{kind=link}

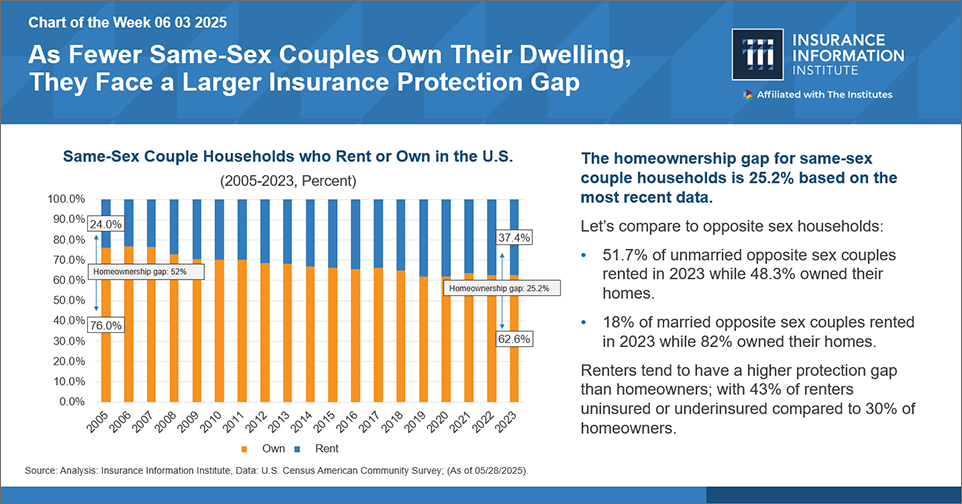

As a part of an ongoing dialogue on the hyperlink between the housing and insurance coverage markets, the Insurance coverage Data Institute (Triple-I) launched a Chart of the Week (COTW), “As Fewer Identical-Intercourse {Couples} Personal Their Dwelling, They Face a Bigger Insurance coverage Safety Hole.” Based mostly on information from 2023, 62.6 % of same-sex households personal their properties and 37.4 % lease, representing a homeownership hole of 25.2 proportion factors inside this neighborhood. As compared, 82 % of married opposite-sex households personal their properties, whereas solely 18 % lease.

{kind=link}

In the US, homeownership provides a number of advantages (versus renting) to these with the monetary sources to attain and maintain it. House owners can accrue fairness to extend their possibilities of making a revenue after they promote their residence. They’ll reap tax advantages via mortgage deductions. Mortgage holders may decrease month-to-month housing prices when rates of interest drop. Finally, a house can improve private internet price and provide a mechanism to switch wealth to the subsequent era. Defending this asset and its contents makes good monetary sense.

Renters could not personal their dwelling, however they hold private belongings in it. They’ll face severe monetary dangers within the occasion of a loss, theft, catastrophe, or private legal responsibility occasion. But, in keeping with the COTW, 43 % of renters are uninsured or underinsured, in comparison with 30 % of householders. There are a number of causes attributable to this distinction, but it surely’s important to maintain one on the forefront: insurance coverage protection necessities are commonplace in mortgage agreements however not in lease agreements. Thus, homeownership standing can drive participation within the insurance coverage market.

Analyzing elements that impede homeownership for same-sex {couples} would possibly make clear how one can entice and retain extra policyholders on this demographic. Wanting intently on the interaction of simply three of those – housing costs, geography, and legislative setting – reveals that housing tends to be extra costly in LGBTQIA+-friendly areas. Potential patrons could must earn not less than $150,000 a yr – as a lot as 50 % extra – to keep away from dwelling in areas with out fundamental authorized protections, in keeping with a current examine of actual property market information throughout 54 main U.S. metropolitan areas.

Excessive month-to-month housing prices pressure budgets, pushing householders and renters out of the insurance coverage market. It may additionally put the monetary {qualifications} for residence shopping for – i.e., constructing credit score and financial savings – out of attain. Households are thought-about cost-burdened after they spend greater than 30 % of their earnings on lease, mortgage funds, and different housing prices, in keeping with the U.S. Division of Housing and City Improvement (HUD).

Nationwide, renters had increased median housing prices as a proportion of their earnings (31.0 %) in comparison with householders (21.1 % for householders with a mortgage and 11.5 % for these with out a mortgage). In metropolitan areas that welcome and shield range, renters usually tend to be housing cost-burdened, notably in New York (52.1 % of residents pay greater than 30 % of their earnings) and San Francisco (37.6 % of residents). Renters in states and municipalities the place laws is significantly much less welcoming however rents are decrease can face comparatively increased premiums for rental protection.

Regardless of the legalization of same-sex marriage and numerous anti-discrimination legal guidelines, the LGBTQ neighborhood nonetheless battles appreciable discrimination and systemic biases in lots of areas of life, together with housing. Insurers can work to higher perceive the varied wants of LGBTQIA+ people, {couples}, and their households, facilitating simpler options for managing monetary dangers. And most significantly, the business can enhance communication round potential protection advantages for these households.

“We will begin closing the safety hole by having individuals on the desk who perceive the lived experiences behind the numbers,” says Amy Cole-Smith, Govt Director for BIIC/ Director of Range at The Institutes.

For instance, renters would possibly discover it useful to know their coverage covers a loss occasion linked to discrimination in opposition to them, resembling malicious harm or vandalism to the property by a 3rd celebration. Even when it’s evident the destruction isn’t the renter’s fault, the owner would possibly nonetheless try to carry them accountable, both via a lawsuit, a lease improve, or eviction. Moreover, single {couples} must be knowledgeable about whether or not the insurer contains each companions’ names on a coverage and the way this provision impacts them within the occasion of a declare.

“Cultivating an inclusive workforce drives smarter options, like renters’ insurance coverage that aligns with the realities of same-sex {couples}, extra equitable underwriting, and advertising and marketing that actually resonates,” Cole-Smith says. “This isn’t nearly fairness—it’s about unlocking development and staying aggressive in a altering market. When the insurance coverage workforce displays the variety of the market, we’re in a stronger place to construct merchandise that meet individuals the place they’re.”

Triple-I works to advance the dialog round essential points within the insurance coverage business, together with Expertise and Recruitment. To affix the dialogue, register for JIF 2025. We additionally invite you to observe our weblog to be taught extra about traits in insurance coverage affordability and availability throughout the property/casualty market.