Final Wednesday (August 28), the market waited with bated breath for Nvidia’s incomes name, scheduled for after the market closed. That decision, at first sight, contained exceptionally excellent news, with revenues and earnings coming in at stratospheric ranges, and above expectations, however the inventory fell within the aftermath, down 8% in Thursday’s buying and selling. That drop of greater than $200 billion in market capitalization in response to what appeared like excellent news, no less than on the floor, puzzled market observers, although, as is their wont, they’d discovered a motive by day finish. This dance between firms and buyers, enjoying out in anticipated and precise earnings, is a function of each earnings season, particularly so in america, and it has at all times fascinated me. On this put up, I’ll use the Nvidia earnings launch to look at what information, if any, is contained in earnings reviews, and the way merchants and buyers use that information to reframe their eager about shares.

Earnings Reviews: The Elements

Once I was first uncovered to monetary markets in a classroom, I used to be taught about info being delivered to markets, the place that info is processed and transformed into costs. I used to be fascinated by the method, an interaction of accounting, finance and psychology, and it was the topic of my doctoral thesis, on how distortions in info supply (delays, lies, errors) impacts inventory returns. In the actual world, that fascination has led me to concentrate to earnings reviews, which whereas overplayed, stay the first mechanism for firms to convey details about their efficiency and prospects to markets.

The Timing

The act additionally specifies that these filings be made in a well timed method, with a 1946 stipulation the annual filings being made inside 90 days of the fiscal year-end, and the quarterly reviews inside 45 calendar days of the quarter-end. With expertise rushing up the submitting course of, a 2002 rule modified these necessities to 60 days, for annual reviews, and 40 days for quarterly reviews, for firms with market capitalizations exceeding $700 million. Whereas there are some firms that take a look at out these limits, most firms file properly inside these deadlines, usually inside a few weeks of the yr or quarter ending, and lots of of them file their reviews on about the identical date yearly.

Should you couple the timing regularity in firm filings with the truth that nearly 65% of listed firms have fiscal years that coincide with calendar years, it ought to come as no shock that earnings reviews are likely to get bunched up at sure instances of the yr (mid-January, mid-April, mid-July and mid-October), creating “earnings seasons”. That mentioned, there are fairly a couple of firms, lots of them high-profile, that protect quirky fiscal years, and since Nvidia’s earnings report triggered this put up, it’s price noting that Nvidia has a fiscal yr that ends on January 31 of every yr, with quarters ending on April 30, July 31 and October 31. In reality, the Nvidia earnings report on August 28 lined the second quarter of this fiscal yr (which is Nvidia’s 2025 fiscal yr).

The Expectations Recreation

Whereas company earnings reviews are delivered as soon as 1 / 4, the work of anticipating what you count on these reviews to comprise, particularly by way of earnings per share, begins nearly instantly after the earlier earnings report is delivered. In reality, a good portion of promote facet fairness analysis is devoted to this exercise, with revisions made to the anticipated earnings, as you get nearer and nearer to the following earnings report. In making their earnings judgments and revisions, analysts draw on many sources, together with:

- The corporate’s historical past/information: With the usual caveat that the previous doesn’t assure future outcomes, analysts take into account an organization’s historic pattern strains in forecasting revenues and earnings. This may be augmented with different info that’s launched by the corporate through the course of the quarter.

- Peer group reporting: To the extent that the corporate’s peer group is affected by frequent components, it’s pure to think about the constructive or destructive the working outcomes from different firms within the group, that will have reported earnings forward of your organization.

- Different analysts’ estimates: A lot as analysts declare to be impartial thinkers, it’s human nature to be affected by what others within the group are doing. Thus, an upward revision in earnings by one analyst, particularly an influential one, can result in revisions upwards on the a part of different analysts.

- Macro information: Whereas macroeconomic information (concerning the financial system, inflation or foreign money trade charges) cuts throughout the market, by way of influence, some firms are extra uncovered to macroeconomic components than others, and analysts should revisit earnings estimates in gentle of latest info.

