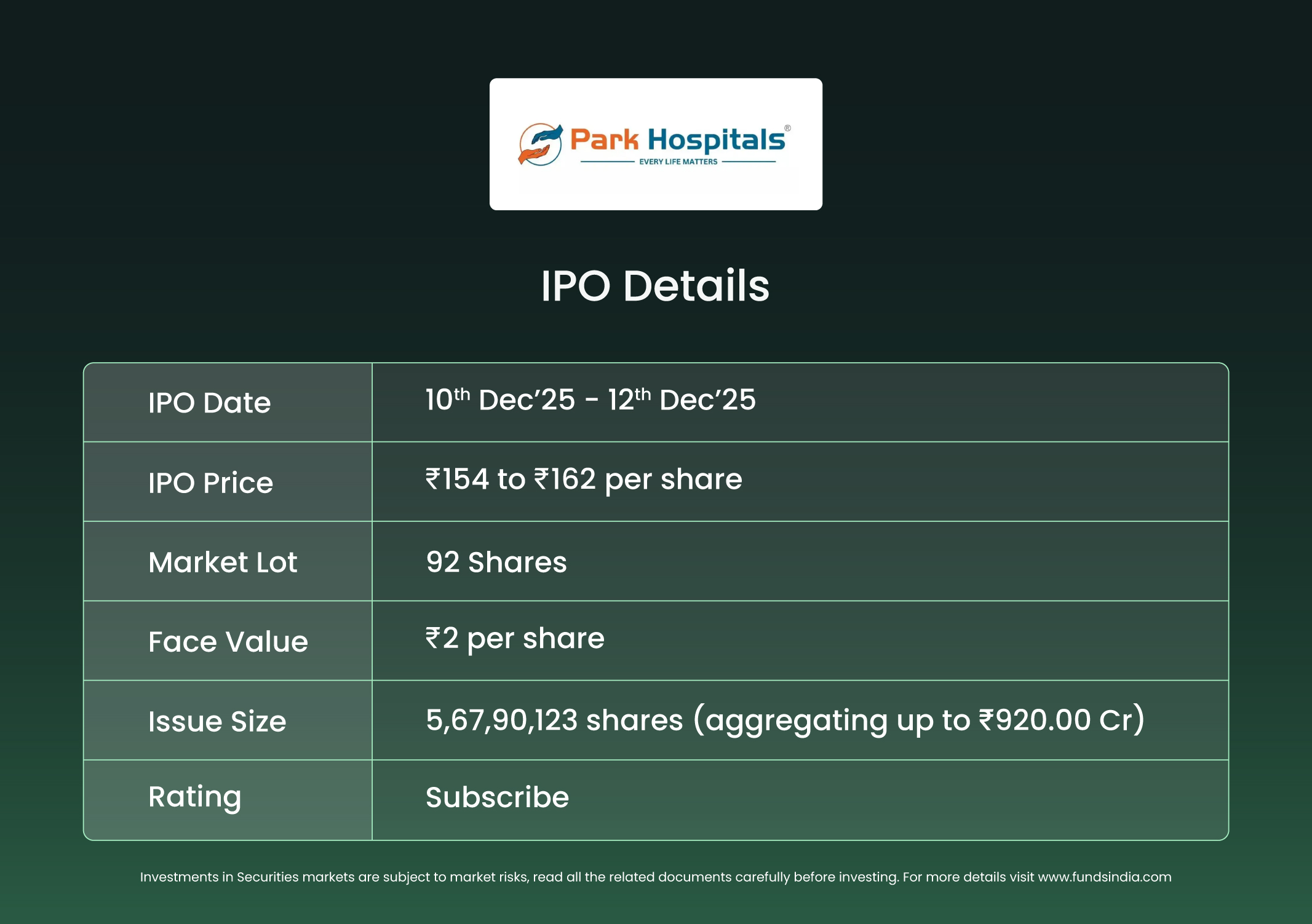

{kind=link}

Firm Overview

PMWL is a multi-super specialty healthcare providers supplier and the biggest personal hospital chain in North India by variety of operational beds amongst friends. As of September 30, 2025, the corporate operated a cluster-based community of 14 NABH-accredited hospitals with a complete capability of three,250 beds, together with 870 ICU beds and 67 operation theatres, together with two devoted most cancers items, concentrated throughout Delhi, Haryana, Rajasthan and Punjab. It additionally has approvals to carry out kidney transplants at 5 hospitals and has deployed robot-assisted surgical procedure programs (iMARS) to assist advanced minimally invasive procedures. The corporate’s complete healthcare providers span throughout specialties equivalent to cardiac sciences, neurosciences, orthopedics, transplant care, renal sciences, gastro sciences, and oncology.

