{kind=link}

A reader from down beneath asks:

You guys have been speaking loads about US financial exceptionalism lately with the caveat that homes are too costly. Honest sufficient. However try housing costs in Australia the place I stay. It’s insanity! Folks have been saying it’s a bubble for years whereas costs simply hold going increased. I don’t actually have a query. Simply wished to level out that costs within the states look tame by comparability. Cheers.

I’m in full settlement with my Australian pal right here.

Whereas it looks like the U.S. housing market is totally damaged and costs are out of attain for thousands and thousands of People, the state of affairs is far worse in different nations. Particularly Australia.

The median worth for an present residence in the US is round $410,000. In Australia it’s greater than $800,000. In Syndey, the median worth of a house is nicely over $1 million.

Householders within the U.S. have skilled unimaginable good points over the previous 30-40 years however we’ve received nothing on Australia:

For the reason that late-Nineteen Eighties, housing costs down beneath have greater than doubled up our returns on homeownership.

It’s additionally import to place these worth good points into context when it comes to affordability. I like to do that by evaluating worth good points to wage good points.

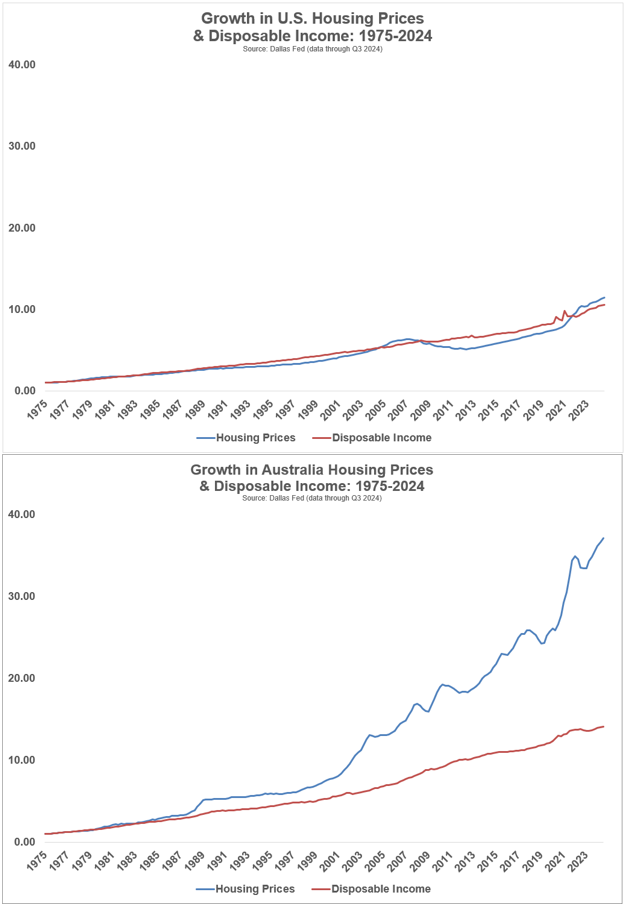

These charts present housing worth progress versus the expansion in disposable earnings for each the US and Australia going again to 1975:

I put these time collection on the identical scale to point out simply how out of whack this relationship is in Australia. Within the U.S., housing costs and disposable incomes have grown roughly in lockstep with each other. Not so in Australia the place the chart appears like an alligator opening vast and exhibiting off its enamel.

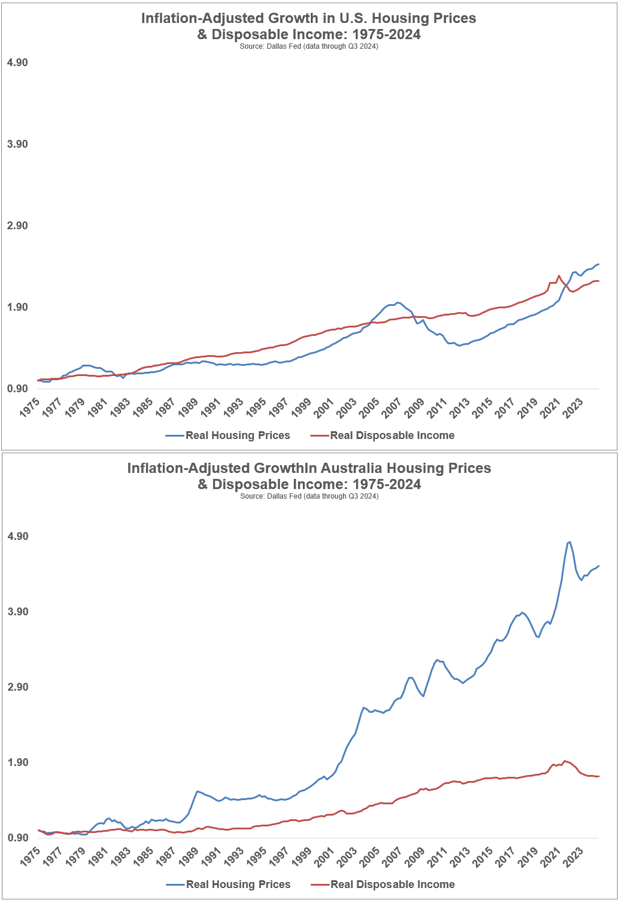

Some folks desire utilizing inflation-adjusted information when making comparisons throughout borders:

The true information paints the same image.