The earnings expectations for particular person firms, from promote facet fairness analysis analysts are publicly accessible, giving us a window on pattern strains.

Nvidia is without doubt one of the most generally adopted firms on the planet, and many of the seventy plus analysts who publicly observe the agency play the estimation recreation, main into the earnings reviews. Forward of the latest second quarter earnings report, the analyst consensus was that the corporate would report revenues of $28.42 billion for the quarter, and absolutely diluted earnings per share of 64 cents; within the 30 days main into the report, the earnings estimates had drifted up mildly (about 0.1%), with the delay within the Blackwell (NVidia’s new AI chip) talked about however not anticipated to have an effect on income progress close to time period. It’s price noting that not all analysts monitoring the inventory forecast each metric, and that there was disagreement amongst them, which can be captured within the vary on the estimates; on earnings per share, for example, the estimates ranged from 60 to 68 cents, and on revenues, from $26 to $30 billion.

The pre-game present shouldn’t be restricted to analysts and buyers, and markets partake within the expectations recreation in two methods.

- Inventory costs modify up or down, as earnings expectations are revised upwards or downwards, within the weeks main as much as the earnings report. Nvidia, which traded at $104 on Could twenty third, proper after the corporate reported its outcomes for the primary quarter of 2024, had its ups and down through the quarter, hitting an all-time excessive of $135.58 on June 18, 2024, and a low of $92.06, on August 5, earlier than ending at $125.61 on August 28, simply forward of the earnings report:

Throughout that interval, the corporate additionally break up its shares, ten to 1, on June 10, per week forward of reaching its highs.

- Inventory volatility can even modifications, relying upon disagreements amongst analysts about anticipated earnings, and the anticipated market response to earnings surprises. That impact is seen not solely in noticed inventory worth volatility, but in addition within the choices market, as implied volatility. For Nvidia, there was clearly far more disagreement amongst buyers concerning the contents of the second quarter earnings report, with implied volatility spiking within the weeks forward of the report:

{kind=link}

Whereas volatility tends to extend simply forward of earnings reviews, the surge in volatility forward of the second quarter earnings for Nvidia was unusually massive, a mirrored image of the disagreement amongst buyers about how the earnings report would play out available in the market. Put merely, even earlier than Nvidia reported earnings on August 28, markets have been indicating extra unease about each the contents of the report and the market response to the report, than they have been with prior earnings releases.

The Occasion

The centerpieces of the earnings report, not surprisingly, are the monetary statements, as working numbers are in comparison with expectations, and Nvidia’s second quarter numbers, no less than at first sight, are dazzling:

The corporate’s astonishing run of the previous few years continues, as its revenues, powered by AI chip gross sales, greater than doubled over the identical quarter final yr, and revenue margins got here in at stratospheric ranges. The issue, although, is that the corporate’s efficiency during the last three quarters, specifically, have created expectations that no firm can meet. Whereas it is only one quarter, there are clear indicators of extra slowing to come back, as scaling will proceed to push income progress down, the unit economics will likely be pressured as chip producers (TSMC) push for a bigger slice and working margins will lower, as competitors will increase.

Over the past twenty years, firms have supplemented the monetary reviews with steerage on key metrics, significantly revenues, margins and earnings, in future quarters. That steerage has two goals, with the primary directed at buyers, with the intent of offering info, and the second at analysts, to border expectations for the following quarter. As an organization that has performed the expectations recreation properly, it ought to come as no shock that Nvidia offered steerage for future quarters in its second quarter report, and right here too, there have been reminders that comparisons would get more difficult in future quarters, as they predicted that income progress charges would come again to earth, and that margins would, at greatest, degree off or maybe even decline.

Lastly, in an neglected information story, Nvidia introduced that it will had approved $50 billion in buybacks, over an unspecified timeframe. Whereas that money return is no surprise for a corporation that has grew to become a revenue machine, it’s at odds with the story that some buyers have been pricing into the inventory of an organization with nearly limitless progress alternatives in an immense new market (AI). Simply as Meta and Alphabet’s dividend initiations signaled that they have been approaching center age, Nvidia’s buyback announcement could also be signaling that the corporate is coming into a brand new section within the life cycle, deliberately or accidentally.

