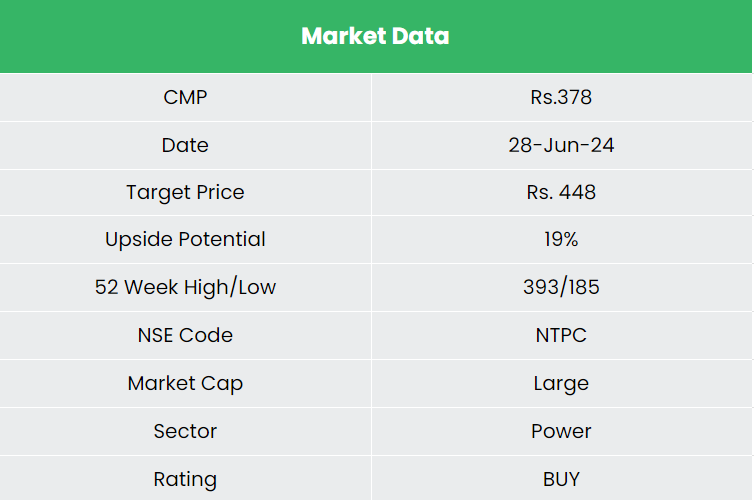

We suggest a BUY score for NTPC Ltd., with a goal value of Rs.448, primarily based on 17x FY26E EPS, reflecting its progress potential and strategic initiatives.

Dangers:

- Monetary Danger: Excessive dependence on debt for growth tasks.

- Execution Delay: Potential delays in thermal and renewable power tasks impacting turnover.

Observe: Please observe that this isn’t a suggestion and is meant just for academic functions. So, kindly seek the advice of your monetary advisor earlier than investing.

Recap of our earlier suggestions (As on 28 June 2024)

Motherson Sumi Wiring India Ltd

Different articles chances are you’ll like

Put up Views:

144