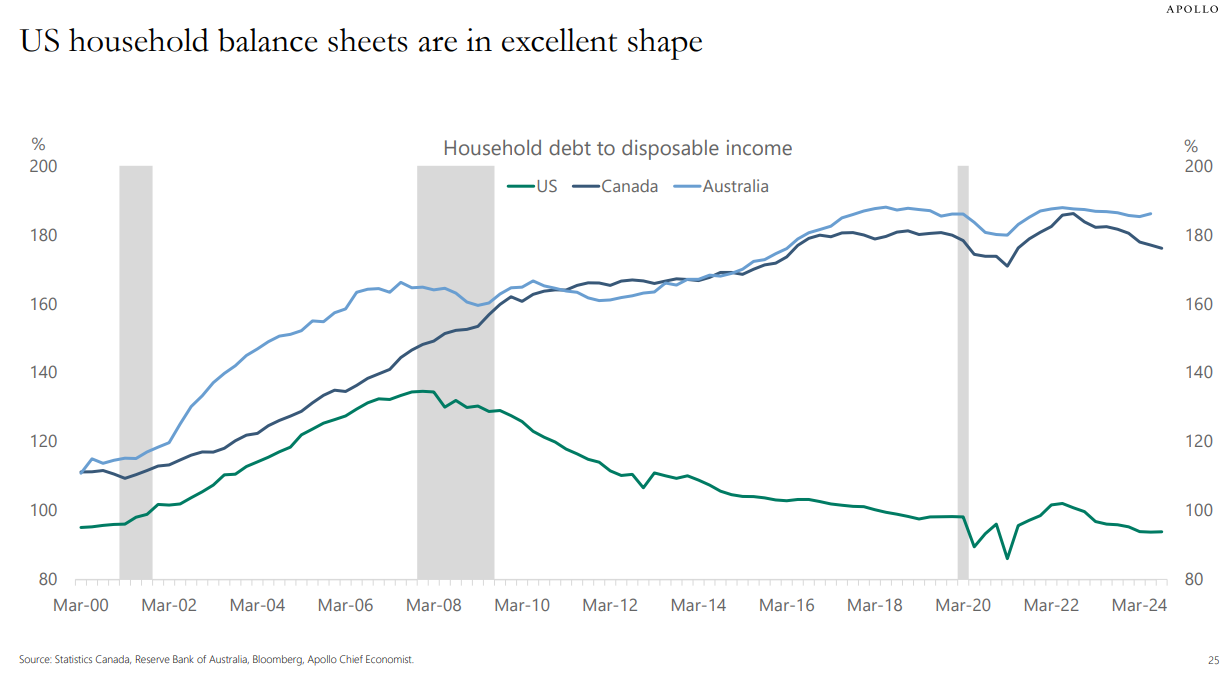

Torsten Slok has an ideal chart that compares family debt to disposable earnings within the U.S., Canada and Australia:

Canada and Australia have seen debt-to-income ratios rise for years now whereas U.S. households have been repairing their stability sheets ever because the Nice Monetary Disaster. Larger housing costs are clearly the principle wrongdoer right here

Mortgage debt makes up 70% of family debt within the U.S. I don’t have the precise figures for Australian households however I’m guessing it’s the same profile.