The Scoring

The ultimate piece of the incomes launch story, and the one which will get probably the most information consideration, is the market response to the earnings reviews. There may be proof in market historical past that earnings reviews have an effect on inventory costs, with the route of the impact relying on how precise earnings measure as much as expectations. Whereas there have been dozens of educational papers that concentrate on market reactions to earnings reviews, their findings will be captured in a composite graph that classifies earnings reviews into deciles, primarily based upon the earnings shock, outlined because the distinction between precise and predicted earnings:

As you may see, constructive surprises trigger inventory costs to extend, whereas destructive surprises result in worth drops, on the announcement date, however there’s drift each earlier than and after surprises in the identical route. The previous (costs drifting up earlier than constructive and down earlier than destructive surprises) is in line with the notion that details about earnings surprises leaks to markets within the days earlier than the report, however the latter (costs persevering with to float up after constructive or down after destructive surprises) signifies a slow-learning market that may maybe be exploited to earn extra returns. Breaking down the findings on earnings reviews, there appears to be proof that the that the earnings shock impact has moderated over time, maybe as a result of there are extra pathways for info to get to markets.

Nvidia shouldn’t be solely one of the crucial extensively adopted and talked about shares available in the market, however one which has discovered to play the expectations recreation properly, insofar because it appears to discover a strategy to beat them constantly, as will be seen within the following desk, which seems at their earnings surprises during the last 5 years:

|

| Nvidia Earnings Shock (%) |

Barring two quarters in 2022, Nvidia has managed to beat expectations on earnings per share each quarter for the final 5 years. There are two interpretations of those outcomes, and there’s fact in each of them. The primary is that Nvidia, as with many different expertise firms, has sufficient discretion in each its expenditures (particularly in R&D) and in its income recognition, that it may possibly use it to beat what analysts count on. The second is that the pace with which the demand for AI chips has grown has shocked everybody within the house (firm, analysts, buyers) and that the outcomes mirror the undershooting on forecasts.

Focusing particularly on the 2025 second quarter, Nvidia beat analyst expectations, delivering earnings per share of 68 cents (above the 64 cents forecast) and revenues of $30 billion (once more larger than the $28.4 billion forecast), however the share by which it beat expectations was smaller than in the latest quarters. Which will sound like nitpicking, however the expectations recreation is an insidious one, the place buyers transfer the objective posts continually, and extra so, if in case you have been profitable previously. On August 28, after the earnings report, Nvidia noticed share costs drop by 8% and never solely did that loss persist by the following buying and selling day, the inventory has continued to lose floor, and was buying and selling at $106 firstly of buying and selling on September 6, 2028.

Earnings Reviews: Studying the Tea Leaves

So what do you be taught from earnings reviews that will trigger you to reassess what a inventory is price? The reply will rely upon whether or not you take into account your self extra of a dealer or primarily an investor. If that distinction is misplaced on you, I’ll begin this part by drawing the distinction between the 2 approaches, and what every strategy is searching for in an earnings report.

Worth versus Worth

On the threat of revisiting a theme that I’ve used many instances earlier than, there are key variations in philosophy and strategy between valuing an asset and pricing it.

- The worth of an asset is decided by its fundamentals – money flows, progress and threat, and we try to estimate that worth by bringing in these fundamentals right into a assemble like discounted money circulation valuation or a DCF. Trying previous the modeling and the numbers, although, the worth of a enterprise in the end comes from the story you inform about that enterprise, and the way that story performs out within the valuation inputs.

- The worth of an asset is ready by demand and provide, and whereas fundamentals play a job, 5 a long time of behavioral finance has additionally taught us that momentum and temper have a a lot larger impact in pricing, and that the simplest strategy to pricing an asset is to search out out what others are paying for comparable property. Thus, figuring out how a lot to pay for a inventory through the use of a PE ratio derived from wanting its peer group is pricing the inventory, not valuing it.

