{kind=link}

My private finance pipedream for America is that we undertake one thing like Australia’s retirement system the place employees are pressured to avoid wasting a sure proportion of their earnings for retirement.

That pipedream won’t ever occur as a result of Individuals hate being pressured to do something.

It’s worthwhile to make individuals suppose that saving for retirement is their concept.

Fortunately, behavioral psychologists have discovered sufficient about alternative structure that we are able to use plan design to encourage extra individuals to avoid wasting for retirement.

In current many years, outlined contribution plans have added options like default financial savings charges, computerized sign-up (opt-out as a substitute of opt-in), default diversified funding alternatives and escalating financial savings charges over time to enhance outcomes for retirement savers.

It’s a gentle drive that’s helped tens of millions of individuals save greater than they might have if that they had made the selection on their very own.

The issue is that the “pressured” financial savings charges initially launched by most corporations had been too low. A 3% financial savings fee was the preliminary default for many of those plans.

That’s simply not going to chop it for many households.

Fortunately, corporations at the moment are growing the default financial savings fee.

The Wall Road Journal had a current piece that exhibits 6% is the brand new 3% relating to default financial savings charges:

I would like one thing nearer to 10% however that is progress.

Right here’s extra coloration from the story:

Almost a 3rd of corporations that use computerized 401(ok) enrollment now begin employees saving at 6% of their salaries or larger, about double the share of organizations that did so a decade in the past, in accordance with Vanguard Group.

About 60% of corporations mechanically enroll new hires, bringing 401(ok) participation charges to 82% of eligible employees, up from 66% in 2007, in accordance with Vanguard, which administers 401(ok)-type accounts for almost 5 million individuals.

Immediately 91% of the Verizon plan’s 68,000 members are saving 6% or extra, and obtain the complete match, up from 78% in 2020, earlier than the swap, he mentioned.

That is excellent news!1

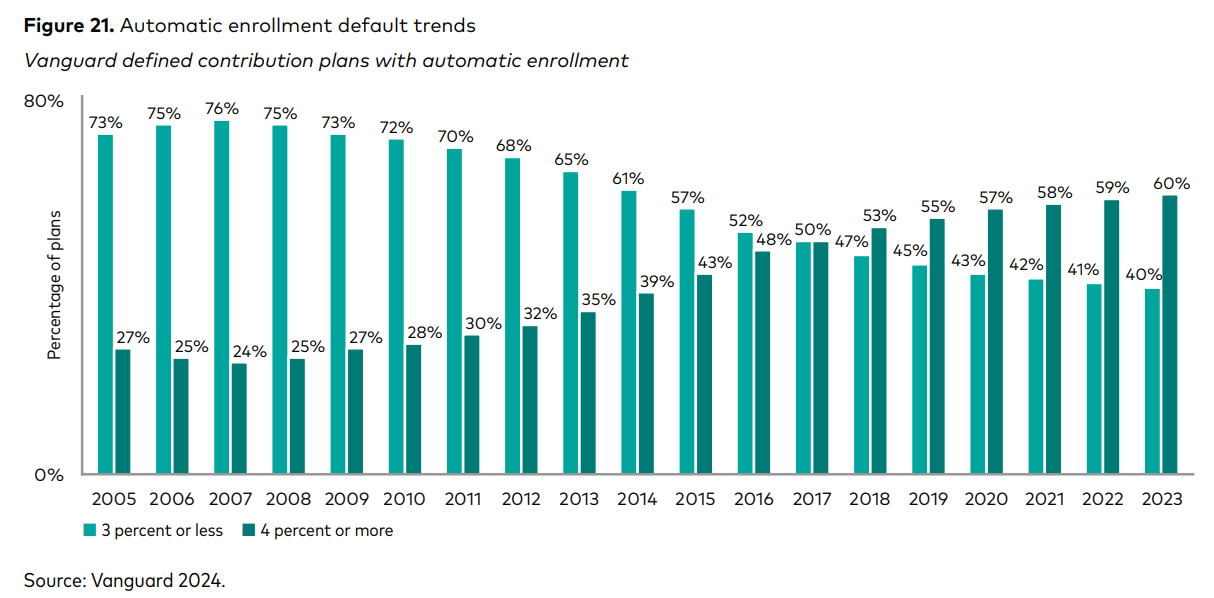

Vanguard’s annual How America Saves report, which covers 5 million outlined contribution retirement plan members, exhibits the same development in auto-enrollment financial savings charges:

We will construct on this!2

Most individuals would like the previous system the place staff got outlined profit pensions. Sounds pretty in concept however there is no such thing as a approach profit-seeking corporations had been going to place up with these prices what with individuals residing longer and all.

Prefer it or not, it was by no means sustainable for employers to cowl their staff’ retirement spending (or healthcare prices).

The 401k plan is much from good as a result of there are nonetheless many plans that cost egregious charges and there are many employers that don’t even provide their staff a retirement plan.

I want the U.S. authorities would mechanically enroll anybody who earns earnings (with an opt-out, clearly) within the TSP as a nationwide retirement plan. Alas, one more pipedream.

Regardless, outlined contribution plans such because the 401k are significantly better than tens of millions of individuals being fully on their very own relating to saving for retirement.

The entire behavioral nudges 401k plans and the like have added are having a huge impact on the monetary markets at giant as effectively.

Listed here are some issues I imagine however can’t show for sure about these impacts:

Computerized investing will increase valuations. There are many causes valuations on the inventory market have been slowly climbing for years.

Hundreds of thousands of individuals placing cash to work within the inventory market out of each single paycheck needed to trigger an upward bias in valuations.

This merely didn’t exist prior to now.

Computerized investing makes buyers higher behaved. Targetdate funds are the default funding automobile in 401k plans and now have one thing like $3.5 trillion in them.

These funds are usually low price, diversified and mechanically rebalanced. This can be a win for buyers who’re overwhelmed, wish to simplify or don’t know what to spend money on.

Plus, there’s the truth that 401k plans allow you to to avoid wasting mechanically in a set-it-and-forget-it method.

These options permit buyers to automate good conduct.

Computerized investing received’t cease bear markets. Automated investing has performed a task within the upward trajectory within the inventory market the previous 4 many years for positive.

However there are nonetheless loads of buyers who don’t automate their investments who freak out, get fearful when others are fearful and attempt to outsmart the market.

In different phrases, people are nonetheless human.

Whereas they will’t cease markets from taking place once in a while, the trillions of {dollars} in outlined contribution retirement plans have ceaselessly modified the markets.

Michael and I talked concerning the affect of 401k plans on the inventory market and rather more on this week’s Animal Spirits video:

Subscribe to The Compound so that you by no means miss an episode.

Additional Studying:

How the Particular person Retirement Account Modified the Inventory Market Ceaselessly

Now right here’s what I’ve been studying recently:

Books:

1My spouse usually tells me I’m not enthusiastic sufficient, so I’m doing my greatest to make use of extra exclamation factors right here and there. It doesn’t really feel pure, however I’m attempting.

2OK that’s an excessive amount of. I’ll cease now.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.