Its enterprise mannequin is centred round pure-play healthcare providers, with no income from sale of pharmaceutical or healthcare merchandise reported in FY23–FY25, and in-patient providers contributing over 95% of FY25 service revenue, whereas out-patient providers type a comparatively smaller share.

Objects of the supply

- To allow compensation/ prepayment, in full or partly, of excellent borrowings availed by the Firm and its Subsidiaries.

- To fund capital expenditure for growth of recent hospital by Subsidiary, Park Medicity (NCR).

- To fund capital expenditure for buy of medical tools by the Firm and its Subsidiaries, Blue Heavens and Ratangiri.

- To fund unidentified inorganic acquisitions and basic company functions

Funding Rationale

- Strategic management in an undersupplied North India healthcare market – PMWL is the biggest personal hospital chain in North India by operational beds amongst friends, working 3,250 beds throughout 14 NABH-accredited hospitals in Delhi, Haryana, Rajasthan and Punjab. North India has the bottom healthcare penetration amongst main areas in India, with solely ~15–16 beds (world imply is 33 beds per 10,000 inhabitants) and ~7 medical doctors per 10,000 inhabitants but is predicted to develop at a 12–14% CAGR to Rs.3.3–3.4 trillion by FY29. PMWL primarily serves middle-income sufferers below authorities and PSU healthcare schemes, supported by sturdy empanelment. This allows high-volume, important care supply in areas the place credible tertiary capability is scarce, making a market place that advantages from each structural undersupply and robust affected person entry pipelines by way of giant institutional payors.

- Sturdy operational effectivity regardless of affordability-led pricing – PMWL operates with wholesome utilization in high-acuity specialties, reporting 68.14% occupancy in H1FY26 and an ALOS (Common size of keep) of 6.53–6.66 days throughout FY24–FY25. Regardless of a considerably decrease ARPOB (Common income per occupied mattress) of Rs.27,105 in H1FY26 in contrast with premium chains equivalent to Fortis Healthcare (Rs.68,200), International Well being (Rs.65,600) and KIMS (Rs.42,500), the corporate delivered the next EBITDA margin of 26.85% in H1FY26 than these friends. It additionally maintains environment friendly asset deployment, with gross block per mattress of Rs.3.65 million and fixed-asset turnover of 0.76x in H1FY26. This skill to maintain profitability at considerably cheaper price factors displays a cost-competitive working mannequin properly aligned with high-volume underserved markets in North India.

- Monetary Efficiency – The corporate delivered a consolidated income from operations of Rs.1,394 crore in FY25, rising 13% YoY from Rs.1,231 crore in FY24. EBITDA was recorded at Rs.372 crore in FY25 with a margin of 26.71% up from Rs.310 crore in FY24, marking a 20% YoY development. PAT for FY25 stood at Rs.213 crore, translating to a margin of 15%, a rise of 40% YoY. Regardless of community growth and newly added property, the corporate maintained double-digit returns with ROE of 21% and ROCE of 17%.

Key Dangers

- Excessive Dependence on Authorities Schemes and PSUs – A major majority of income is derived from authorities schemes and PSU-funded sufferers, making collections susceptible to delayed funds or declare rejections from public businesses. Such delays might adversely have an effect on money flows and dealing capital.

- Geographic Focus in Haryana – Hospitals in Haryana contributed 73.43% of income from operations in FY25. Any native regulatory tightening, coverage modifications, or opposed developments within the state might materially impression enterprise efficiency.

- OFS-Threat – A considerable portion of the IPO is an Provide for Sale, permitting promoters to partially monetize holdings with no direct capital infusion into the enterprise. The supply contains the sale of stake price Rs.1,500 million by promoter Dr Ajit Gupta.

Outlook

Park Medi World has demonstrated sustained income development, robust working margins, and environment friendly capital deployment inside the North India hospital market. Its concentrate on high-acuity specialties, cluster-based growth mannequin, and affordability-led positioning present a stable platform for continued scale and utilization enchancment. A significant allocation of IPO proceeds towards debt discount and community growth is predicted to strengthen steadiness sheet flexibility and assist incremental mattress additions. In line with the RHP, Fortis Healthcare Ltd, Apollo Hospitals Enterprise Ltd, Max Healthcare Institute Ltd are a number of of its listed friends. The friends are buying and selling at a median P/E of 69.11x with the very best P/E of 101.54x and the bottom being 48.6x. On the increased value band, the itemizing market cap of Park Medi World will likely be ~Rs. 6,997 crore and the corporate is demanding a P/E a number of of 33x based mostly on publish subject diluted FY25 EPS of Rs.4.93. In comparison with its friends, the problem appears to be totally priced in (pretty valued). Based mostly on the above views, we offer a ‘Subscribe’ score for this IPO for a medium to long-term Holding.

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please observe that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you might like

Submit Views:

61