The distinction between investing and buying and selling stems from this distinction between worth and worth. Investing is about valuing an asset, shopping for it at a worth lower than worth and hoping that the hole will shut, whereas buying and selling is nearly totally a pricing recreation, shopping for at a low worth and promoting at a better one, making the most of momentum or temper shifts. Given the very totally different views the 2 teams convey to markets, it ought to come as no shock that what merchants search for in an earnings report may be very totally different from what buyers see in that very same earnings report.

Earnings Reviews: The Buying and selling Learn

If costs are pushed by temper and momentum, it ought to come as no shock that what merchants are searching for in an earnings report are clues about how whether or not the prevailing temper and momentum will prevail or shift. It follows that merchants are likely to concentrate on the earnings per share surprises, since its centrality to the report makes it extra more likely to be a momentum-driver. As well as, merchants are additionally swayed extra by the theater round how earnings information will get delivered, as evidenced, for example, by the destructive response to a latest earnings report from Tesla, the place Elon Musk sounded downbeat, through the earnings name. Lastly, there’s a important suggestions loop, in pricing, the place the preliminary response to an earnings report, both on-line or within the after market, can have an effect on subsequent response. As a dealer, it’s possible you’ll be taught extra about how an earnings report will play out by watching social media and market response to it than by poring over the monetary statements.

For Nvidia, the second quarter report contained excellent news, if good is outlined as beating expectations, however the earnings beat was decrease than in prior quarters. Coupled with sober steerage and a priority the inventory had gone up an excessive amount of and too quick, as its market cap had elevated from lower than half a trillion to 3 trillion over the course of two years, the stage was set for a temper and momentum shift, and the buying and selling for the reason that earnings launch signifies that it has occurred. Observe, although, that this doesn’t imply that one thing else couldn’t trigger the momentum to shift again, however earlier than you, as an Nvidia supervisor or shareholder, are tempted to complain concerning the vagaries of momentum, acknowledge that for a lot of the final two years, no inventory has benefited extra from momentum than Nvidia.

The Investing Learn

For buyers, the takeaways from earnings reviews needs to be very totally different. If worth comes from key worth inputs (revenues progress, profitability, reinvestment and threat), and these worth inputs themselves come out of your firm narrative, as an investor, you’re looking on the earnings reviews to see if there’s info in them that may change your core narrative for the corporate. Thus, an earnings report can have a big impact on worth, if it considerably modifications the expansion, profitability or threat components of your organization’s story, though the corporate’s backside line (earnings per share) might need are available at expectations. Listed below are a couple of examples:

- An organization reporting income progress, small and even negligible for the second, however coming from a geography or product that has massive market potential, can see its worth bounce as a consequence. In 2012, I reassessed the worth of Fb upwards, a couple of months after it had gone public and seen its inventory worth collapse, as a result of its first earnings report, whereas disappointing by way of the underside line, contained indications that the corporate was beginning to achieve getting its platform engaged on good telephones, a historic weak spot for the agency.

- You too can have an organization reporting larger than anticipated income progress accompanied by decrease than anticipated revenue margins, suggesting a altering enterprise mannequin, and thus a modified story and valuation. Earlier this yr, I valued Tesla, and argued that their decrease margins, whereas dangerous information standing alone, was excellent news in case your story for Tesla was that it will emerge as a mass market vehicle firm, able to promoting extra automobiles than Volkswagen and Toyota. Because the solely pathway to that story is with lower-priced automobiles, the Tesla technique of chopping costs was consistent with that story, albeit on the expense of revenue margins.

- An organization reporting regulatory or authorized actions directed towards it, that make its enterprise mannequin extra pricey or extra dangerous to function, though its present numbers (revenues, earnings and many others.) are unscathed (to date).

Briefly, in case you are an investor, probably the most attention-grabbing elements of the report usually are not within the proverbial backside line, i.e., whether or not earnings per share got here in under or above expectations, however within the particulars. Lastly, as buyers, it’s possible you’ll be eager about how earnings reviews change market temper, normally a buying and selling focus, as a result of that temper change can function as a catalyst that causes the price-value hole to shut, enriching you within the course of.