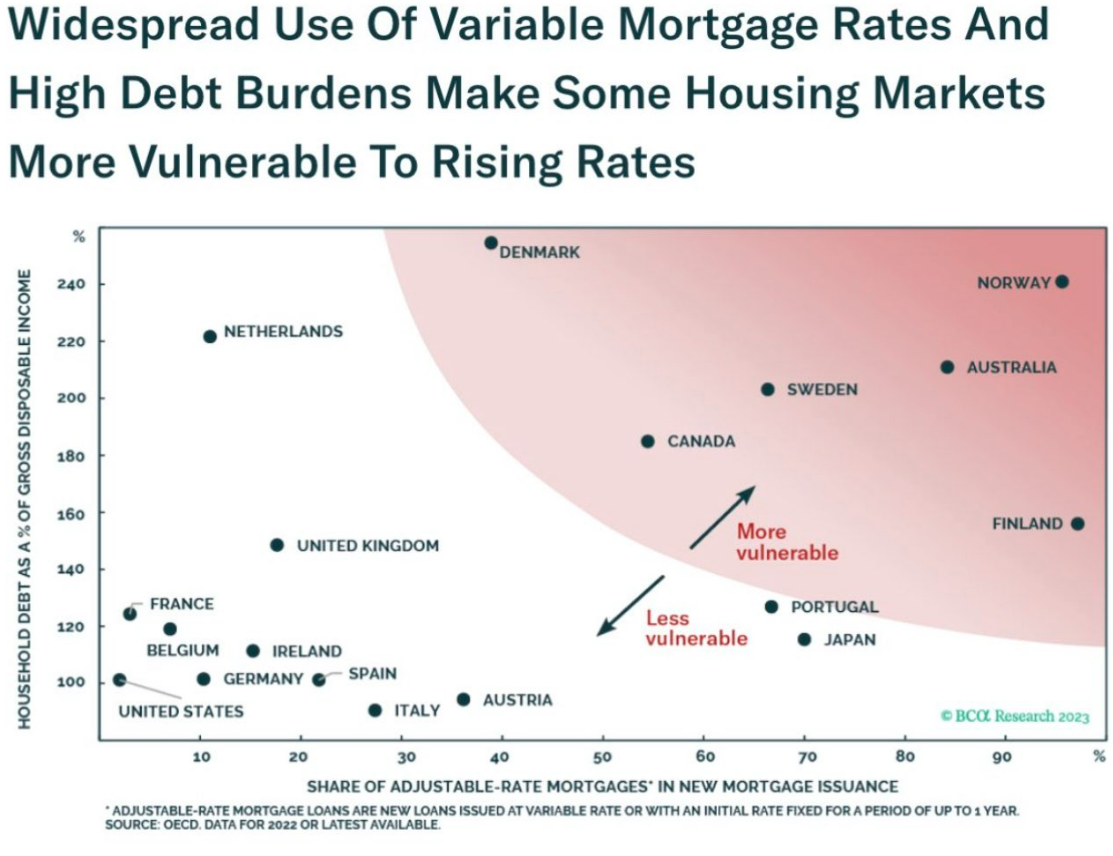

But it surely’s not simply increased housing prices which are hurting Australian family stability sheets. Larger rates of interest lately have damage most owners due to how their mortgage market is structured.

The next chart reveals debt to earnings by nation plotted in opposition to the utilization of variable charge mortgages:

You possibly can see Australia has one of many highest shares of variable-rate mortgages. So far as I can inform you’re in a position to lock in your charge for round 5 years after which it resets. This was a beautiful set-up when charges had been falling, however now that we’re in the next rate of interest world, it’s costlier for present and new owners alike.

U.S. owners had been in a position to lock in 3% mortgage charges in the course of the pandemic to defend themselves from a rising charge atmosphere. That’s not the case in lots of different nations as a result of they don’t make the most of 30 12 months mounted charge mortgages like we do.

Does another person’s state of affairs make these struggling to purchase a house in America really feel any higher about their very own state of affairs?

In fact not!

But it surely’s price declaring that as dangerous because the housing market appears proper now within the U.S. from an affordability perspective it might all the time be worse. It is worse in loads of different nations.

And it’s doable we might see affordability get even worse right here if we don’t make it simpler to construct extra properties to repair our housing scarcity.

We coated this query on the most recent episode of Ask the Compound:

Invoice Candy joined me on the present this week to debate questions concerning the tax advantages of proudly owning rental properties, the tax implications of an inheritance, retirement planning for navy service members and the way tariffs work.

Additional Studying:

The U.S. Housing Market vs. The Canadian Housing Market

This content material, which comprises security-related opinions and/or info, is offered for informational functions solely and shouldn’t be relied upon in any method as skilled recommendation, or an endorsement of any practices, services or products. There will be no ensures or assurances that the views expressed right here might be relevant for any specific info or circumstances, and shouldn’t be relied upon in any method. It’s best to seek the advice of your individual advisers as to authorized, enterprise, tax, and different associated issues regarding any funding.

The commentary on this “submit” (together with any associated weblog, podcasts, movies, and social media) displays the private opinions, viewpoints, and analyses of the Ritholtz Wealth Administration staff offering such feedback, and shouldn’t be regarded the views of Ritholtz Wealth Administration LLC. or its respective associates or as an outline of advisory companies offered by Ritholtz Wealth Administration or efficiency returns of any Ritholtz Wealth Administration Investments consumer.

References to any securities or digital property, or efficiency information, are for illustrative functions solely and don’t represent an funding advice or provide to supply funding advisory companies. Charts and graphs offered inside are for informational functions solely and shouldn’t be relied upon when making any funding determination. Previous efficiency will not be indicative of future outcomes. The content material speaks solely as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these supplies are topic to vary with out discover and should differ or be opposite to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Administration, receives cost from numerous entities for ads in affiliated podcasts, blogs and emails. Inclusion of such ads doesn’t represent or indicate endorsement, sponsorship or advice thereof, or any affiliation therewith, by the Content material Creator or by Ritholtz Wealth Administration or any of its staff. Investments in securities contain the chance of loss. For extra commercial disclaimers see right here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see disclosures right here.