The determine under summarizes this part, by first contrasting the worth and pricing processes, after which how earnings releases can have totally different meanings to totally different market members.

As in different facets of the market, it ought to subsequently come as no shock that the identical earnings report can have totally different penalties for various market members, and it’s also potential that what is nice information for one group (merchants) could also be dangerous information for an additional group (buyers).

Nvidia: Earnings and Worth

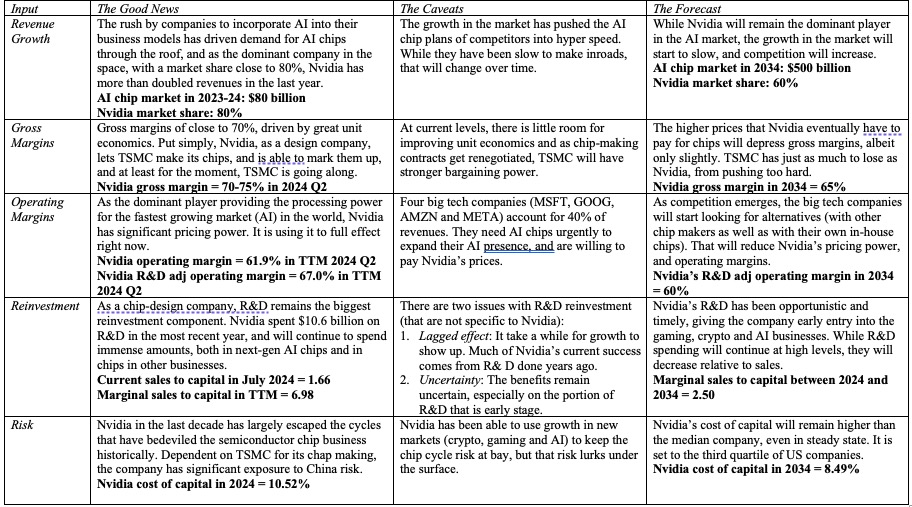

My buying and selling expertise are restricted, and that I’m incapable of enjoying the momentum recreation with any success. Consequently, I’m not certified to weigh in on the controversy on whether or not the momentum shift on Nvidia is momentary or long run, however I’ll use the Nvidia second quarter earnings report as a chance to revisit my Nvidia story and to ship a September 2024 valuation for the corporate. My intrinsic valuation fashions are parsimonious, constructed round income progress, revenue margins and reinvestment, and I used the second quarter earnings report back to overview my story (and inputs) on each:

|

| Nvidia: Valuation Inputs (Sept 2024) |

With these enter modifications in place, I revalued Nvidia firstly of September 2024, breaking its revenues, earnings and money flows down into three companies: an AI chip enterprise that continues to be its central progress alternative, and one during which it has a big lead on the competitors, an auto chip enterprise the place it’s a small participant in a small recreation, however one the place there’s potential coming from demand for extra highly effective chips in automobiles, and the remainder, together with its present enterprise in crypto and gaming, the place progress and margins are strong, however unlikely to maneuver dramatically. Whereas merchants could also be disenchanted with Nvidia’s earnings launch, and need it might preserve its present tempo going, I feel it’s each unrealistic and harmful to count on it to take action. In reality, one motive that my story for Nvidia has grow to be extra expansive, relative to my evaluation in June 2023, is that the pace with which AI structure is being put in place is permitting the entire market to develop at a price far sooner than I had forecast final yr. Briefly, relative to the place I used to be a couple of yr in the past, the final 4 earnings reviews from the corporate point out that the corporate can scale up greater than I believed it might, has larger and extra sustainable margins than I predicted and is maybe much less uncovered to the cycles that the chip enterprise has traditionally been victimized by. With these modifications in place, my worth per share for Nvidia in is about $87, nonetheless about 22% under the inventory worth of $106 that the inventory was buying and selling at on September 5, 2024, a big distinction however one that’s far smaller than the divergence that I famous final yr.

YouTube Video

Hyperlinks